Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Ta Win Holdings Berhad (KLSE:TAWIN) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Ta Win Holdings Berhad

What Is Ta Win Holdings Berhad's Net Debt?

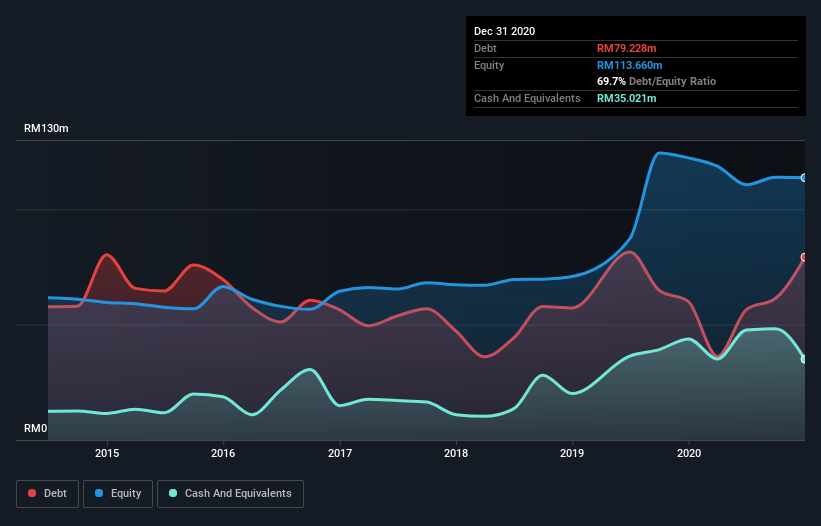

As you can see below, at the end of December 2020, Ta Win Holdings Berhad had RM79.2m of debt, up from RM60.0m a year ago. Click the image for more detail. However, it also had RM35.0m in cash, and so its net debt is RM44.2m.

How Healthy Is Ta Win Holdings Berhad's Balance Sheet?

The latest balance sheet data shows that Ta Win Holdings Berhad had liabilities of RM107.3m due within a year, and liabilities of RM7.70m falling due after that. On the other hand, it had cash of RM35.0m and RM62.3m worth of receivables due within a year. So its liabilities total RM17.7m more than the combination of its cash and short-term receivables.

Given Ta Win Holdings Berhad has a market capitalization of RM123.6m, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. When analysing debt levels, the balance sheet is the obvious place to start. But it is Ta Win Holdings Berhad's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Ta Win Holdings Berhad had a loss before interest and tax, and actually shrunk its revenue by 12%, to RM307m. We would much prefer see growth.

Caveat Emptor

While Ta Win Holdings Berhad's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Its EBIT loss was a whopping RM14m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through RM23m of cash over the last year. So in short it's a really risky stock. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 4 warning signs we've spotted with Ta Win Holdings Berhad (including 2 which can't be ignored) .

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Ta Win Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:TAWIN

Ta Win Holdings Berhad

An investment holding company, manufactures, sells, and trades in copper wires, rods, and related products in Malaysia, Brunei, Hong Kong, China, Vietnam, and internationally.

Adequate balance sheet low.

Market Insights

Community Narratives