- Mexico

- /

- Infrastructure

- /

- BMV:PINFRA *

Promotora y Operadora de Infraestructura, S. A. B. de C. V.'s (BMV:PINFRA) Popularity With Investors Is Clear

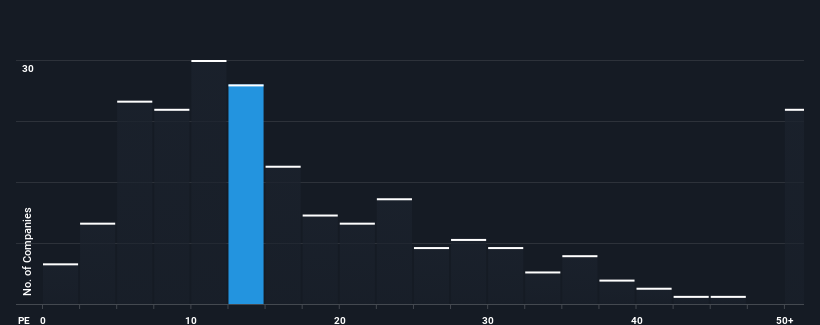

With a median price-to-earnings (or "P/E") ratio of close to 13x in Mexico, you could be forgiven for feeling indifferent about Promotora y Operadora de Infraestructura, S. A. B. de C. V.'s (BMV:PINFRA) P/E ratio of 14.6x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

While the market has experienced earnings growth lately, Promotora y Operadora de Infraestructura S. A. B. de C. V's earnings have gone into reverse gear, which is not great. It might be that many expect the dour earnings performance to strengthen positively, which has kept the P/E from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

Check out our latest analysis for Promotora y Operadora de Infraestructura S. A. B. de C. V

Is There Some Growth For Promotora y Operadora de Infraestructura S. A. B. de C. V?

In order to justify its P/E ratio, Promotora y Operadora de Infraestructura S. A. B. de C. V would need to produce growth that's similar to the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 13%. Still, the latest three year period has seen an excellent 47% overall rise in EPS, in spite of its unsatisfying short-term performance. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 8.3% per annum during the coming three years according to the eight analysts following the company. That's shaping up to be similar to the 9.2% per annum growth forecast for the broader market.

With this information, we can see why Promotora y Operadora de Infraestructura S. A. B. de C. V is trading at a fairly similar P/E to the market. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

The Bottom Line On Promotora y Operadora de Infraestructura S. A. B. de C. V's P/E

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Promotora y Operadora de Infraestructura S. A. B. de C. V's analyst forecasts revealed that its market-matching earnings outlook is contributing to its current P/E. At this stage investors feel the potential for an improvement or deterioration in earnings isn't great enough to justify a high or low P/E ratio. Unless these conditions change, they will continue to support the share price at these levels.

Don't forget that there may be other risks. For instance, we've identified 4 warning signs for Promotora y Operadora de Infraestructura S. A. B. de C. V that you should be aware of.

If you're unsure about the strength of Promotora y Operadora de Infraestructura S. A. B. de C. V's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BMV:PINFRA *

Promotora y Operadora de Infraestructura S. A. B. de C. V

Promotora y Operadora de Infraestructura, S.

Flawless balance sheet and undervalued.

Market Insights

Community Narratives