- Malaysia

- /

- Real Estate

- /

- KLSE:EUPE

Eupe Corporation Berhad (KLSE:EUPE) Is Increasing Its Dividend To MYR0.022

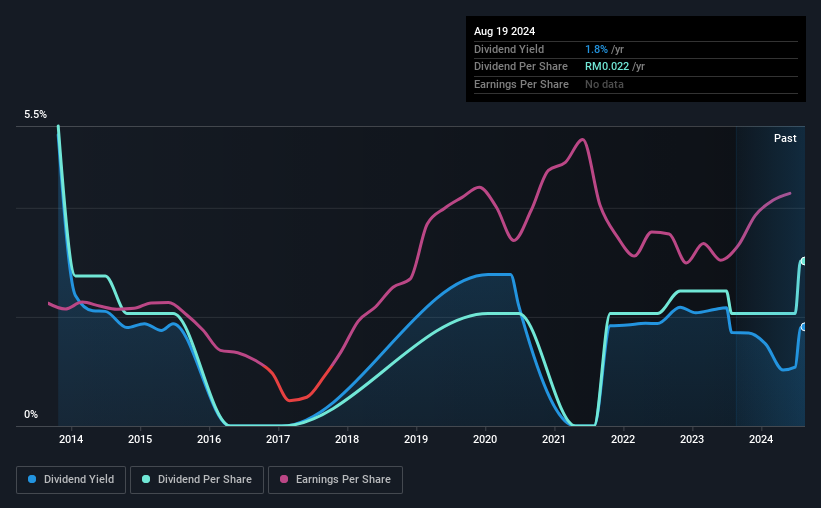

The board of Eupe Corporation Berhad (KLSE:EUPE) has announced that it will be increasing its dividend by 47% on the 11th of September to MYR0.022, up from last year's comparable payment of MYR0.015. This takes the annual payment to 1.8% of the current stock price, which unfortunately is below what the industry is paying.

Check out our latest analysis for Eupe Corporation Berhad

Eupe Corporation Berhad's Earnings Easily Cover The Distributions

Even a low dividend yield can be attractive if it is sustained for years on end. However, Eupe Corporation Berhad's earnings easily cover the dividend. This means that most of what the business earns is being used to help it grow.

EPS is set to fall by 0.4% over the next 12 months if recent trends continue. If the dividend continues along recent trends, we estimate the payout ratio could be 8.9%, which we consider to be quite comfortable, with most of the company's earnings left over to grow the business in the future.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. The annual payment during the last 10 years was MYR0.04 in 2014, and the most recent fiscal year payment was MYR0.022. Doing the maths, this is a decline of about 5.8% per year. Generally, we don't like to see a dividend that has been declining over time as this can degrade shareholders' returns and indicate that the company may be running into problems.

Eupe Corporation Berhad May Find It Hard To Grow The Dividend

Dividends have been going in the wrong direction, so we definitely want to see a different trend in the earnings per share. Although it's important to note that Eupe Corporation Berhad's earnings per share has basically not grown from where it was five years ago, which could erode the purchasing power of the dividend over time.

An additional note is that the company has been raising capital by issuing stock equal to 15% of shares outstanding in the last 12 months. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We would be a touch cautious of relying on this stock primarily for the dividend income.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. To that end, Eupe Corporation Berhad has 4 warning signs (and 1 which doesn't sit too well with us) we think you should know about. Is Eupe Corporation Berhad not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Eupe Corporation Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:EUPE

Eupe Corporation Berhad

An investment holding company, engages in the investment, development, construction, rental, and management of properties in Malaysia.

Good value with adequate balance sheet and pays a dividend.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)