Advertisement

- South Korea

- /

- Retail Distributors

- /

- KOSDAQ:A036620

Is Virtualtek (KOSDAQ:036620) Using Debt Sensibly?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Virtualtek Corp (KOSDAQ:036620) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Virtualtek

What Is Virtualtek's Debt?

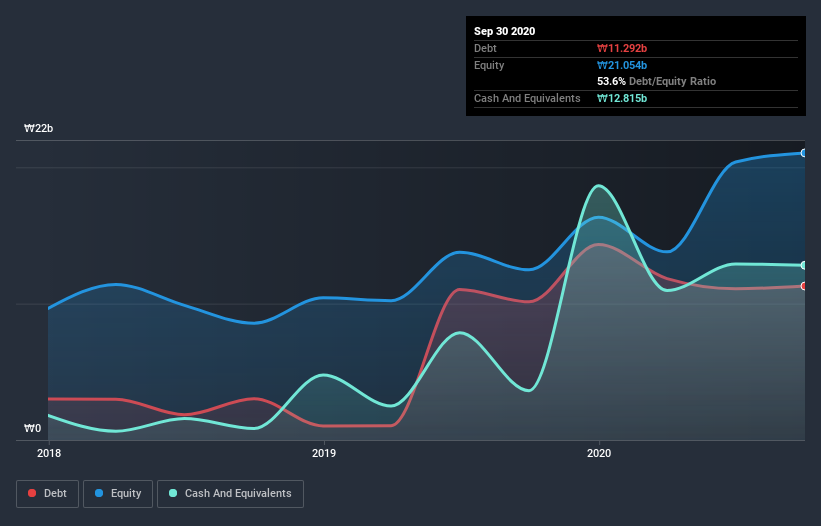

As you can see below, at the end of September 2020, Virtualtek had ₩11.3b of debt, up from ₩10.1b a year ago. Click the image for more detail. But it also has ₩12.8b in cash to offset that, meaning it has ₩1.52b net cash.

How Healthy Is Virtualtek's Balance Sheet?

The latest balance sheet data shows that Virtualtek had liabilities of ₩15.6b due within a year, and liabilities of ₩2.02b falling due after that. On the other hand, it had cash of ₩12.8b and ₩3.95b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₩855.9m.

This state of affairs indicates that Virtualtek's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the ₩56.0b company is short on cash, but still worth keeping an eye on the balance sheet. While it does have liabilities worth noting, Virtualtek also has more cash than debt, so we're pretty confident it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But it is Virtualtek's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Virtualtek wasn't profitable at an EBIT level, but managed to grow its revenue by 193%, to ₩14b. So its pretty obvious shareholders are hoping for more growth!

So How Risky Is Virtualtek?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that Virtualtek had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through ₩8.3b of cash and made a loss of ₩6.5b. But at least it has ₩1.52b on the balance sheet to spend on growth, near-term. The good news for shareholders is that Virtualtek has dazzling revenue growth, so there's a very good chance it can boost its free cash flow in the years to come. While unprofitable companies can be risky, they can also grow hard and fast in those pre-profit years. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 2 warning signs with Virtualtek , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

When trading Virtualtek or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A036620

GAMSUNG Corporation

Engages in the apparel and mobile peripheral business.

Reasonable growth potential and slightly overvalued.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7063.1% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.5% undervalued

51 followersusers have followed this narrative

8 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0539.5% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15121.8% undervalued

92 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Investigator Silver ·

Investigator Silver, Leverage Exposed: $1/oz Move = $42M Cash for This ASX Developer

Fair Value:AU$2.3997.7% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

TA

Talos on Voyager Technologies ·

The "Landlord of Orbit" – A Deep Value Play Ahead of the Starlab Era

Fair Value:US$385.289.5% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Advanced Micro Devices ·

The "David vs. Goliath" AI Trade – Why Second Place is Worth Billions

Fair Value:US$907.3239.7% undervalued

38 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.3% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1929.0% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9721.9% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative