- Malaysia

- /

- Food and Staples Retail

- /

- KLSE:SUPREME

Earnings Troubles May Signal Larger Issues for Supreme Consolidated Resources Berhad (KLSE:SUPREME) Shareholders

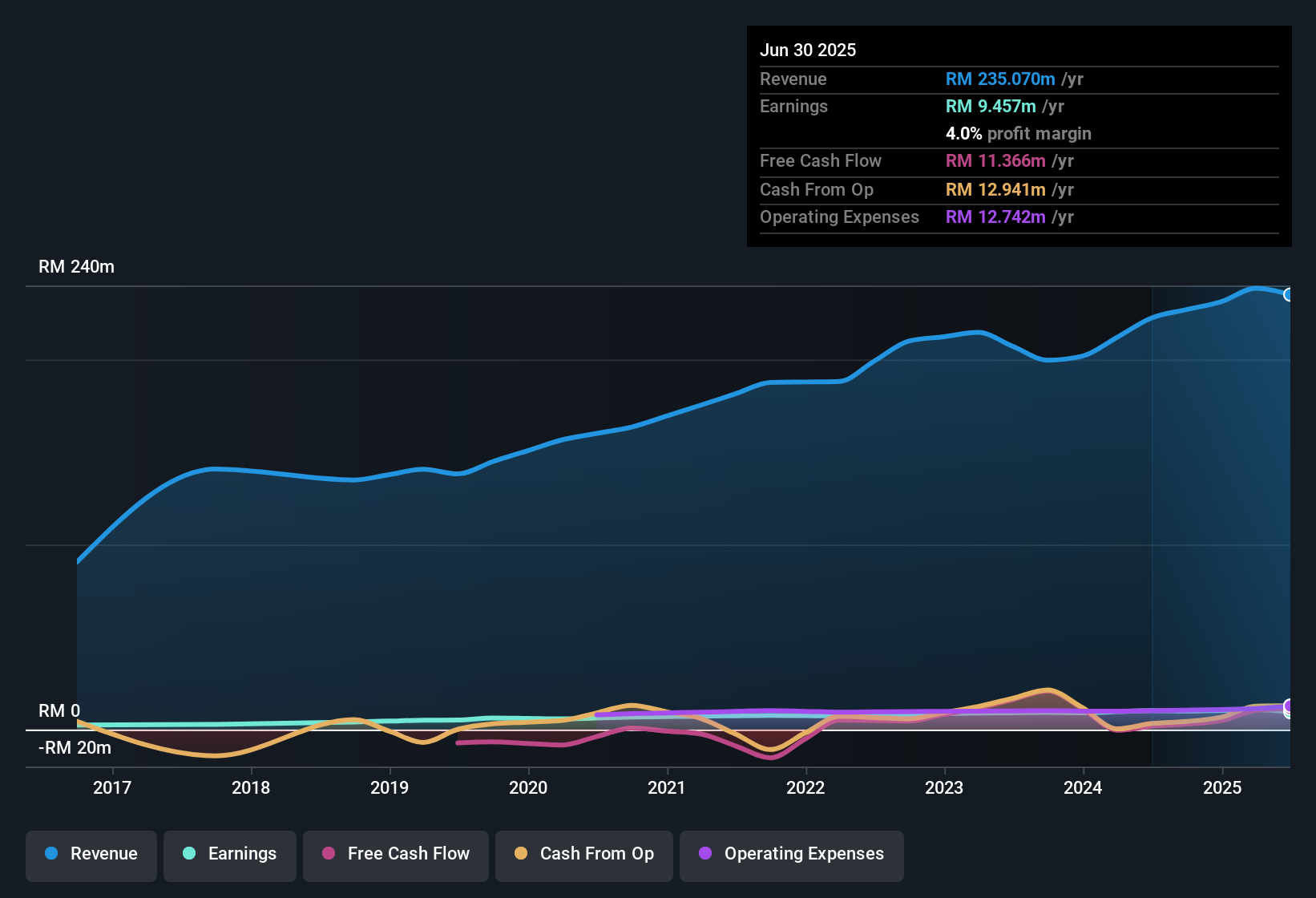

The subdued market reaction suggests that Supreme Consolidated Resources Berhad's (KLSE:SUPREME) recent earnings didn't contain any surprises. However, we believe that investors should be aware of some underlying factors which may be of concern.

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. In fact, Supreme Consolidated Resources Berhad increased the number of shares on issue by 19% over the last twelve months by issuing new shares. That means its earnings are split among a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. Check out Supreme Consolidated Resources Berhad's historical EPS growth by clicking on this link.

A Look At The Impact Of Supreme Consolidated Resources Berhad's Dilution On Its Earnings Per Share (EPS)

Supreme Consolidated Resources Berhad has improved its profit over the last three years, with an annualized gain of 22% in that time. But on the other hand, earnings per share actually fell by 2.2% per year. Net income was down 7.7% over the last twelve months. But the EPS result was even worse, with the company recording a decline of 22%. Therefore, the dilution is having a noteworthy influence on shareholder returns.

In the long term, if Supreme Consolidated Resources Berhad's earnings per share can increase, then the share price should too. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Supreme Consolidated Resources Berhad.

Our Take On Supreme Consolidated Resources Berhad's Profit Performance

Over the last year Supreme Consolidated Resources Berhad issued new shares and so, there's a noteworthy divergence between EPS and net income growth. Because of this, we think that it may be that Supreme Consolidated Resources Berhad's statutory profits are better than its underlying earnings power. In further bad news, its earnings per share decreased in the last year. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. For example, we've discovered 3 warning signs that you should run your eye over to get a better picture of Supreme Consolidated Resources Berhad.

This note has only looked at a single factor that sheds light on the nature of Supreme Consolidated Resources Berhad's profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:SUPREME

Supreme Consolidated Resources Berhad

An investment holding company, imports, trades in, and distributes frozen, chilled, dairy, and dry food products in Malaysia.

Excellent balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)