- South Korea

- /

- Biotech

- /

- KOSDAQ:A214450

3 Growth Stocks With High Insider Ownership And 24% Revenue Growth

Reviewed by Simply Wall St

In a week marked by mixed performances across global markets, major U.S. indices like the S&P 500 and Nasdaq Composite reached new record highs, driven largely by a rally in growth stocks. As investors navigate these fluctuating conditions, focusing on growth companies with high insider ownership can be an effective strategy, as it often indicates strong confidence from those closest to the business and aligns management's interests with shareholders'.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| People & Technology (KOSDAQ:A137400) | 16.4% | 37.3% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 26.3% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 41.3% |

| Laopu Gold (SEHK:6181) | 36.4% | 34.2% |

| Medley (TSE:4480) | 34% | 31.7% |

| Plenti Group (ASX:PLT) | 12.8% | 120.1% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 131.1% |

| Fulin Precision (SZSE:300432) | 13.6% | 66.7% |

| HANA Micron (KOSDAQ:A067310) | 18.4% | 110.9% |

| Findi (ASX:FND) | 34.8% | 112.9% |

We're going to check out a few of the best picks from our screener tool.

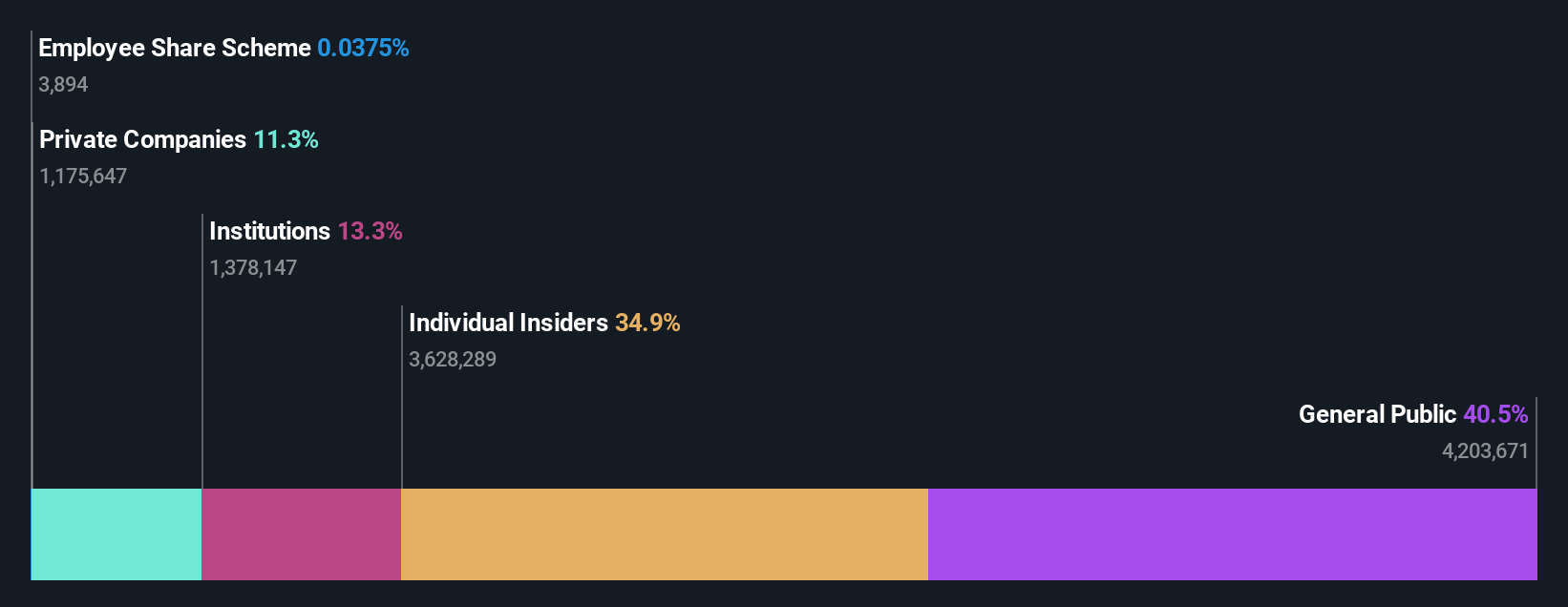

PharmaResearch (KOSDAQ:A214450)

Simply Wall St Growth Rating: ★★★★★☆

Overview: PharmaResearch Co., Ltd., along with its subsidiaries, is a biopharmaceutical company operating mainly in South Korea with a market cap of ₩2.41 trillion.

Operations: The company generates revenue of ₩316.99 billion from its pharmaceuticals segment.

Insider Ownership: 38.6%

Revenue Growth Forecast: 24.2% p.a.

PharmaResearch is poised for significant growth, with revenue forecasted to increase by 24.2% annually, outpacing the KR market's 9%. Despite trading at 44.9% below fair value estimates, analysts predict a stock price rise of 21.9%. Earnings are expected to grow significantly at 28% annually over the next three years, although slightly below the market average. The company recently completed a private placement on October 8, enhancing its financial flexibility for future expansion.

- Delve into the full analysis future growth report here for a deeper understanding of PharmaResearch.

- Upon reviewing our latest valuation report, PharmaResearch's share price might be too pessimistic.

Nanjing Develop Advanced Manufacturing (SHSE:688377)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Nanjing Develop Advanced Manufacturing Co., Ltd. operates in the advanced manufacturing sector and has a market cap of CN¥3.79 billion.

Operations: Unfortunately, the provided text does not include specific revenue segment information for Nanjing Develop Advanced Manufacturing Co., Ltd., so I am unable to summarize it into a sentence.

Insider Ownership: 16.8%

Revenue Growth Forecast: 23.9% p.a.

Nanjing Develop Advanced Manufacturing is positioned for robust growth, with earnings expected to increase significantly at 48.2% annually, surpassing the CN market's average of 25.9%. Despite a decrease in net income to CNY 63.81 million from CNY 124.18 million last year, revenue growth is forecasted at 23.9% per year, exceeding the market rate of 13.7%. However, profit margins have declined and the dividend yield of 1.17% lacks coverage by free cash flows.

- Click here to discover the nuances of Nanjing Develop Advanced Manufacturing with our detailed analytical future growth report.

- Insights from our recent valuation report point to the potential overvaluation of Nanjing Develop Advanced Manufacturing shares in the market.

Bichamp Cutting Technology (Hunan) (SZSE:002843)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Bichamp Cutting Technology (Hunan) Co., Ltd. (SZSE:002843) operates in the cutting tools industry and has a market cap of CN¥5.25 billion.

Operations: Bichamp Cutting Technology generates its revenue primarily from the cutting tools industry.

Insider Ownership: 31.8%

Revenue Growth Forecast: 24.1% p.a.

Bichamp Cutting Technology (Hunan) anticipates robust growth, with earnings projected to grow at 28.7% annually, outpacing the CN market's 25.9%. Revenue is expected to rise by 24.1% per year, exceeding the market average of 13.7%. However, recent financials show a decline in net income to CNY 66.02 million from CNY 102.63 million last year and a dividend yield of 0.92% that isn't supported by free cash flows.

- Get an in-depth perspective on Bichamp Cutting Technology (Hunan)'s performance by reading our analyst estimates report here.

- Our comprehensive valuation report raises the possibility that Bichamp Cutting Technology (Hunan) is priced higher than what may be justified by its financials.

Summing It All Up

- Gain an insight into the universe of 1510 Fast Growing Companies With High Insider Ownership by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A214450

PharmaResearch

Operates as a biopharmaceutical company primarily in South Korea.

Flawless balance sheet with high growth potential.

Market Insights

Community Narratives