Advertisement

- South Korea

- /

- Electronic Equipment and Components

- /

- KOSDAQ:A131400

There's Reason For Concern Over EV Advanced Material Co.,Ltd's (KOSDAQ:131400) Massive 39% Price Jump

Those holding EV Advanced Material Co.,Ltd (KOSDAQ:131400) shares would be relieved that the share price has rebounded 39% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 39% in the last twelve months.

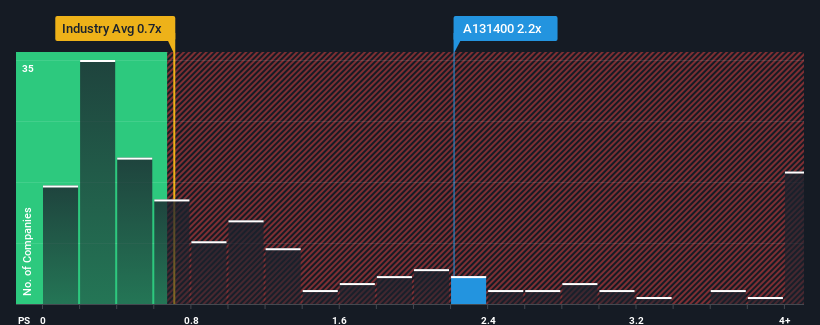

Following the firm bounce in price, you could be forgiven for thinking EV Advanced MaterialLtd is a stock not worth researching with a price-to-sales ratios (or "P/S") of 2.2x, considering almost half the companies in Korea's Electronic industry have P/S ratios below 0.7x. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for EV Advanced MaterialLtd

How EV Advanced MaterialLtd Has Been Performing

Revenue has risen firmly for EV Advanced MaterialLtd recently, which is pleasing to see. Perhaps the market is expecting this decent revenue performance to beat out the industry over the near term, which has kept the P/S propped up. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on EV Advanced MaterialLtd's earnings, revenue and cash flow.What Are Revenue Growth Metrics Telling Us About The High P/S?

EV Advanced MaterialLtd's P/S ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 8.6% last year. The latest three year period has also seen a 11% overall rise in revenue, aided somewhat by its short-term performance. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Comparing the recent medium-term revenue trends against the industry's one-year growth forecast of 12% shows it's noticeably less attractive.

With this in mind, we find it worrying that EV Advanced MaterialLtd's P/S exceeds that of its industry peers. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

The Bottom Line On EV Advanced MaterialLtd's P/S

EV Advanced MaterialLtd shares have taken a big step in a northerly direction, but its P/S is elevated as a result. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of EV Advanced MaterialLtd revealed its poor three-year revenue trends aren't detracting from the P/S as much as we though, given they look worse than current industry expectations. When we see slower than industry revenue growth but an elevated P/S, there's considerable risk of the share price declining, sending the P/S lower. Unless there is a significant improvement in the company's medium-term performance, it will be difficult to prevent the P/S ratio from declining to a more reasonable level.

You need to take note of risks, for example - EV Advanced MaterialLtd has 2 warning signs (and 1 which can't be ignored) we think you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if EV Advanced MaterialLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A131400

EV Advanced MaterialLtd

Engages in the manufacture and sale of flexible printed circuit boards (FPCBs) in South Korea.

Flawless balance sheet with low risk.

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4034.1% undervalued

20 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6089.9% undervalued

22 followersusers have followed this narrative

2 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.0% undervalued

43 followersusers have followed this narrative

3 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

KI

KiwiInvest on Rocket Lab ·

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value:US$97.8335.1% undervalued

136 followersusers have followed this narrative

8 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BA

Bauyrzhan on Dollar General ·

Dollar general to grow

Fair Value:US$158.916.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MH

mhbb on Mastersystem Infotama ·

Mastersystem Infotama will achieve 18.9% revenue growth as fair value hits IDR1,650

Fair Value:Rp1.63k13.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

119 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.7% undervalued

963 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8683.3% undervalued

77 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative