Advertisement

- Malaysia

- /

- Construction

- /

- KLSE:BPURI

We Think Bina Puri Holdings Bhd's (KLSE:BPURI) CEO Compensation Package Needs To Be Put Under A Microscope

The results at Bina Puri Holdings Bhd (KLSE:BPURI) have been quite disappointing recently and CEO Hock Tee bears some responsibility for this. Shareholders can take the chance to hold the board and management accountable for the unsatisfactory performance at the next AGM on 05 December 2022. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. We present the case why we think CEO compensation is out of sync with company performance.

Check out the opportunities and risks within the MY Construction industry.

How Does Total Compensation For Hock Tee Compare With Other Companies In The Industry?

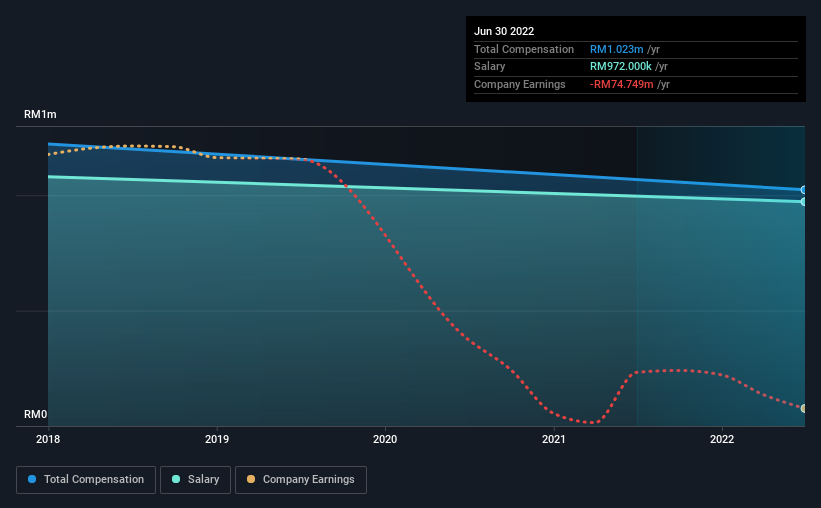

At the time of writing, our data shows that Bina Puri Holdings Bhd has a market capitalization of RM56m, and reported total annual CEO compensation of RM1.0m for the year to June 2022. There was no change in the compensation compared to last year. In particular, the salary of RM972.0k, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the industry with market capitalizations below RM896m, reported a median total CEO compensation of RM695k. Hence, we can conclude that Hock Tee is remunerated higher than the industry median. Moreover, Hock Tee also holds RM4.5m worth of Bina Puri Holdings Bhd stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2022 | 2022 | Proportion (2022) |

| Salary | RM972k | RM972k | 95% |

| Other | RM51k | RM51k | 5% |

| Total Compensation | RM1.0m | RM1.0m | 100% |

Speaking on an industry level, nearly 84% of total compensation represents salary, while the remainder of 16% is other remuneration. Bina Puri Holdings Bhd pays out 95% of remuneration in the form of a salary, significantly higher than the industry average. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

Bina Puri Holdings Bhd's Growth

Bina Puri Holdings Bhd has reduced its earnings per share by 8.2% a year over the last three years. In the last year, its revenue is down 18%.

Overall this is not a very positive result for shareholders. And the fact that revenue is down year on year arguably paints an ugly picture. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Bina Puri Holdings Bhd Been A Good Investment?

With a total shareholder return of -65% over three years, Bina Puri Holdings Bhd shareholders would by and large be disappointed. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Given that shareholders haven't seen any positive returns on their investment, not to mention the lack of earnings growth, this may suggest that few of them would be willing to award the CEO with a pay rise. At the upcoming AGM, they can question the management's plans and strategies to turn performance around and reassess their investment thesis in regards to the company.

CEO pay is simply one of the many factors that need to be considered while examining business performance. That's why we did our research, and identified 3 warning signs for Bina Puri Holdings Bhd (of which 2 are potentially serious!) that you should know about in order to have a holistic understanding of the stock.

Switching gears from Bina Puri Holdings Bhd, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if Bina Puri Holdings Bhd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:BPURI

Bina Puri Holdings Bhd

An investment holding company, engages in the construction and property development businesses in Malaysia and other Asian countries.

Moderate with questionable track record.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|24.5% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|45.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|33.9% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|56.1% undervalued

AX

Community Contributor