Advertisement

- Malaysia

- /

- Consumer Durables

- /

- KLSE:TCS

These 4 Measures Indicate That TCS Group Holdings Berhad (KLSE:TCS) Is Using Debt Reasonably Well

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, TCS Group Holdings Berhad (KLSE:TCS) does carry debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

How Much Debt Does TCS Group Holdings Berhad Carry?

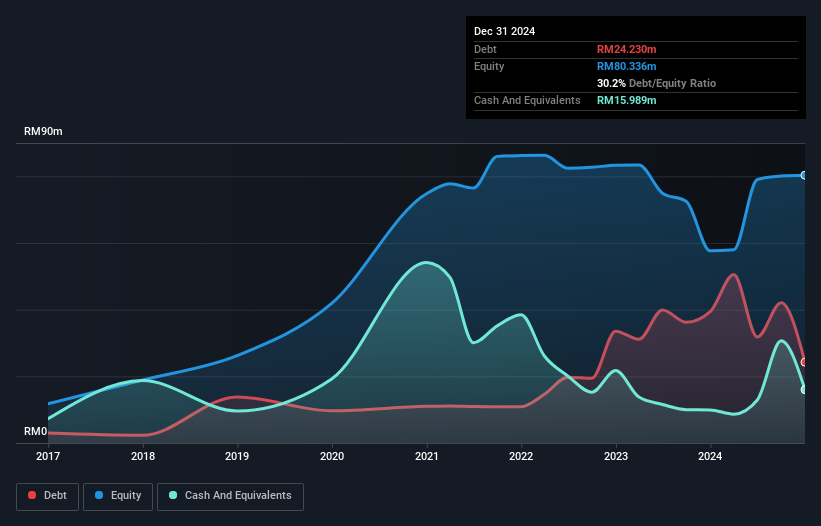

As you can see below, TCS Group Holdings Berhad had RM24.2m of debt at December 2024, down from RM39.4m a year prior. However, it does have RM16.0m in cash offsetting this, leading to net debt of about RM8.24m.

How Healthy Is TCS Group Holdings Berhad's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that TCS Group Holdings Berhad had liabilities of RM152.3m due within 12 months and liabilities of RM13.2m due beyond that. On the other hand, it had cash of RM16.0m and RM186.9m worth of receivables due within a year. So it can boast RM37.3m more liquid assets than total liabilities.

This surplus strongly suggests that TCS Group Holdings Berhad has a rock-solid balance sheet (and the debt is of no concern whatsoever). On this view, lenders should feel as safe as the beloved of a black-belt karate master.

Check out our latest analysis for TCS Group Holdings Berhad

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

TCS Group Holdings Berhad has a very low debt to EBITDA ratio of 0.68 so it is strange to see weak interest coverage, with last year's EBIT being only 1.2 times the interest expense. So one way or the other, it's clear the debt levels are not trivial. We also note that TCS Group Holdings Berhad improved its EBIT from a last year's loss to a positive RM4.3m. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since TCS Group Holdings Berhad will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot .

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. In the last year, TCS Group Holdings Berhad's free cash flow amounted to 34% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

Happily, TCS Group Holdings Berhad's impressive level of total liabilities implies it has the upper hand on its debt. But the stark truth is that we are concerned by its interest cover. All these things considered, it appears that TCS Group Holdings Berhad can comfortably handle its current debt levels. On the plus side, this leverage can boost shareholder returns, but the potential downside is more risk of loss, so it's worth monitoring the balance sheet. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 2 warning signs for TCS Group Holdings Berhad you should be aware of, and 1 of them makes us a bit uncomfortable.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if TCS Group Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:TCS

TCS Group Holdings Berhad

An investment holding company, provides construction services for buildings, infrastructure, civil, and structural works in Malaysia.

Mediocre balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|20.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor