Advertisement

- Malaysia

- /

- Medical Equipment

- /

- KLSE:HARTA

Need To Know: Analysts Just Made A Substantial Cut To Their Hartalega Holdings Berhad (KLSE:HARTA) Estimates

Today is shaping up negative for Hartalega Holdings Berhad (KLSE:HARTA) shareholders, with the analysts delivering a substantial negative revision to this year's forecasts. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting the analysts have soured majorly on the business.

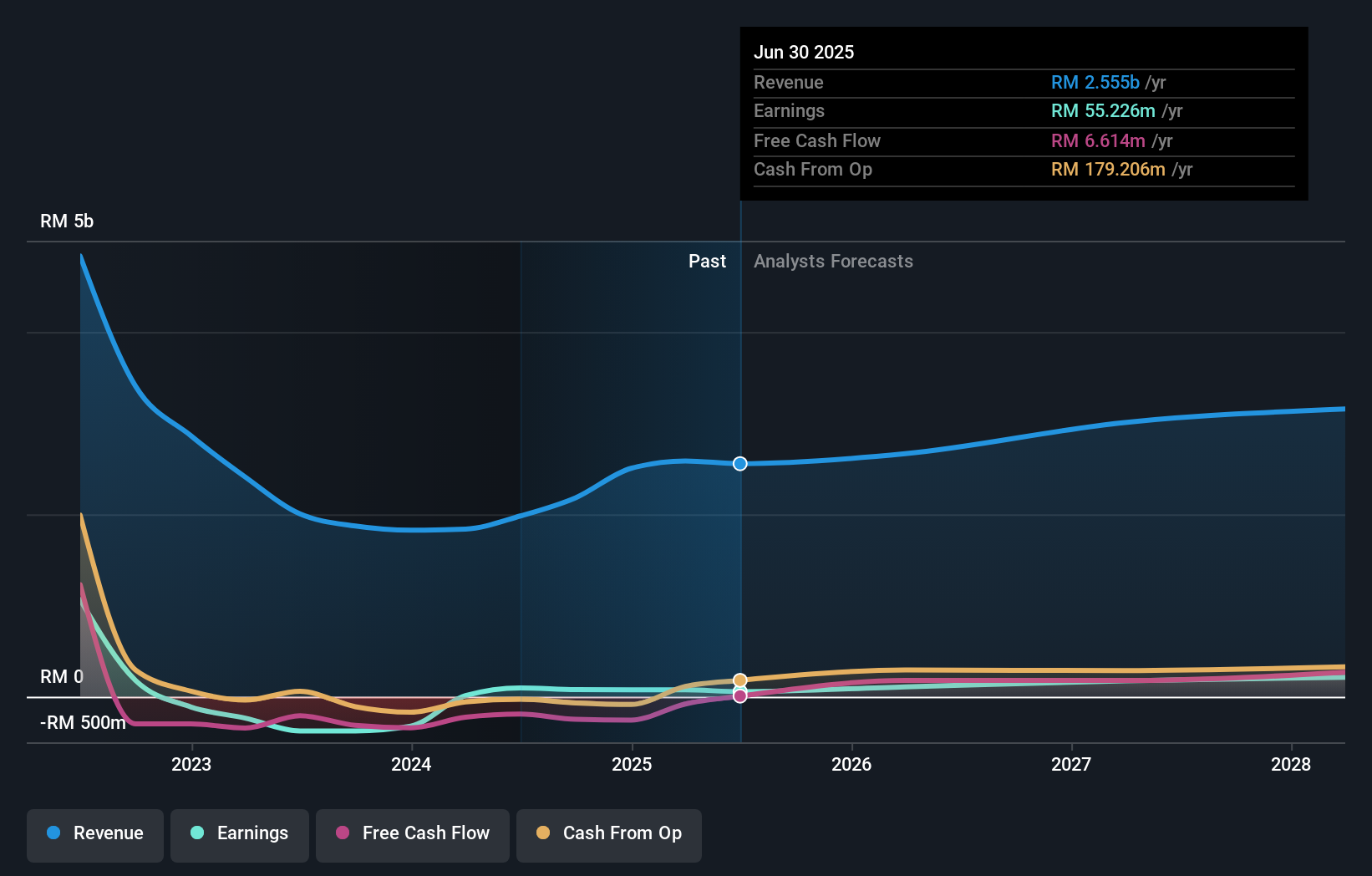

After the downgrade, the 19 analysts covering Hartalega Holdings Berhad are now predicting revenues of RM2.7b in 2026. If met, this would reflect an okay 4.3% improvement in sales compared to the last 12 months. Per-share earnings are expected to soar 94% to RM0.031. Previously, the analysts had been modelling revenues of RM3.0b and earnings per share (EPS) of RM0.045 in 2026. Indeed, we can see that the analysts are a lot more bearish about Hartalega Holdings Berhad's prospects, administering a measurable cut to revenue estimates and slashing their EPS estimates to boot.

View our latest analysis for Hartalega Holdings Berhad

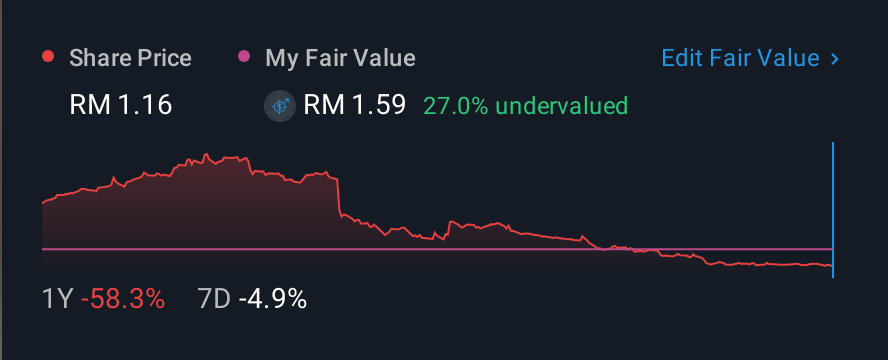

It'll come as no surprise then, to learn that the analysts have cut their price target 29% to RM1.63.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. For example, we noticed that Hartalega Holdings Berhad's rate of growth is expected to accelerate meaningfully, with revenues forecast to exhibit 4.3% growth to the end of 2026 on an annualised basis. That is well above its historical decline of 26% a year over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 12% per year. Although Hartalega Holdings Berhad's revenues are expected to improve, it seems that the analysts are still bearish on the business, forecasting it to grow slower than the broader industry.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for Hartalega Holdings Berhad. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that Hartalega Holdings Berhad's revenues are expected to grow slower than the wider market. Given the scope of the downgrades, it would not be a surprise to see the market become more wary of the business.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. At Simply Wall St, we have a full range of analyst estimates for Hartalega Holdings Berhad going out to 2028, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies backed by insiders.

Valuation is complex, but we're here to simplify it.

Discover if Hartalega Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:HARTA

Hartalega Holdings Berhad

An investment holding company, engages in the manufacture, retail, and wholesale of latex and nitrile gloves in Malaysia, North America, Europe, Asia, Australia, the Middle East, and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|32.6% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.6% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|1.6% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.2% undervalued

RO

Community Contributor