- South Korea

- /

- Electrical

- /

- KOSDAQ:A154040

Why Dasan SoluetaLtd's (KOSDAQ:154040) Healthy Earnings Aren’t As Good As They Seem

Shareholders didn't seem to be thrilled with Dasan Solueta Co.,Ltd.'s (KOSDAQ:154040) recent earnings report, despite healthy profit numbers. Our analysis has found some concerning factors which weaken the profit's foundation.

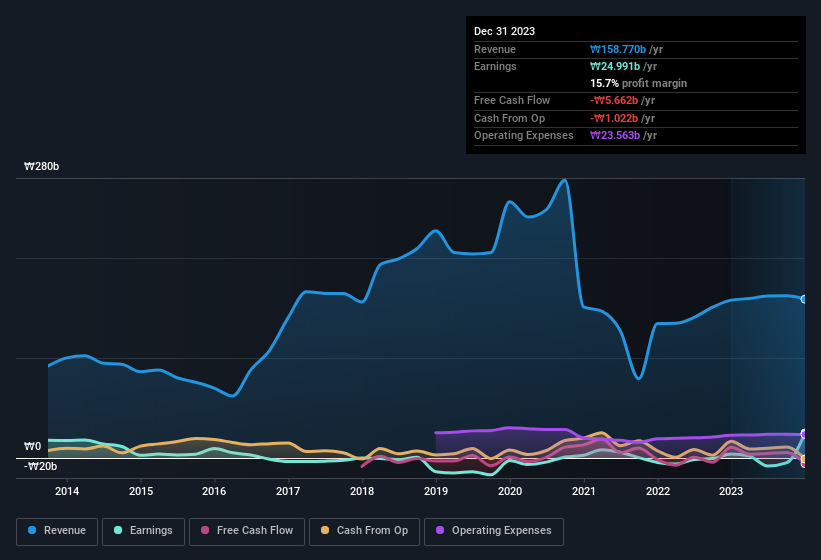

View our latest analysis for Dasan SoluetaLtd

Zooming In On Dasan SoluetaLtd's Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

Dasan SoluetaLtd has an accrual ratio of 0.26 for the year to December 2023. We can therefore deduce that its free cash flow fell well short of covering its statutory profit. In the last twelve months it actually had negative free cash flow, with an outflow of ₩5.7b despite its profit of ₩25.0b, mentioned above. We saw that FCF was ₩11b a year ago though, so Dasan SoluetaLtd has at least been able to generate positive FCF in the past. However, that's not the end of the story. We can look at how unusual items in the profit and loss statement impacted its accrual ratio, as well as explore how dilution is impacting shareholders negatively. One positive for Dasan SoluetaLtd shareholders is that it's accrual ratio was significantly better last year, providing reason to believe that it may return to stronger cash conversion in the future. As a result, some shareholders may be looking for stronger cash conversion in the current year.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Dasan SoluetaLtd.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. In fact, Dasan SoluetaLtd increased the number of shares on issue by 17% over the last twelve months by issuing new shares. That means its earnings are split among a greater number of shares. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. Check out Dasan SoluetaLtd's historical EPS growth by clicking on this link.

How Is Dilution Impacting Dasan SoluetaLtd's Earnings Per Share (EPS)?

We don't have any data on the company's profits from three years ago. On the bright side, in the last twelve months it grew profit by 521%. On the other hand, earnings per share are only up 414% over the same period. Therefore, the dilution is having a noteworthy influence on shareholder returns.

In the long term, earnings per share growth should beget share price growth. So Dasan SoluetaLtd shareholders will want to see that EPS figure continue to increase. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

How Do Unusual Items Influence Profit?

Given the accrual ratio, it's not overly surprising that Dasan SoluetaLtd's profit was boosted by unusual items worth ₩67m in the last twelve months. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. And, after all, that's exactly what the accounting terminology implies. If Dasan SoluetaLtd doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

Our Take On Dasan SoluetaLtd's Profit Performance

In conclusion, Dasan SoluetaLtd's weak accrual ratio suggested its statutory earnings have been inflated by the unusual items. The dilution means the results are weaker when viewed from a per-share perspective. Considering all this we'd argue Dasan SoluetaLtd's profits probably give an overly generous impression of its sustainable level of profitability. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. For example, we've found that Dasan SoluetaLtd has 4 warning signs (2 are a bit concerning!) that deserve your attention before going any further with your analysis.

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A154040

Dasan SoluetaLtd

Operates as a electromagnetic shielding material company in Korea and internationally.

Good value with proven track record.

Market Insights

Community Narratives