Advertisement

- Malaysia

- /

- Auto Components

- /

- KLSE:MCEHLDG

Only Four Days Left To Cash In On MCE Holdings Berhad's (KLSE:MCEHLDG) Dividend

Readers hoping to buy MCE Holdings Berhad (KLSE:MCEHLDG) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. The ex-dividend date is usually set to be two business days before the record date, which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is an important date to be aware of as any purchase of the stock made on or after this date might mean a late settlement that doesn't show on the record date. Accordingly, MCE Holdings Berhad investors that purchase the stock on or after the 29th of April will not receive the dividend, which will be paid on the 15th of May.

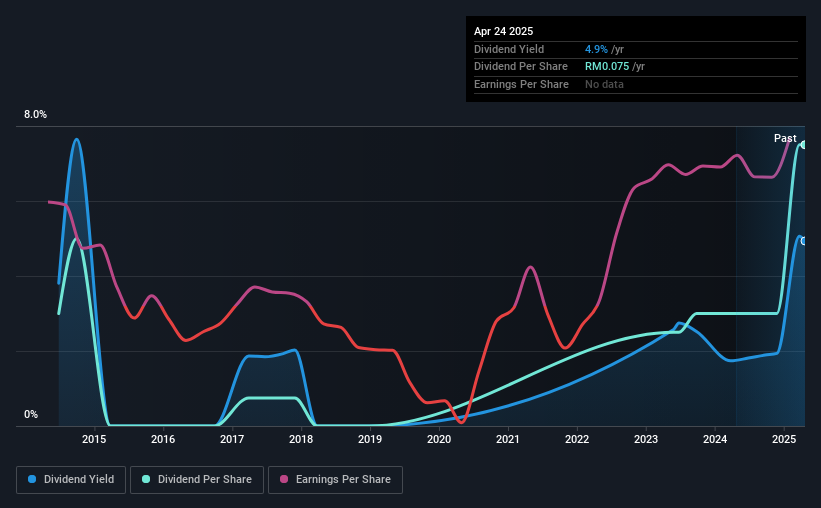

The company's next dividend payment will be RM00.06 per share, and in the last 12 months, the company paid a total of RM0.075 per share. Last year's total dividend payments show that MCE Holdings Berhad has a trailing yield of 4.9% on the current share price of RM01.52. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. So we need to investigate whether MCE Holdings Berhad can afford its dividend, and if the dividend could grow.

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. MCE Holdings Berhad paid out a comfortable 45% of its profit last year. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Over the past year it paid out 131% of its free cash flow as dividends, which is uncomfortably high. We're curious about why the company paid out more cash than it generated last year, since this can be one of the early signs that a dividend may be unsustainable.

MCE Holdings Berhad does have a large net cash position on the balance sheet, which could fund large dividends for a time, if the company so chose. Still, smart investors know that it is better to assess dividends relative to the cash and profit generated by the business. Paying dividends out of cash on the balance sheet is not long-term sustainable.

MCE Holdings Berhad paid out less in dividends than it reported in profits, but unfortunately it didn't generate enough cash to cover the dividend. Were this to happen repeatedly, this would be a risk to MCE Holdings Berhad's ability to maintain its dividend.

View our latest analysis for MCE Holdings Berhad

Click here to see how much of its profit MCE Holdings Berhad paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. That's why it's comforting to see MCE Holdings Berhad's earnings have been skyrocketing, up 61% per annum for the past five years. Earnings have been growing quickly, but we're concerned dividend payments consumed most of the company's cash flow over the past year.

MCE Holdings Berhad also issued more than 5% of its market cap in new stock during the past year, which we feel is likely to hurt its dividend prospects in the long run. It's hard to grow dividends per share when a company keeps creating new shares.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. MCE Holdings Berhad has delivered an average of 9.6% per year annual increase in its dividend, based on the past 10 years of dividend payments. It's encouraging to see the company lifting dividends while earnings are growing, suggesting at least some corporate interest in rewarding shareholders.

The Bottom Line

Is MCE Holdings Berhad an attractive dividend stock, or better left on the shelf? We like that MCE Holdings Berhad has been successfully growing its earnings per share at a nice rate and reinvesting most of its profits in the business. However, we note the high cashflow payout ratio with some concern. To summarise, MCE Holdings Berhad looks okay on this analysis, although it doesn't appear a stand-out opportunity.

While it's tempting to invest in MCE Holdings Berhad for the dividends alone, you should always be mindful of the risks involved. To help with this, we've discovered 3 warning signs for MCE Holdings Berhad (1 makes us a bit uncomfortable!) that you ought to be aware of before buying the shares.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:MCEHLDG

MCE Holdings Berhad

An investment holding company, designs, manufactures, and sells automotive electronics and mechatronics parts in Malaysia.

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.0% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.8% undervalued

RO

Community Contributor