- South Korea

- /

- Machinery

- /

- KOSE:A042670

HD Hyundai Infracore Third Quarter 2024 Earnings: ₩132 loss per share (vs ₩246 profit in 3Q 2023)

HD Hyundai Infracore (KRX:042670) Third Quarter 2024 Results

Key Financial Results

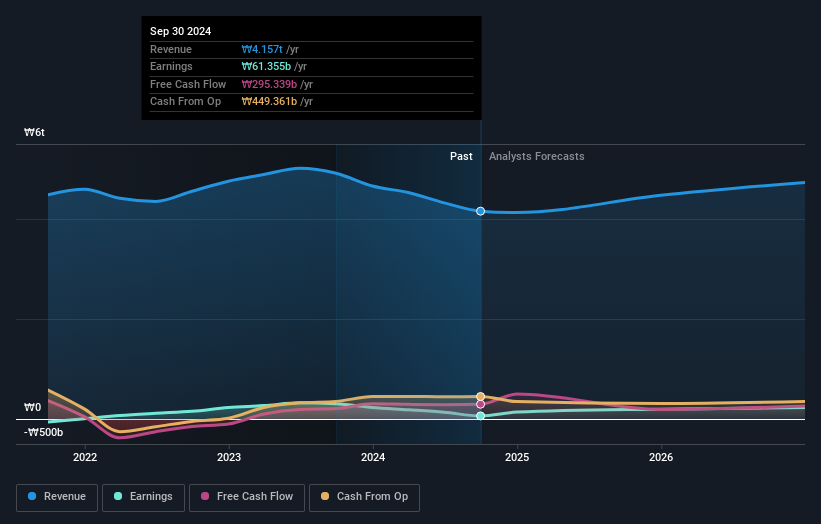

- Revenue: ₩909.8b (down 16% from 3Q 2023).

- Net loss: ₩25.5b (down by 152% from ₩49.1b profit in 3Q 2023).

- ₩132 loss per share (down from ₩246 profit in 3Q 2023).

All figures shown in the chart above are for the trailing 12 month (TTM) period

HD Hyundai Infracore Earnings Insights

Looking ahead, revenue is forecast to grow 6.2% p.a. on average during the next 3 years, compared to a 16% growth forecast for the Machinery industry in South Korea.

Performance of the South Korean Machinery industry.

The company's share price is broadly unchanged from a week ago.

Risk Analysis

You should learn about the 3 warning signs we've spotted with HD Hyundai Infracore.

Valuation is complex, but we're here to simplify it.

Discover if HD Hyundai Infracore might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A042670

HD Hyundai Infracore

Engages in the production and sale of construction equipment, engines, attachments, and utility equipment in South Korea and internationally.

Excellent balance sheet and fair value.