Can Mixed Fundamentals Have A Negative Impact on QES Group Berhad (KLSE:QES) Current Share Price Momentum?

Most readers would already be aware that QES Group Berhad's (KLSE:QES) stock increased significantly by 6.8% over the past week. However, we decided to pay attention to the company's fundamentals which don't appear to give a clear sign about the company's financial health. Specifically, we decided to study QES Group Berhad's ROE in this article.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

See our latest analysis for QES Group Berhad

How Is ROE Calculated?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for QES Group Berhad is:

8.6% = RM8.2m ÷ RM96m (Based on the trailing twelve months to June 2020).

The 'return' is the income the business earned over the last year. So, this means that for every MYR1 of its shareholder's investments, the company generates a profit of MYR0.09.

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

A Side By Side comparison of QES Group Berhad's Earnings Growth And 8.6% ROE

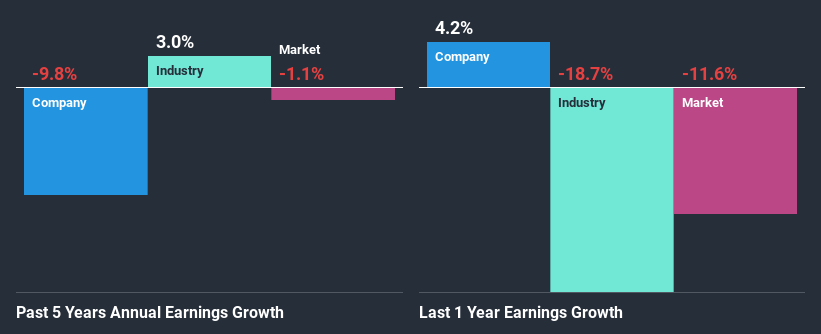

At first glance, QES Group Berhad's ROE doesn't look very promising. Yet, a closer study shows that the company's ROE is similar to the industry average of 9.7%. But then again, QES Group Berhad's five year net income shrunk at a rate of 9.8%. Bear in mind, the company does have a slightly low ROE. Therefore, the decline in earnings could also be the result of this.

That being said, we compared QES Group Berhad's performance with the industry and were concerned when we found that while the company has shrunk its earnings, the industry has grown its earnings at a rate of 3.0% in the same period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. If you're wondering about QES Group Berhad's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is QES Group Berhad Making Efficient Use Of Its Profits?

In spite of a normal three-year median payout ratio of 30% (that is, a retention ratio of 70%), the fact that QES Group Berhad's earnings have shrunk is quite puzzling. So there could be some other explanations in that regard. For instance, the company's business may be deteriorating.

In addition, QES Group Berhad only recently started paying a dividend so the management probably decided the shareholders prefer dividends even though earnings have been shrinking.

Summary

Overall, we have mixed feelings about QES Group Berhad. While the company does have a high rate of profit retention, its low rate of return is probably hampering its earnings growth. With that said, we studied the latest analyst forecasts and found that while the company has shrunk its earnings in the past, analysts expect its earnings to grow in the future. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

When trading QES Group Berhad or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if QES Group Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KLSE:QES

QES Group Berhad

An investment holding company, engages in the manufacture, distribution, and provision of engineering services for inspection, test, measuring, analytical, and automated handling equipment.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)