- Malaysia

- /

- Trade Distributors

- /

- KLSE:PANSAR

These 4 Measures Indicate That Pansar Berhad (KLSE:PANSAR) Is Using Debt Reasonably Well

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Pansar Berhad (KLSE:PANSAR) makes use of debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Pansar Berhad

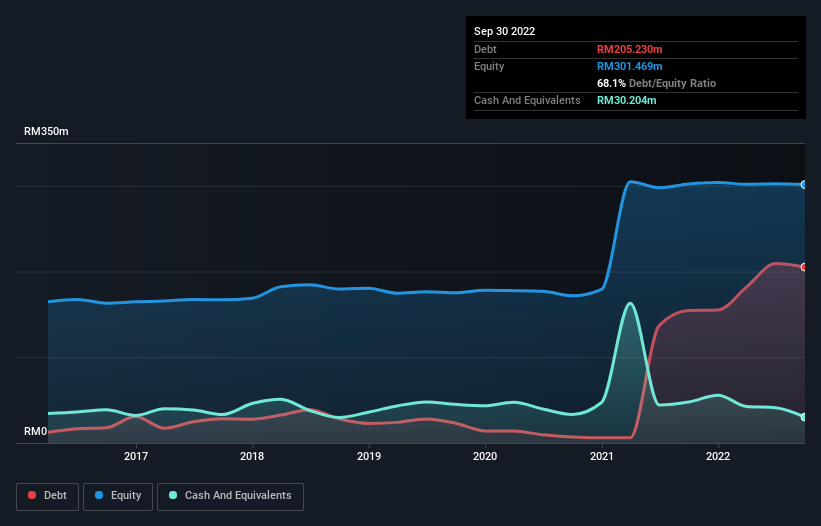

How Much Debt Does Pansar Berhad Carry?

You can click the graphic below for the historical numbers, but it shows that as of September 2022 Pansar Berhad had RM205.2m of debt, an increase on RM154.6m, over one year. However, it does have RM30.2m in cash offsetting this, leading to net debt of about RM175.0m.

How Strong Is Pansar Berhad's Balance Sheet?

We can see from the most recent balance sheet that Pansar Berhad had liabilities of RM306.8m falling due within a year, and liabilities of RM34.2m due beyond that. Offsetting this, it had RM30.2m in cash and RM380.7m in receivables that were due within 12 months. So it actually has RM69.9m more liquid assets than total liabilities.

This excess liquidity suggests that Pansar Berhad is taking a careful approach to debt. Given it has easily adequate short term liquidity, we don't think it will have any issues with its lenders.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Weak interest cover of 1.5 times and a disturbingly high net debt to EBITDA ratio of 10.8 hit our confidence in Pansar Berhad like a one-two punch to the gut. This means we'd consider it to have a heavy debt load. The good news is that Pansar Berhad grew its EBIT a smooth 69% over the last twelve months. Like the milk of human kindness that sort of growth increases resilience, making the company more capable of managing debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is Pansar Berhad's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the last two years, Pansar Berhad saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

Pansar Berhad's conversion of EBIT to free cash flow was a real negative on this analysis, as was its net debt to EBITDA. But like a ballerina ending on a perfect pirouette, it has not trouble growing its EBIT. When we consider all the factors mentioned above, we do feel a bit cautious about Pansar Berhad's use of debt. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 5 warning signs for Pansar Berhad (2 make us uncomfortable) you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:PANSAR

Pansar Berhad

Sells and distributes building materials, marine and industrial products, agro-engineering equipment and supplies, and electrical and office automation supplies in Malaysia and Singapore.

Good value with proven track record.

Similar Companies

Market Insights

Community Narratives