Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Comfort Gloves Berhad (KLSE:COMFORT) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Comfort Gloves Berhad

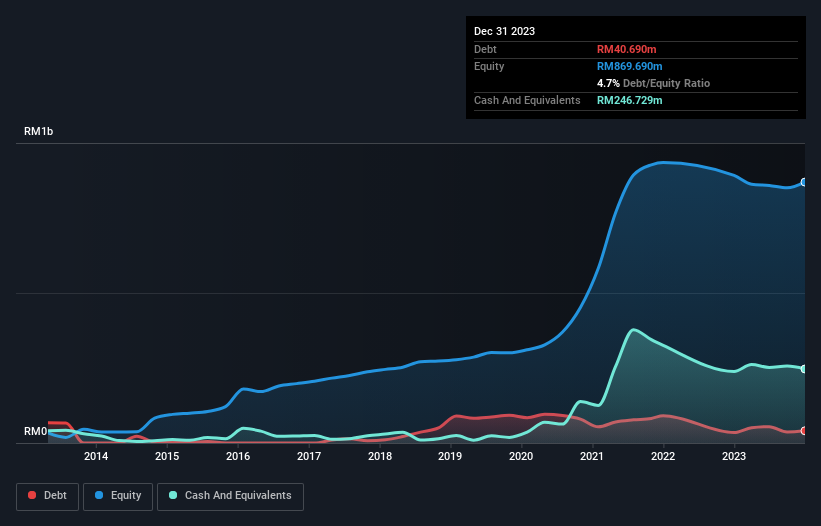

How Much Debt Does Comfort Gloves Berhad Carry?

You can click the graphic below for the historical numbers, but it shows that as of December 2023 Comfort Gloves Berhad had RM40.7m of debt, an increase on RM34.7m, over one year. However, it does have RM246.7m in cash offsetting this, leading to net cash of RM206.0m.

How Healthy Is Comfort Gloves Berhad's Balance Sheet?

The latest balance sheet data shows that Comfort Gloves Berhad had liabilities of RM79.4m due within a year, and liabilities of RM11.6m falling due after that. Offsetting this, it had RM246.7m in cash and RM152.5m in receivables that were due within 12 months. So it actually has RM308.2m more liquid assets than total liabilities.

This surplus liquidity suggests that Comfort Gloves Berhad's balance sheet could take a hit just as well as Homer Simpson's head can take a punch. On this view, lenders should feel as safe as the beloved of a black-belt karate master. Succinctly put, Comfort Gloves Berhad boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Comfort Gloves Berhad will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Comfort Gloves Berhad had a loss before interest and tax, and actually shrunk its revenue by 46%, to RM326m. That makes us nervous, to say the least.

So How Risky Is Comfort Gloves Berhad?

While Comfort Gloves Berhad lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow RM111k. So although it is loss-making, it doesn't seem to have too much near-term balance sheet risk, keeping in mind the net cash. The next few years will be important as the business matures. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 2 warning signs for Comfort Gloves Berhad you should be aware of, and 1 of them shouldn't be ignored.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:COMFORT

Comfort Gloves Berhad

An investment holding company, manufactures and trades in nitrile and latex gloves in Malaysia, the United States, Canada, Asia, Europe, and internationally.

Adequate balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|28.9% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|46.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|33.9% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|56.1% undervalued

AX

Community Contributor