Advertisement

DXN Holdings Bhd.'s (KLSE:DXN) investors are due to receive a payment of MYR0.009 per share on 29th of August. This means the annual payment is 7.3% of the current stock price, which is above the average for the industry.

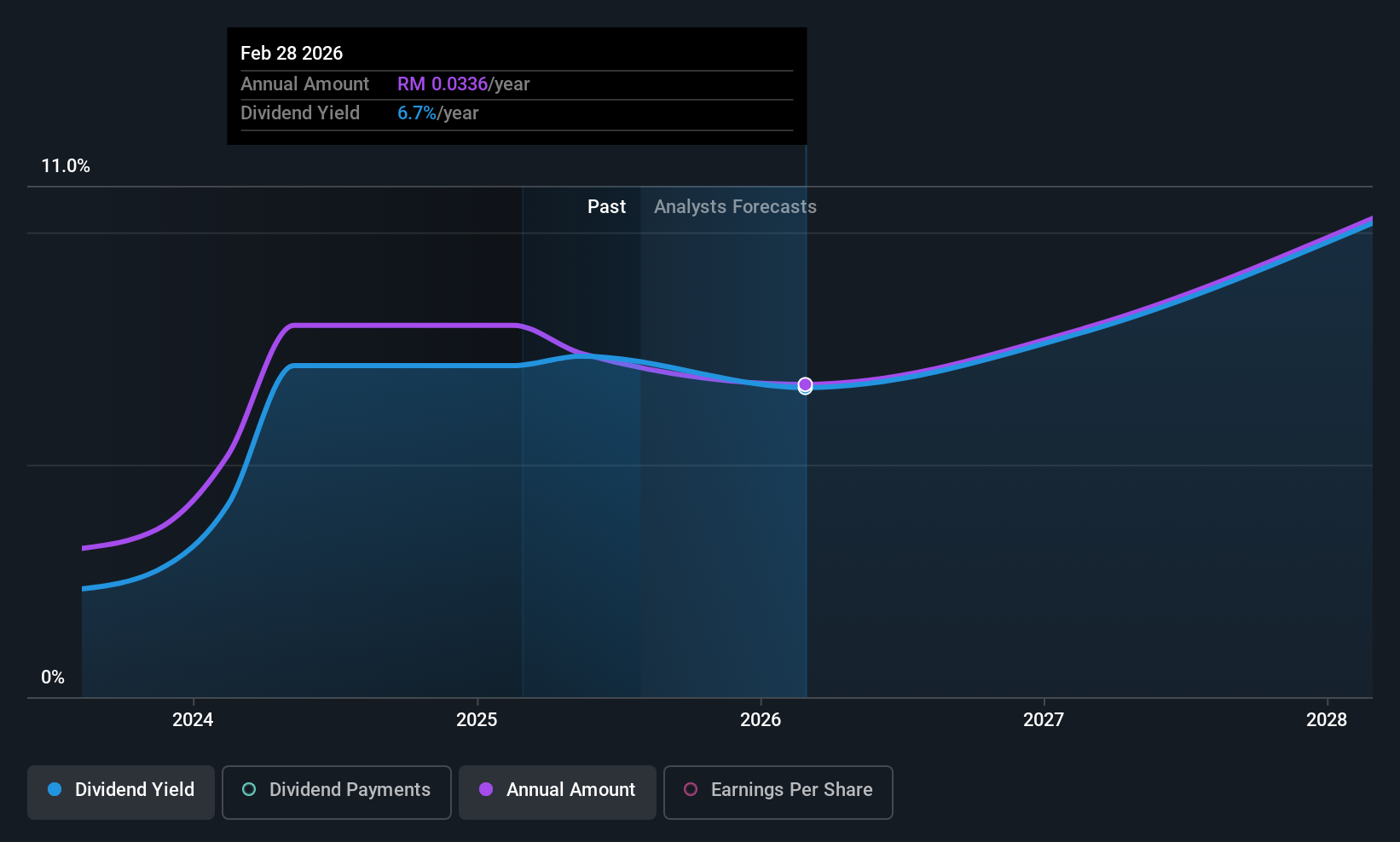

DXN Holdings Bhd's Payment Could Potentially Have Solid Earnings Coverage

If the payments aren't sustainable, a high yield for a few years won't matter that much. Prior to this announcement, DXN Holdings Bhd was quite comfortably covering its dividend with earnings and it was paying more than 75% of its free cash flow to shareholders. By paying out so much of its cash flows, this could indicate that the company has limited opportunities for investment and growth.

The next year is set to see EPS grow by 49.6%. Assuming the dividend continues along recent trends, we think the payout ratio could be 7.3% by next year, which is in a pretty sustainable range.

See our latest analysis for DXN Holdings Bhd

DXN Holdings Bhd Is Still Building Its Track Record

The dividend hasn't seen any major cuts in the past, but the company has only been paying a dividend for 2 years, which isn't that long in the grand scheme of things. Since 2023, the dividend has gone from MYR0.016 total annually to MYR0.037. This implies that the company grew its distributions at a yearly rate of about 52% over that duration. We're not overly excited about the relatively short history of dividend payments, however the dividend is growing at a nice rate and we might take a closer look.

Dividend Growth May Be Hard To Achieve

Investors could be attracted to the stock based on the quality of its payment history. Earnings have grown at around 4.9% a year for the past five years, which isn't massive but still better than seeing them shrink. The company has been growing at a pretty soft 4.9% per annum, and is paying out quite a lot of its earnings to shareholders. This could mean the dividend doesn't have the growth potential we look for going into the future.

Our Thoughts On DXN Holdings Bhd's Dividend

Overall, we don't think this company makes a great dividend stock, even though the dividend wasn't cut this year. The low payout ratio is a redeeming feature, but generally we are not too happy with the payments DXN Holdings Bhd has been making. This company is not in the top tier of income providing stocks.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Earnings growth generally bodes well for the future value of company dividend payments. See if the 3 DXN Holdings Bhd analysts we track are forecasting continued growth with our free report on analyst estimates for the company. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:DXN

DXN Holdings Bhd

Manufactures and sales health supplements and other products on direct sales basis in Latin America, Malaysia, Asia, North America, Africa, Europe, the Middle East, and Oceania.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|33.9% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|26.5% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.3% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor