- Netherlands

- /

- Specialty Stores

- /

- ENXTAM:BBED

Beter Bed Holding (AMS:BBED) Has Some Difficulty Using Its Capital Effectively

If you're looking at a mature business that's past the growth phase, what are some of the underlying trends that pop up? A business that's potentially in decline often shows two trends, a return on capital employed (ROCE) that's declining, and a base of capital employed that's also declining. This reveals that the company isn't compounding shareholder wealth because returns are falling and its net asset base is shrinking. Having said that, after a brief look, Beter Bed Holding (AMS:BBED) we aren't filled with optimism, but let's investigate further.

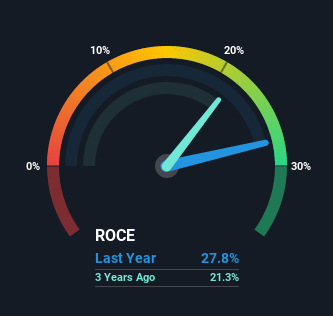

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Beter Bed Holding:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.28 = €13m ÷ (€116m - €70m) (Based on the trailing twelve months to December 2020).

Thus, Beter Bed Holding has an ROCE of 28%. That's a fantastic return and not only that, it outpaces the average of 11% earned by companies in a similar industry.

Check out our latest analysis for Beter Bed Holding

In the above chart we have measured Beter Bed Holding's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Beter Bed Holding here for free.

The Trend Of ROCE

The trend of returns that Beter Bed Holding is generating are raising some concerns. The company used to generate 39% on its capital five years ago but it has since fallen noticeably. What's equally concerning is that the amount of capital deployed in the business has shrunk by 42% over that same period. The combination of lower ROCE and less capital employed can indicate that a business is likely to be facing some competitive headwinds or seeing an erosion to its moat. If these underlying trends continue, we wouldn't be too optimistic going forward.

While on the subject, we noticed that the ratio of current liabilities to total assets has risen to 61%, which has impacted the ROCE. Without this increase, it's likely that ROCE would be even lower than 28%. And with current liabilities at these levels, suppliers or short-term creditors are effectively funding a large part of the business, which can introduce some risks.

The Key Takeaway

To see Beter Bed Holding reducing the capital employed in the business in tandem with diminishing returns, is concerning. This could explain why the stock has sunk a total of 72% in the last five years. With underlying trends that aren't great in these areas, we'd consider looking elsewhere.

If you'd like to know about the risks facing Beter Bed Holding, we've discovered 1 warning sign that you should be aware of.

If you want to search for more stocks that have been earning high returns, check out this free list of stocks with solid balance sheets that are also earning high returns on equity.

If you’re looking to trade Beter Bed Holding, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade Beter Bed Holding, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Beter Bed Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ENXTAM:BBED

Beter Bed Holding

Beter Bed Holding N.V. retails and wholesales bedroom furnishing products in the Netherlands and Belgium.

Flawless balance sheet with moderate growth potential.

Market Insights

Community Narratives