Advertisement

- Malaysia

- /

- Food and Staples Retail

- /

- KLSE:SEM

7-Eleven Malaysia Holdings Berhad Earnings Missed Analyst Estimates: Here's What Analysts Are Forecasting Now

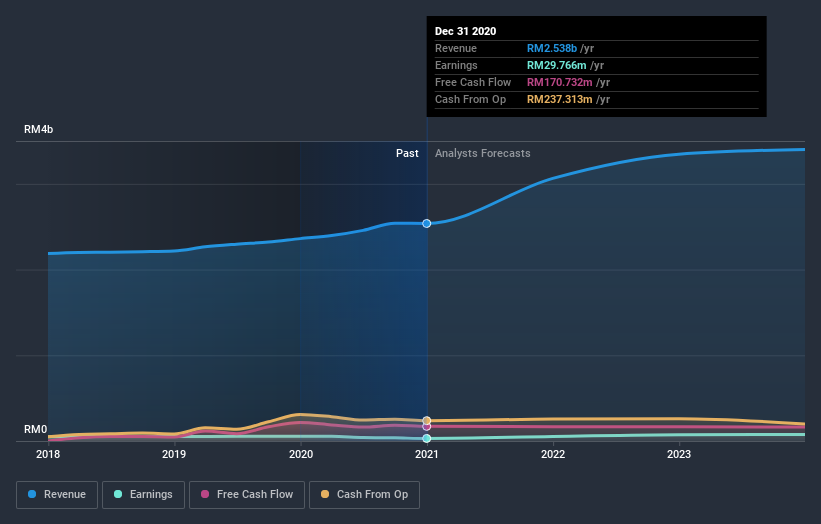

7-Eleven Malaysia Holdings Berhad (KLSE:SEM) missed earnings with its latest full-year results, disappointing overly-optimistic forecasters. It wasn't a great result overall - while revenue fell marginally short of analyst estimates at RM2.5b, statutory earnings missed forecasts by an incredible 48%, coming in at just RM0.026 per share. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

View our latest analysis for 7-Eleven Malaysia Holdings Berhad

Following the latest results, 7-Eleven Malaysia Holdings Berhad's five analysts are now forecasting revenues of RM3.06b in 2021. This would be a huge 21% improvement in sales compared to the last 12 months. Statutory earnings per share are predicted to shoot up 77% to RM0.046. Before this earnings report, the analysts had been forecasting revenues of RM3.06b and earnings per share (EPS) of RM0.059 in 2021. So there's definitely been a decline in sentiment after the latest results, noting the large cut to new EPS forecasts.

The consensus price target held steady at RM1.60, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values 7-Eleven Malaysia Holdings Berhad at RM2.00 per share, while the most bearish prices it at RM1.30. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's clear from the latest estimates that 7-Eleven Malaysia Holdings Berhad's rate of growth is expected to accelerate meaningfully, with the forecast 21% revenue growth noticeably faster than its historical growth of 4.4%p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 10% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect 7-Eleven Malaysia Holdings Berhad to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for 7-Eleven Malaysia Holdings Berhad. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple 7-Eleven Malaysia Holdings Berhad analysts - going out to 2023, and you can see them free on our platform here.

However, before you get too enthused, we've discovered 3 warning signs for 7-Eleven Malaysia Holdings Berhad (1 is significant!) that you should be aware of.

If you’re looking to trade 7-Eleven Malaysia Holdings Berhad, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:SEM

7-Eleven Malaysia Holdings Berhad

An investment holding company, owns, operates, and franchises a chain of convenience stores under the 7-Eleven brand in Malaysia.

Reasonable growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor