Advertisement

- South Korea

- /

- IT

- /

- KOSDAQ:A042000

Risks Still Elevated At These Prices As Cafe24 Corp. (KOSDAQ:042000) Shares Dive 26%

Unfortunately for some shareholders, the Cafe24 Corp. (KOSDAQ:042000) share price has dived 26% in the last thirty days, prolonging recent pain. Looking at the bigger picture, even after this poor month the stock is up 87% in the last year.

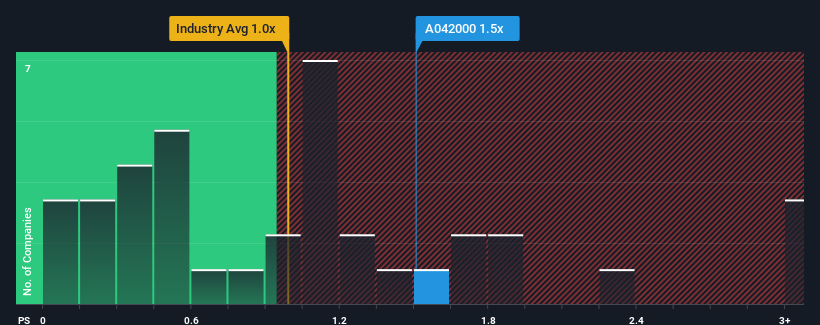

Although its price has dipped substantially, when almost half of the companies in Korea's IT industry have price-to-sales ratios (or "P/S") below 1x, you may still consider Cafe24 as a stock probably not worth researching with its 1.5x P/S ratio. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Cafe24

What Does Cafe24's P/S Mean For Shareholders?

With revenue growth that's superior to most other companies of late, Cafe24 has been doing relatively well. The P/S is probably high because investors think this strong revenue performance will continue. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think Cafe24's future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The High P/S Ratio?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Cafe24's to be considered reasonable.

Retrospectively, the last year delivered a decent 7.2% gain to the company's revenues. The solid recent performance means it was also able to grow revenue by 22% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Turning to the outlook, the next year should bring diminished returns, with revenue decreasing 0.8% as estimated by the only analyst watching the company. Meanwhile, the broader industry is forecast to expand by 9.9%, which paints a poor picture.

With this in mind, we find it intriguing that Cafe24's P/S is closely matching its industry peers. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as these declining revenues are likely to weigh heavily on the share price eventually.

The Key Takeaway

There's still some elevation in Cafe24's P/S, even if the same can't be said for its share price recently. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Cafe24 currently trades on a much higher than expected P/S for a company whose revenues are forecast to decline. In cases like this where we see revenue decline on the horizon, we suspect the share price is at risk of following suit, bringing back the high P/S into the realms of suitability. At these price levels, investors should remain cautious, particularly if things don't improve.

There are also other vital risk factors to consider and we've discovered 3 warning signs for Cafe24 (1 can't be ignored!) that you should be aware of before investing here.

If you're unsure about the strength of Cafe24's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A042000

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4035.0% undervalued

28 followersusers have followed this narrative

5 commentsusers have commented on this narrative

9 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6090.4% undervalued

26 followersusers have followed this narrative

3 commentsusers have commented on this narrative

19 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8151.3% undervalued

49 followersusers have followed this narrative

4 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.225.4% undervalued

49 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on Fiverr International ·

Fiverr International will transform the freelance industry with AI-powered growth

Fair Value:US$43.3352.3% undervalued

82 followersusers have followed this narrative

8 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YI

yiannisz on Janus Henderson Group ·

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Fair Value:US$41.459.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

120 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8683.7% undervalued

78 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3930.1% undervalued

968 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative