Advertisement

- South Korea

- /

- Aerospace & Defense

- /

- KOSE:A272210

Subdued Growth No Barrier To Hanwha Systems Co., Ltd. (KRX:272210) With Shares Advancing 26%

Hanwha Systems Co., Ltd. (KRX:272210) shares have continued their recent momentum with a 26% gain in the last month alone. The annual gain comes to 101% following the latest surge, making investors sit up and take notice.

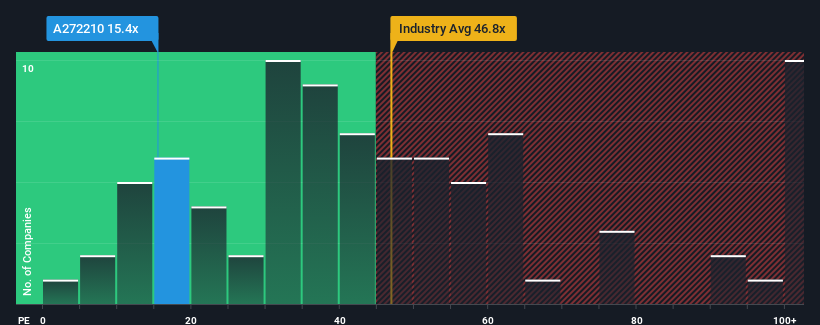

After such a large jump in price, given around half the companies in Korea have price-to-earnings ratios (or "P/E's") below 11x, you may consider Hanwha Systems as a stock to potentially avoid with its 15.4x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

We've discovered 3 warning signs about Hanwha Systems. View them for free.Hanwha Systems certainly has been doing a good job lately as it's been growing earnings more than most other companies. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. If not, then existing shareholders might be a little nervous about the viability of the share price.

View our latest analysis for Hanwha Systems

How Is Hanwha Systems' Growth Trending?

There's an inherent assumption that a company should outperform the market for P/E ratios like Hanwha Systems' to be considered reasonable.

Retrospectively, the last year delivered an exceptional 24% gain to the company's bottom line. Pleasingly, EPS has also lifted 303% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Turning to the outlook, the next three years should bring diminished returns, with earnings decreasing 9.6% per year as estimated by the analysts watching the company. With the market predicted to deliver 18% growth per annum, that's a disappointing outcome.

With this information, we find it concerning that Hanwha Systems is trading at a P/E higher than the market. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as these declining earnings are likely to weigh heavily on the share price eventually.

What We Can Learn From Hanwha Systems' P/E?

Hanwha Systems shares have received a push in the right direction, but its P/E is elevated too. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Hanwha Systems' analyst forecasts revealed that its outlook for shrinking earnings isn't impacting its high P/E anywhere near as much as we would have predicted. When we see a poor outlook with earnings heading backwards, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with Hanwha Systems, and understanding them should be part of your investment process.

You might be able to find a better investment than Hanwha Systems. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Hanwha Systems might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A272210

Hanwha Systems

Hanwha Systems Co., Ltd. manufacture and sell various military equipments in South Korea and internationally.

Excellent balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.8% undervalued

RO

Community Contributor