- South Korea

- /

- Machinery

- /

- KOSE:A267270

HD Hyundai Construction Equipment's (KRX:267270) earnings growth rate lags the 31% CAGR delivered to shareholders

HD Hyundai Construction Equipment Co., LTD. (KRX:267270) shareholders might be concerned after seeing the share price drop 22% in the last month. But that scarcely detracts from the really solid long term returns generated by the company over five years. It's fair to say most would be happy with 259% the gain in that time. To some, the recent pullback wouldn't be surprising after such a fast rise. Only time will tell if there is still too much optimism currently reflected in the share price.

Although HD Hyundai Construction Equipment has shed ₩108b from its market cap this week, let's take a look at its longer term fundamental trends and see if they've driven returns.

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

During five years of share price growth, HD Hyundai Construction Equipment achieved compound earnings per share (EPS) growth of 102% per year. The EPS growth is more impressive than the yearly share price gain of 29% over the same period. So it seems the market isn't so enthusiastic about the stock these days. This cautious sentiment is reflected in its (fairly low) P/E ratio of 10.78.

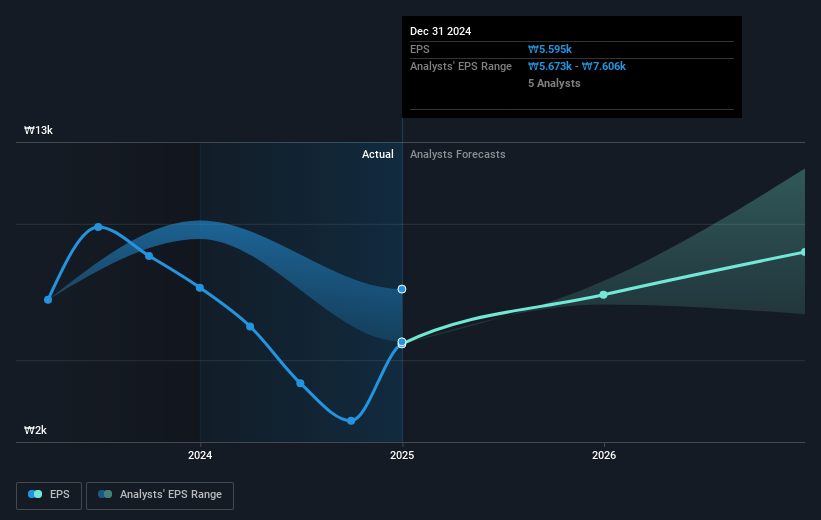

The graphic below depicts how EPS has changed over time (unveil the exact values by clicking on the image).

Dive deeper into HD Hyundai Construction Equipment's key metrics by checking this interactive graph of HD Hyundai Construction Equipment's earnings, revenue and cash flow .

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. As it happens, HD Hyundai Construction Equipment's TSR for the last 5 years was 288%, which exceeds the share price return mentioned earlier. This is largely a result of its dividend payments!

A Different Perspective

It's good to see that HD Hyundai Construction Equipment has rewarded shareholders with a total shareholder return of 10% in the last twelve months. And that does include the dividend. However, the TSR over five years, coming in at 31% per year, is even more impressive. The pessimistic view would be that be that the stock has its best days behind it, but on the other hand the price might simply be moderating while the business itself continues to execute. It's always interesting to track share price performance over the longer term. But to understand HD Hyundai Construction Equipment better, we need to consider many other factors. Consider risks, for instance. Every company has them, and we've spotted 1 warning sign for HD Hyundai Construction Equipment you should know about.

If you are like me, then you will not want to miss this free list of undervalued small caps that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on South Korean exchanges.

Valuation is complex, but we're here to simplify it.

Discover if HD Hyundai Construction Equipment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A267270

HD Hyundai Construction Equipment

HD Hyundai Construction Equipment Co.,Ltd.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Community Narratives