- South Korea

- /

- Machinery

- /

- KOSDAQ:A123840

Hanil Vacuum's (KOSDAQ:123840) Earnings Are Built On Soft Foundations

Shareholders didn't seem to be thrilled with Hanil Vacuum Co., Ltd.'s (KOSDAQ:123840) recent earnings report, despite healthy profit numbers. Our analysis suggests they may be concerned about some underlying details.

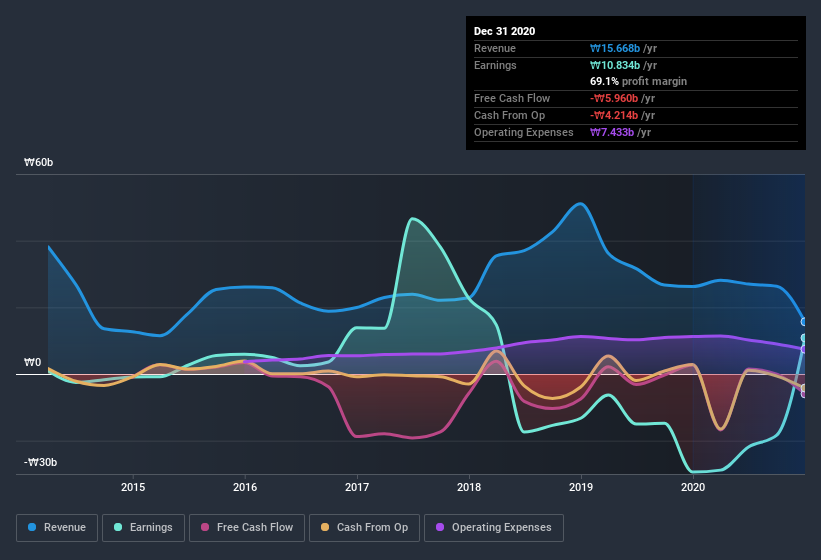

Check out our latest analysis for Hanil Vacuum

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. Hanil Vacuum expanded the number of shares on issue by 39% over the last year. As a result, its net income is now split between a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. You can see a chart of Hanil Vacuum's EPS by clicking here.

A Look At The Impact Of Hanil Vacuum's Dilution on Its Earnings Per Share (EPS).

We don't have any data on the company's profits from three years ago. And even focusing only on the last twelve months, we don't have a meaningful growth rate because it made a loss a year ago, too. What we do know is that while it's great to see a profit over the last twelve months, that profit would have been better, on a per share basis, if the company hadn't needed to issue shares. And so, you can see quite clearly that dilution is having a rather significant impact on shareholders.

In the long term, if Hanil Vacuum's earnings per share can increase, then the share price should too. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Hanil Vacuum.

How Do Unusual Items Influence Profit?

Alongside that dilution, it's also important to note that Hanil Vacuum's profit was boosted by unusual items worth ₩22b in the last twelve months. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. Which is hardly surprising, given the name. We can see that Hanil Vacuum's positive unusual items were quite significant relative to its profit in the year to December 2020. As a result, we can surmise that the unusual items are making its statutory profit significantly stronger than it would otherwise be.

Our Take On Hanil Vacuum's Profit Performance

To sum it all up, Hanil Vacuum got a nice boost to profit from unusual items; without that, its statutory results would have looked worse. And furthermore, it went and issued plenty of new shares, ensuring that each shareholder (who did not tip more money in) now owns a smaller proportion of the company. Considering all this we'd argue Hanil Vacuum's profits probably give an overly generous impression of its sustainable level of profitability. If you want to do dive deeper into Hanil Vacuum, you'd also look into what risks it is currently facing. Case in point: We've spotted 3 warning signs for Hanil Vacuum you should be aware of.

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you decide to trade Hanil Vacuum, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

If you're looking to trade Nuon, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Nuon might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A123840

Adequate balance sheet low.

Market Insights

Community Narratives