Advertisement

- South Korea

- /

- Electronic Equipment and Components

- /

- KOSDAQ:A037030

Is Powernet Technologies (KOSDAQ:037030) Using Too Much Debt?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Powernet Technologies Corporation (KOSDAQ:037030) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Powernet Technologies

What Is Powernet Technologies's Debt?

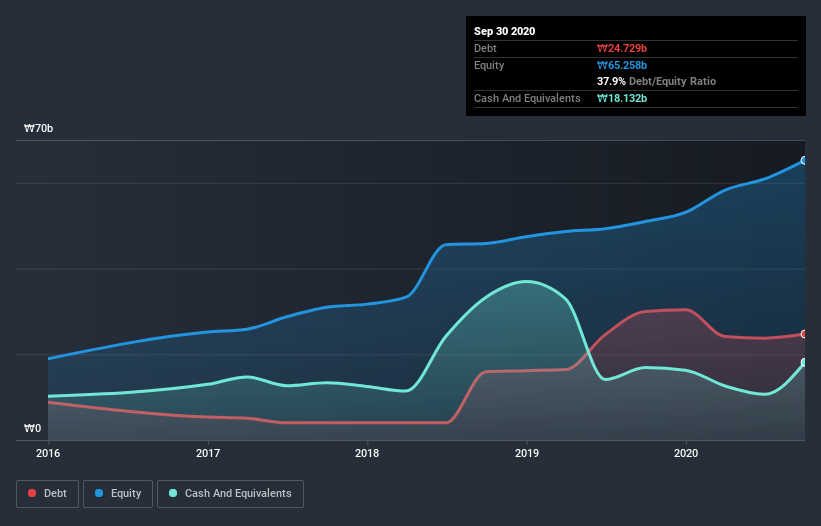

As you can see below, Powernet Technologies had ₩23.3b of debt at September 2020, down from ₩30.0b a year prior. However, it does have ₩18.1b in cash offsetting this, leading to net debt of about ₩5.17b.

A Look At Powernet Technologies's Liabilities

Zooming in on the latest balance sheet data, we can see that Powernet Technologies had liabilities of ₩48.3b due within 12 months and liabilities of ₩13.8b due beyond that. Offsetting these obligations, it had cash of ₩18.1b as well as receivables valued at ₩27.4b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₩16.7b.

Since publicly traded Powernet Technologies shares are worth a total of ₩90.5b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Looking at its net debt to EBITDA of 0.65 and interest cover of 3.3 times, it seems to us that Powernet Technologies is probably using debt in a pretty reasonable way. But the interest payments are certainly sufficient to have us thinking about how affordable its debt is. Sadly, Powernet Technologies's EBIT actually dropped 6.6% in the last year. If earnings continue on that decline then managing that debt will be difficult like delivering hot soup on a unicycle. When analysing debt levels, the balance sheet is the obvious place to start. But it is Powernet Technologies's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Powernet Technologies reported free cash flow worth 7.5% of its EBIT, which is really quite low. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

Powernet Technologies's conversion of EBIT to free cash flow and interest cover definitely weigh on it, in our esteem. But the good news is it seems to be able handle its debt, based on its EBITDA, with ease. When we consider all the factors discussed, it seems to us that Powernet Technologies is taking some risks with its use of debt. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Like risks, for instance. Every company has them, and we've spotted 5 warning signs for Powernet Technologies (of which 1 shouldn't be ignored!) you should know about.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you’re looking to trade Powernet Technologies, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A037030

Powernet Technologies

Manufactures and sells SMPS products.

Moderate risk with mediocre balance sheet.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7065.0% undervalued

41 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.2% undervalued

45 followersusers have followed this narrative

8 commentsusers have commented on this narrative

15 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0541.3% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15123.0% undervalued

91 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

HU

Hunter_Z on Pentech Holdings Berhad ·

Pentech Rides Malaysia’s Growing Demand for Digital Infrastructure

Fair Value:RM 0.450.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on IMPACT Silver ·

Impact Silver, Record 2025 Revenue + High-Grade Kena Vein = Massive Silver Leverage Play

Fair Value:CA$896.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$25.4648.3% undervalued

55 followersusers have followed this narrative

4 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7446.4% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.5% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1931.2% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative