- Malaysia

- /

- Specialty Stores

- /

- KLSE:CARLORINO

Could The Market Be Wrong About Carlo Rino Group Berhad (KLSE:CARLORINO) Given Its Attractive Financial Prospects?

It is hard to get excited after looking at Carlo Rino Group Berhad's (KLSE:CARLORINO) recent performance, when its stock has declined 16% over the past three months. However, stock prices are usually driven by a company’s financial performance over the long term, which in this case looks quite promising. In this article, we decided to focus on Carlo Rino Group Berhad's ROE.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

View our latest analysis for Carlo Rino Group Berhad

How To Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Carlo Rino Group Berhad is:

16% = RM18m ÷ RM110m (Based on the trailing twelve months to September 2024).

The 'return' is the amount earned after tax over the last twelve months. That means that for every MYR1 worth of shareholders' equity, the company generated MYR0.16 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Carlo Rino Group Berhad's Earnings Growth And 16% ROE

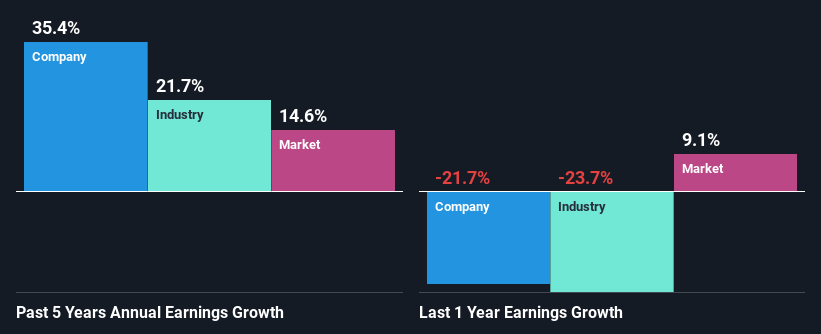

To start with, Carlo Rino Group Berhad's ROE looks acceptable. On comparing with the average industry ROE of 8.4% the company's ROE looks pretty remarkable. This certainly adds some context to Carlo Rino Group Berhad's exceptional 35% net income growth seen over the past five years. We believe that there might also be other aspects that are positively influencing the company's earnings growth. For instance, the company has a low payout ratio or is being managed efficiently.

We then compared Carlo Rino Group Berhad's net income growth with the industry and we're pleased to see that the company's growth figure is higher when compared with the industry which has a growth rate of 22% in the same 5-year period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. If you're wondering about Carlo Rino Group Berhad's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Carlo Rino Group Berhad Using Its Retained Earnings Effectively?

The three-year median payout ratio for Carlo Rino Group Berhad is 36%, which is moderately low. The company is retaining the remaining 64%. By the looks of it, the dividend is well covered and Carlo Rino Group Berhad is reinvesting its profits efficiently as evidenced by its exceptional growth which we discussed above.

Besides, Carlo Rino Group Berhad has been paying dividends over a period of five years. This shows that the company is committed to sharing profits with its shareholders.

Summary

On the whole, we feel that Carlo Rino Group Berhad's performance has been quite good. Specifically, we like that the company is reinvesting a huge chunk of its profits at a high rate of return. This of course has caused the company to see substantial growth in its earnings. If the company continues to grow its earnings the way it has, that could have a positive impact on its share price given how earnings per share influence long-term share prices. Let's not forget, business risk is also one of the factors that affects the price of the stock. So this is also an important area that investors need to pay attention to before making a decision on any business. You can see the 3 risks we have identified for Carlo Rino Group Berhad by visiting our risks dashboard for free on our platform here.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:CARLORINO

Carlo Rino Group Berhad

An investment holding company, designs, promotes, markets, distributes, and retails women's footwear, handbags, and accessories under the Carlo Rino brand in Malaysia.

Flawless balance sheet average dividend payer.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)