Advertisement

- South Korea

- /

- Electronic Equipment and Components

- /

- KOSDAQ:A321370

Does Sensorview (KOSDAQ:321370) Have A Healthy Balance Sheet?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Sensorview Co., LTD (KOSDAQ:321370) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Sensorview

How Much Debt Does Sensorview Carry?

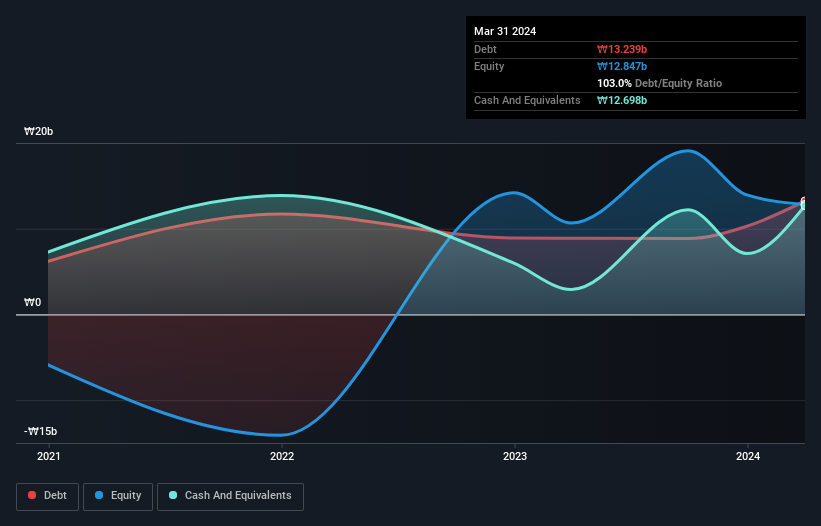

As you can see below, at the end of March 2024, Sensorview had ₩13.2b of debt, up from ₩8.89b a year ago. Click the image for more detail. However, it does have ₩12.7b in cash offsetting this, leading to net debt of about ₩540.8m.

How Healthy Is Sensorview's Balance Sheet?

The latest balance sheet data shows that Sensorview had liabilities of ₩9.05b due within a year, and liabilities of ₩13.9b falling due after that. Offsetting this, it had ₩12.7b in cash and ₩4.04b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₩6.17b.

Of course, Sensorview has a market capitalization of ₩85.1b, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. But either way, Sensorview has virtually no net debt, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Sensorview will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Sensorview wasn't profitable at an EBIT level, but managed to grow its revenue by 36%, to ₩10.0b. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

While we can certainly appreciate Sensorview's revenue growth, its earnings before interest and tax (EBIT) loss is not ideal. Its EBIT loss was a whopping ₩19b. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. However, it doesn't help that it burned through ₩18b of cash over the last year. So suffice it to say we consider the stock very risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for Sensorview (2 are potentially serious!) that you should be aware of before investing here.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A321370

Sensorview

Develops, manufactures, and sells antennas and cables for mmWave and 5G technologies in South Korea and internationally.

Adequate balance sheet with slight risk.

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Optimi Health ·

OPTH: A licensed manufacturer already selling MDMA while peers still wait on trials

Fair Value:US$1259.6% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

FU

FundamentalFlow on Vertiv Holdings Co ·

The Short and Long Term Compounder of Liquid Cooling industry.

Fair Value:US$45040.0% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

JO

John_Eric on SPX Technologies ·

I Fell in Love With a Data-Center Cooling Stock. Then I Opened the Filings.

Fair Value:US$2034.6% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

TR

tripledub on GQG Partners ·

The Cheap Genius Problem

Fair Value:AU$2.4541.2% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

Recently Updated Narratives

RC

rcb9 on Palantir Technologies ·

The Fifty-Five Percent Margin Is A Tax Holiday, Not The Business

Fair Value:US$91.8590.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KL

Klim on PetroTal ·

PetroTal: Betting On a Production Recovery

Fair Value:CA$0.8542.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

david_1211213 on Robo.ai ·

Robo.ai (AIIO): A Long-Term Bullish Technical Setup

Fair Value:US$5.6443.6% undervalued

1 followerusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28022.3% undervalued

294 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9120.5% overvalued

156 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0941.5% undervalued

177 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

IA

ian_oii7z on Woodside Energy Group ·

Hey James! Thank you but I am not sure if I am reading this correctly as your analysis opens with "At A$36.602 per share, Woodside Energy Group (ASX: WDS) appears reasonably valued based on its existing operations and near-term production growth." I would like to say that the last time that WDS was above $36.00 per share was in October 2023, so I am a little confused by your statement w.r.t. current prices etc . Can you please explain?

1

|0

GE

george_b177x on Bloom Energy ·

Brilliant analysis. Great company with proven product and service!

0

|0