- Malaysia

- /

- Construction

- /

- KLSE:GDB

GDB Holdings Berhad's (KLSE:GDB) Fundamentals Look Pretty Strong: Could The Market Be Wrong About The Stock?

It is hard to get excited after looking at GDB Holdings Berhad's (KLSE:GDB) recent performance, when its stock has declined 7.1% over the past three months. However, a closer look at its sound financials might cause you to think again. Given that fundamentals usually drive long-term market outcomes, the company is worth looking at. Specifically, we decided to study GDB Holdings Berhad's ROE in this article.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Put another way, it reveals the company's success at turning shareholder investments into profits.

See our latest analysis for GDB Holdings Berhad

How Do You Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for GDB Holdings Berhad is:

23% = RM29m ÷ RM123m (Based on the trailing twelve months to December 2019).

The 'return' is the profit over the last twelve months. That means that for every MYR1 worth of shareholders' equity, the company generated MYR0.23 in profit.

Why Is ROE Important For Earnings Growth?

Thus far, we have learnt that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

GDB Holdings Berhad's Earnings Growth And 23% ROE

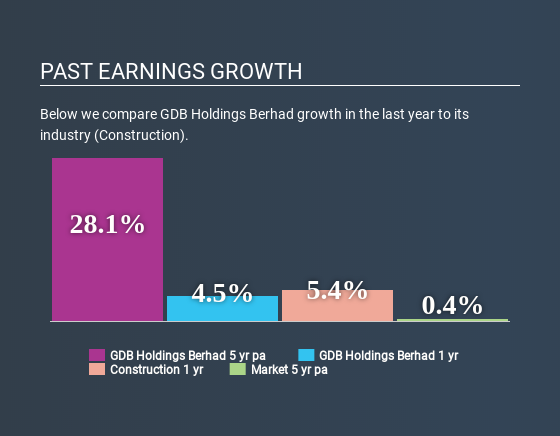

At first glance, GDB Holdings Berhad seems to have a decent ROE. Further, the company's ROE compares quite favorably to the industry average of 6.3%. This probably laid the ground for GDB Holdings Berhad's significant 28% net income growth seen over the past five years. We reckon that there could also be other factors at play here. For instance, the company has a low payout ratio or is being managed efficiently.

As a next step, we compared GDB Holdings Berhad's net income growth with the industry, and pleasingly, we found that the growth seen by the company is higher than the average industry growth of 0.2%.

Earnings growth is a huge factor in stock valuation. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. This then helps them determine if the stock is placed for a bright or bleak future. If you're wondering about GDB Holdings Berhad's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is GDB Holdings Berhad Using Its Retained Earnings Effectively?

GDB Holdings Berhad's three-year median payout ratio is a pretty moderate 47%, meaning the company retains 53% of its income. So it seems that GDB Holdings Berhad is reinvesting efficiently in a way that it sees impressive growth in its earnings (discussed above) and pays a dividend that's well covered.

While GDB Holdings Berhad has seen growth in its earnings, it only recently started to pay a dividend. It is most likely that the company decided to impress new and existing shareholders with a dividend. Our latest analyst data shows that the future payout ratio of the company is expected to drop to 33% over the next three years.

Conclusion

On the whole, we feel that GDB Holdings Berhad's performance has been quite good. Specifically, we like that the company is reinvesting a huge chunk of its profits at a high rate of return. This of course has caused the company to see substantial growth in its earnings. If the company continues to grow its earnings the way it has, that could have a positive impact on its share price given how earnings per share influence long-term share prices. Remember, the price of a stock is also dependent on the perceived risk. Therefore investors must keep themselves informed about the risks involved before investing in any company. To know the 4 risks we have identified for GDB Holdings Berhad visit our risks dashboard for free.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About KLSE:GDB

GDB Holdings Berhad

An investment holding company, engages in the provision of construction services in Malaysia.

Flawless balance sheet and undervalued.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)