Advertisement

- Mexico

- /

- Basic Materials

- /

- BMV:CEMEX CPO

Results: CEMEX, S.A.B. de C.V. Beat Earnings Expectations And Analysts Now Have New Forecasts

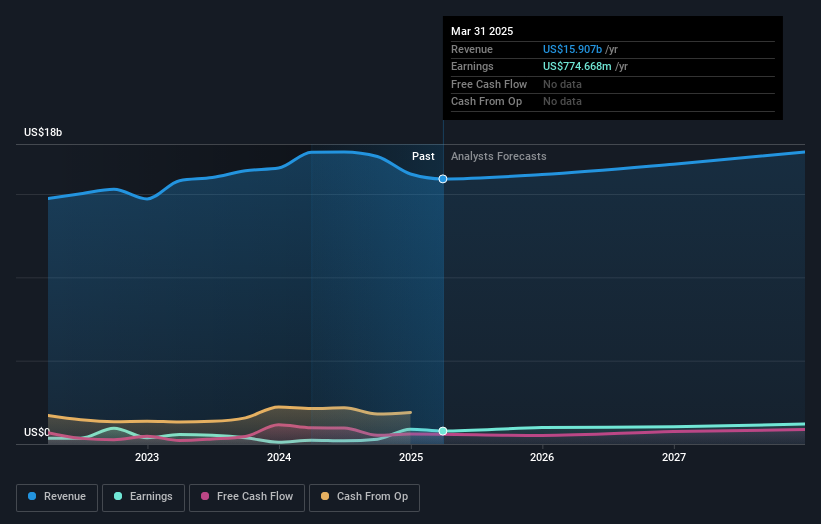

Investors in CEMEX, S.A.B. de C.V. (BMV:CEMEXCPO) had a good week, as its shares rose 8.0% to close at Mex$12.10 following the release of its quarterly results. It looks like a credible result overall - although revenues of US$3.6b were what the analysts expected, CEMEX. de surprised by delivering a (statutory) profit of US$0.05 per share, an impressive 400% above what was forecast. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

Taking into account the latest results, CEMEX. de's 14 analysts currently expect revenues in 2025 to be US$16.2b, approximately in line with the last 12 months. Statutory earnings per share are predicted to shoot up 50% to US$0.08. In the lead-up to this report, the analysts had been modelling revenues of US$16.2b and earnings per share (EPS) of US$0.067 in 2025. There was no real change to the revenue estimates, but the analysts do seem more bullish on earnings, given the nice gain to earnings per share expectations following these results.

View our latest analysis for CEMEX. de

The consensus price target was unchanged at Mex$17.49, implying that the improved earnings outlook is not expected to have a long term impact on value creation for shareholders. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic CEMEX. de analyst has a price target of Mex$23.06 per share, while the most pessimistic values it at Mex$14.73. As you can see the range of estimates is wide, with the lowest valuation coming in at less than half the most bullish estimate, suggesting there are some strongly diverging views on how analysts think this business will perform. As a result it might not be a great idea to make decisions based on the consensus price target, which is after all just an average of this wide range of estimates.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. We would highlight that CEMEX. de's revenue growth is expected to slow, with the forecast 2.2% annualised growth rate until the end of 2025 being well below the historical 6.4% p.a. growth over the last five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 9.1% annually. Factoring in the forecast slowdown in growth, it seems obvious that CEMEX. de is also expected to grow slower than other industry participants.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around CEMEX. de's earnings potential next year. Fortunately, the analysts also reconfirmed their revenue estimates, suggesting that it's tracking in line with expectations. Although our data does suggest that CEMEX. de's revenue is expected to perform worse than the wider industry. The consensus price target held steady at Mex$17.49, with the latest estimates not enough to have an impact on their price targets.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for CEMEX. de going out to 2027, and you can see them free on our platform here..

That said, it's still necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with CEMEX. de , and understanding these should be part of your investment process.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BMV:CEMEX CPO

CEMEX. de

Engages in the production, marketing, distribution, and sale of cement, ready-mix concrete, aggregates, urbanization solutions, and other construction materials and services worldwide.

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor