Advertisement

- Malaysia

- /

- Construction

- /

- KLSE:SYCAL

Sycal Ventures Berhad's (KLSE:SYCAL) P/E Still Appears To Be Reasonable

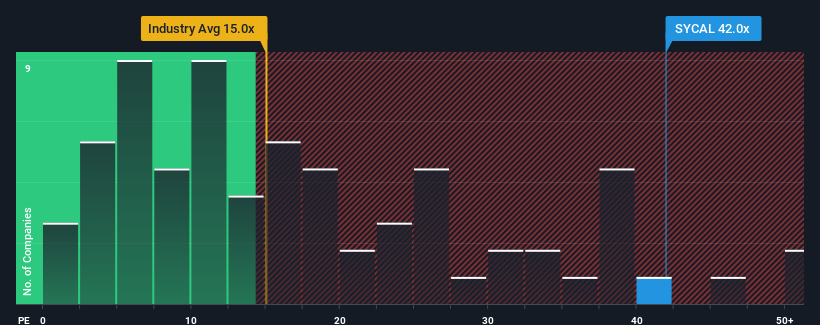

When close to half the companies in Malaysia have price-to-earnings ratios (or "P/E's") below 13x, you may consider Sycal Ventures Berhad (KLSE:SYCAL) as a stock to avoid entirely with its 42x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

With earnings growth that's exceedingly strong of late, Sycal Ventures Berhad has been doing very well. The P/E is probably high because investors think this strong earnings growth will be enough to outperform the broader market in the near future. If not, then existing shareholders might be a little nervous about the viability of the share price.

See our latest analysis for Sycal Ventures Berhad

Does Growth Match The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Sycal Ventures Berhad's to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 98% last year. Pleasingly, EPS has also lifted 81% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Comparing that to the market, which is only predicted to deliver 16% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised earnings results.

In light of this, it's understandable that Sycal Ventures Berhad's P/E sits above the majority of other companies. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Key Takeaway

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Sycal Ventures Berhad revealed its three-year earnings trends are contributing to its high P/E, given they look better than current market expectations. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless the recent medium-term conditions change, they will continue to provide strong support to the share price.

And what about other risks? Every company has them, and we've spotted 3 warning signs for Sycal Ventures Berhad (of which 1 is concerning!) you should know about.

If these risks are making you reconsider your opinion on Sycal Ventures Berhad, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:SYCAL

Sycal Ventures Berhad

An investment holding company, operates as a contractor for building, infrastructure, and civil construction works in Malaysia.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.1% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|22.0% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.6% undervalued

RO

Community Contributor