- Malaysia

- /

- Construction

- /

- KLSE:CRESBLD

We Think Some Shareholders May Hesitate To Increase Crest Builder Holdings Berhad's (KLSE:CRESBLD) CEO Compensation

Key Insights

- Crest Builder Holdings Berhad to hold its Annual General Meeting on 29th of May

- Total pay for CEO Eric Yong includes RM534.0k salary

- The total compensation is similar to the average for the industry

- Over the past three years, Crest Builder Holdings Berhad's EPS grew by 43% and over the past three years, the total loss to shareholders 10%

In the past three years, the share price of Crest Builder Holdings Berhad (KLSE:CRESBLD) has struggled to generate growth for its shareholders. Despite positive EPS growth in the past few years, the share price hasn't tracked the fundamental performance of the company. The AGM coming up on the 29th of May could be an opportunity for shareholders to bring these concerns to the board's attention. They could also try to influence management and firm direction through voting on resolutions such as executive remuneration and other company matters. Here's our take on why we think shareholders may want to be cautious of approving a raise for the CEO at the moment.

Check out our latest analysis for Crest Builder Holdings Berhad

How Does Total Compensation For Eric Yong Compare With Other Companies In The Industry?

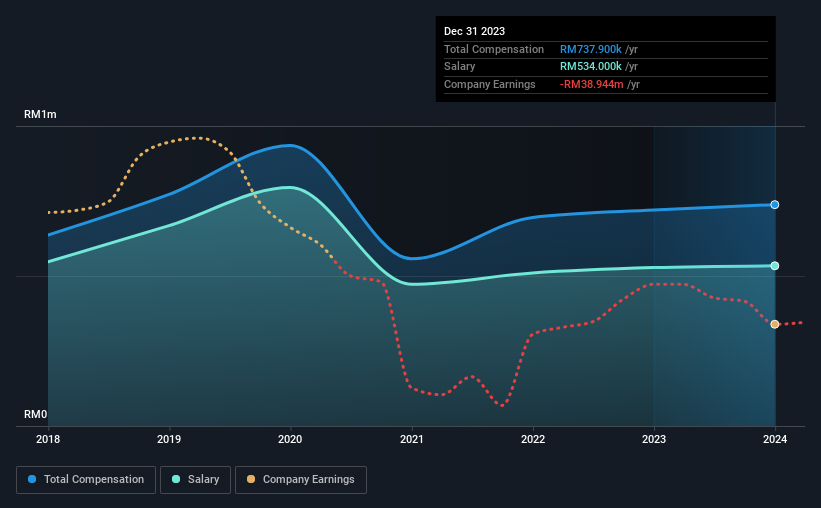

Our data indicates that Crest Builder Holdings Berhad has a market capitalization of RM91m, and total annual CEO compensation was reported as RM738k for the year to December 2023. This means that the compensation hasn't changed much from last year. We note that the salary portion, which stands at RM534.0k constitutes the majority of total compensation received by the CEO.

In comparison with other companies in the Malaysian Construction industry with market capitalizations under RM939m, the reported median total CEO compensation was RM725k. So it looks like Crest Builder Holdings Berhad compensates Eric Yong in line with the median for the industry.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | RM534k | RM528k | 72% |

| Other | RM204k | RM192k | 28% |

| Total Compensation | RM738k | RM720k | 100% |

On an industry level, around 77% of total compensation represents salary and 23% is other remuneration. Our data reveals that Crest Builder Holdings Berhad allocates salary more or less in line with the wider market. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Crest Builder Holdings Berhad's Growth Numbers

Over the past three years, Crest Builder Holdings Berhad has seen its earnings per share (EPS) grow by 43% per year. It achieved revenue growth of 40% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's great to see that revenue growth is strong, too. These metrics suggest the business is growing strongly. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Crest Builder Holdings Berhad Been A Good Investment?

Given the total shareholder loss of 10% over three years, many shareholders in Crest Builder Holdings Berhad are probably rather dissatisfied, to say the least. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

In Summary...

The fact that shareholders are sitting on a loss on the value of their shares in the past few years is certainly disconcerting. The stock's movement is disjointed with the company's earnings growth, which ideally should move in the same direction. Shareholders would be keen to know what's holding the stock back when earnings have grown. These concerns should be addressed at the upcoming AGM, where shareholders can question the board and evaluate if their judgement and decision making is still in line with their expectations.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. We did our research and identified 3 warning signs (and 2 which are significant) in Crest Builder Holdings Berhad we think you should know about.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:CRESBLD

Crest Builder Holdings Berhad

An investment holding company, operates as a construction, and mechanical and electrical (M&E) engineering contractor in Malaysia.

Good value with acceptable track record.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion