- South Korea

- /

- Chemicals

- /

- KOSE:A002380

The recent 5.5% gain must have brightened CEO Mong-Jin Chung's week, KCC Corporation's (KRX:002380) most bullish insider

Key Insights

- Insiders appear to have a vested interest in KCC's growth, as seen by their sizeable ownership

- A total of 4 investors have a majority stake in the company with 52% ownership

- Institutions own 27% of KCC

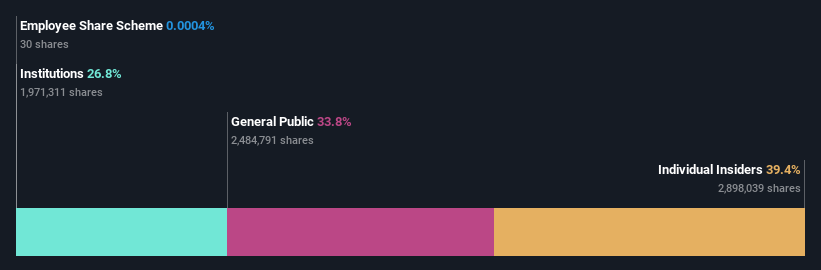

If you want to know who really controls KCC Corporation (KRX:002380), then you'll have to look at the makeup of its share registry. And the group that holds the biggest piece of the pie are individual insiders with 39% ownership. In other words, the group stands to gain the most (or lose the most) from their investment into the company.

As a result, insiders scored the highest last week as the company hit ₩1.9t market cap following a 5.5% gain in the stock.

Let's delve deeper into each type of owner of KCC, beginning with the chart below.

Check out our latest analysis for KCC

What Does The Institutional Ownership Tell Us About KCC?

Institutional investors commonly compare their own returns to the returns of a commonly followed index. So they generally do consider buying larger companies that are included in the relevant benchmark index.

As you can see, institutional investors have a fair amount of stake in KCC. This can indicate that the company has a certain degree of credibility in the investment community. However, it is best to be wary of relying on the supposed validation that comes with institutional investors. They too, get it wrong sometimes. It is not uncommon to see a big share price drop if two large institutional investors try to sell out of a stock at the same time. So it is worth checking the past earnings trajectory of KCC, (below). Of course, keep in mind that there are other factors to consider, too.

KCC is not owned by hedge funds. The company's CEO Mong-Jin Chung is the largest shareholder with 27% of shares outstanding. In comparison, the second and third largest shareholders hold about 12% and 7.6% of the stock.

On looking further, we found that 52% of the shares are owned by the top 4 shareholders. In other words, these shareholders have a meaningful say in the decisions of the company.

While it makes sense to study institutional ownership data for a company, it also makes sense to study analyst sentiments to know which way the wind is blowing. While there is some analyst coverage, the company is probably not widely covered. So it could gain more attention, down the track.

Insider Ownership Of KCC

While the precise definition of an insider can be subjective, almost everyone considers board members to be insiders. Management ultimately answers to the board. However, it is not uncommon for managers to be executive board members, especially if they are a founder or the CEO.

Insider ownership is positive when it signals leadership are thinking like the true owners of the company. However, high insider ownership can also give immense power to a small group within the company. This can be negative in some circumstances.

It seems insiders own a significant proportion of KCC Corporation. It is very interesting to see that insiders have a meaningful ₩749b stake in this ₩1.9t business. It is good to see this level of investment. You can check here to see if those insiders have been buying recently.

General Public Ownership

The general public-- including retail investors -- own 34% stake in the company, and hence can't easily be ignored. While this size of ownership may not be enough to sway a policy decision in their favour, they can still make a collective impact on company policies.

Next Steps:

I find it very interesting to look at who exactly owns a company. But to truly gain insight, we need to consider other information, too. Take risks for example - KCC has 3 warning signs (and 2 which are significant) we think you should know about.

If you are like me, you may want to think about whether this company will grow or shrink. Luckily, you can check this free report showing analyst forecasts for its future.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

If you're looking to trade KCC, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if KCC might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A002380

Undervalued with proven track record and pays a dividend.

Market Insights

Community Narratives