Advertisement

- Malaysia

- /

- Real Estate

- /

- KLSE:GLOMAC

Bullish: Analysts Just Made A Significant Upgrade To Their Glomac Berhad (KLSE:GLOMAC) Forecasts

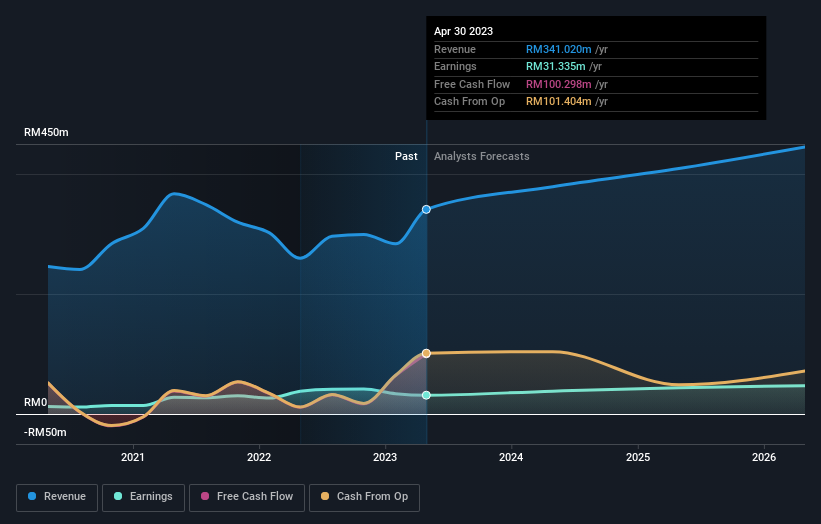

Glomac Berhad (KLSE:GLOMAC) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's forecasts. Consensus estimates suggest investors could expect greatly increased statutory revenues and earnings per share, with analysts modelling a real improvement in business performance.

Following the upgrade, the most recent consensus for Glomac Berhad from its three analysts is for revenues of RM379m in 2024 which, if met, would be a meaningful 11% increase on its sales over the past 12 months. Statutory earnings per share are presumed to surge 21% to RM0.049. Previously, the analysts had been modelling revenues of RM337m and earnings per share (EPS) of RM0.043 in 2024. So we can see there's been a pretty clear increase in analyst sentiment in recent times, with both revenues and earnings per share receiving a decent lift in the latest estimates.

Check out our latest analysis for Glomac Berhad

Despite these upgrades, the analysts have not made any major changes to their price target of RM0.38, suggesting that the higher estimates are not likely to have a long term impact on what the stock is worth. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Glomac Berhad, with the most bullish analyst valuing it at RM0.43 and the most bearish at RM0.33 per share. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or that the analysts have a clear view on its prospects.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Glomac Berhad's past performance and to peers in the same industry. For example, we noticed that Glomac Berhad's rate of growth is expected to accelerate meaningfully, with revenues forecast to exhibit 11% growth to the end of 2024 on an annualised basis. That is well above its historical decline of 0.9% a year over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in the industry are forecast to see their revenue grow 3.7% per year. So it looks like Glomac Berhad is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for this year. Fortunately, analysts also upgraded their revenue estimates, and our data indicates sales are expected to perform better than the wider market. Some investors might be disappointed to see that the price target is unchanged, but we feel that improving fundamentals are usually a positive - assuming these forecasts are met! So Glomac Berhad could be a good candidate for more research.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Glomac Berhad going out to 2026, and you can see them free on our platform here..

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:GLOMAC

Glomac Berhad

An investment holding company, engages in the property development business in Malaysia.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor