Advertisement

- South Korea

- /

- Specialty Stores

- /

- KOSE:A128820

Daesung Industrial (KRX:128820) Is Posting Promising Earnings But The Good News Doesn’t Stop There

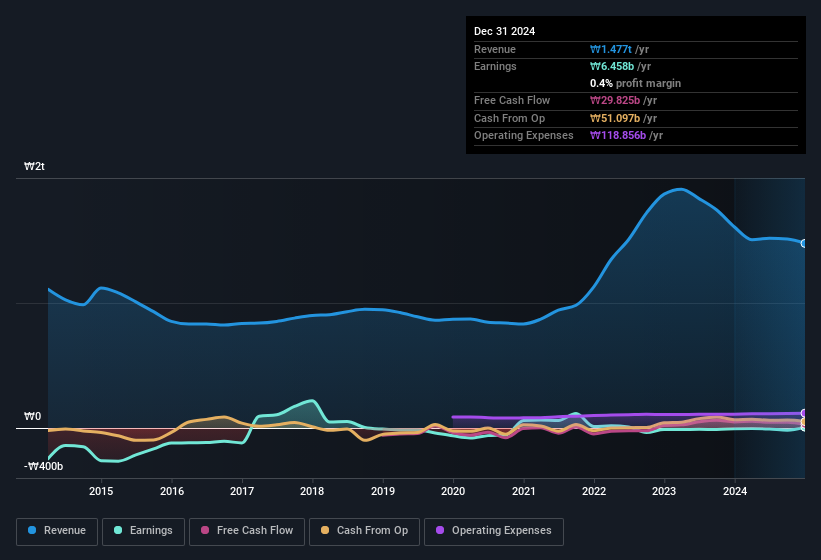

Shareholders appeared to be happy with Daesung Industrial Co., Ltd.'s (KRX:128820) solid earnings report last week. According to our analysis of the report, the strong headline profit numbers are supported by strong earnings fundamentals.

How Do Unusual Items Influence Profit?

For anyone who wants to understand Daesung Industrial's profit beyond the statutory numbers, it's important to note that during the last twelve months statutory profit was reduced by ₩13b due to unusual items. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And, after all, that's exactly what the accounting terminology implies. Daesung Industrial took a rather significant hit from unusual items in the year to December 2024. All else being equal, this would likely have the effect of making the statutory profit look worse than its underlying earnings power.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Daesung Industrial.

An Unusual Tax Situation

Having already discussed the impact of the unusual items, we should also note that Daesung Industrial received a tax benefit of ₩3.7b. This is of course a bit out of the ordinary, given it is more common for companies to be paying tax than receiving tax benefits! The receipt of a tax benefit is obviously a good thing, on its own. And given that it lost money last year, it seems possible that the benefit is evidence that it now expects to find value in its past tax losses. However, the devil in the detail is that these kind of benefits only impact in the year they are booked, and are often one-off in nature. Assuming the tax benefit is not repeated every year, we could see its profitability drop noticeably, all else being equal. While we think it's good that the company has booked a tax benefit, it does mean that there's every chance the statutory profit will come in a lot higher than it would be if the income was adjusted for one-off factors.

Our Take On Daesung Industrial's Profit Performance

In its last report Daesung Industrial received a tax benefit which might make its profit look better than it really is on a underlying level. Having said that, it also had a unusual item reducing its profit. Based on these factors, we think that Daesung Industrial's profits are a reasonably conservative guide to its underlying profitability. So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. Be aware that Daesung Industrial is showing 3 warning signs in our investment analysis and 1 of those is a bit concerning...

In this article we've looked at a number of factors that can impair the utility of profit numbers, as a guide to a business. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A128820

Daesung Industrial

Engages in distribution of energy and other businesses worldwide.

Fair value low.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.0% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.7% undervalued

RO

Community Contributor