Is Now An Opportune Moment To Examine SCGM Bhd (KLSE:SCGM)?

SCGM Bhd (KLSE:SCGM), might not be a large cap stock, but it received a lot of attention from a substantial price increase on the KLSE over the last few months. As a small cap stock, hardly covered by any analysts, there is generally more of an opportunity for mispricing as there is less activity to push the stock closer to fair value. Is there still an opportunity here to buy? Let’s take a look at SCGM Bhd’s outlook and value based on the most recent financial data to see if the opportunity still exists.

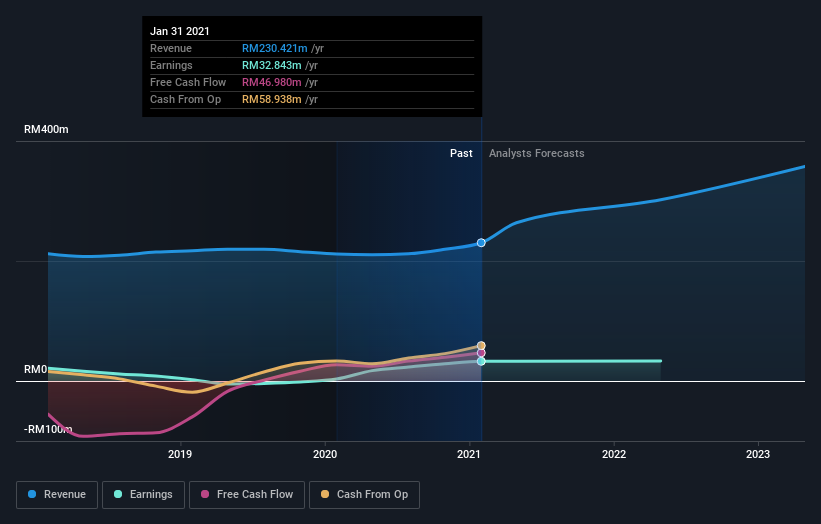

View our latest analysis for SCGM Bhd

What's the opportunity in SCGM Bhd?

The share price seems sensible at the moment according to my price multiple model, where I compare the company's price-to-earnings ratio to the industry average. In this instance, I’ve used the price-to-earnings (PE) ratio given that there is not enough information to reliably forecast the stock’s cash flows. I find that SCGM Bhd’s ratio of 12.61x is trading slightly below its industry peers’ ratio of 13.06x, which means if you buy SCGM Bhd today, you’d be paying a decent price for it. And if you believe SCGM Bhd should be trading in this range, then there isn’t much room for the share price to grow beyond the levels of other industry peers over the long-term. Furthermore, SCGM Bhd’s share price also seems relatively stable compared to the rest of the market, as indicated by its low beta. This may mean it is less likely for the stock to fall lower from natural market volatility, which suggests less opportunities to buy moving forward.

Can we expect growth from SCGM Bhd?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Buying a great company with a robust outlook at a cheap price is always a good investment, so let’s also take a look at the company's future expectations. Though in the case of SCGM Bhd, it is expected to deliver a relatively unexciting earnings growth of 1.6%, which doesn’t help build up its investment thesis. Growth doesn’t appear to be a main reason for a buy decision for SCGM Bhd, at least in the near term.

What this means for you:

Are you a shareholder? SCGM’s future growth appears to have been factored into the current share price, with shares trading around industry price multiples. However, there are also other important factors which we haven’t considered today, such as the track record of its management team. Have these factors changed since the last time you looked at SCGM? Will you have enough conviction to buy should the price fluctuate below the industry PE ratio?

Are you a potential investor? If you’ve been keeping an eye on SCGM, now may not be the most advantageous time to buy, given it is trading around industry price multiples. However, the positive growth outlook may mean it’s worth diving deeper into other factors in order to take advantage of the next price drop.

With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. In terms of investment risks, we've identified 1 warning sign with SCGM Bhd, and understanding it should be part of your investment process.

If you are no longer interested in SCGM Bhd, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:SCGM

Flawless balance sheet with low risk.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)