- Japan

- /

- Electronic Equipment and Components

- /

- TSE:7213

Lecip Holdings' (TSE:7213) Dividend Will Be Increased To ¥10.00

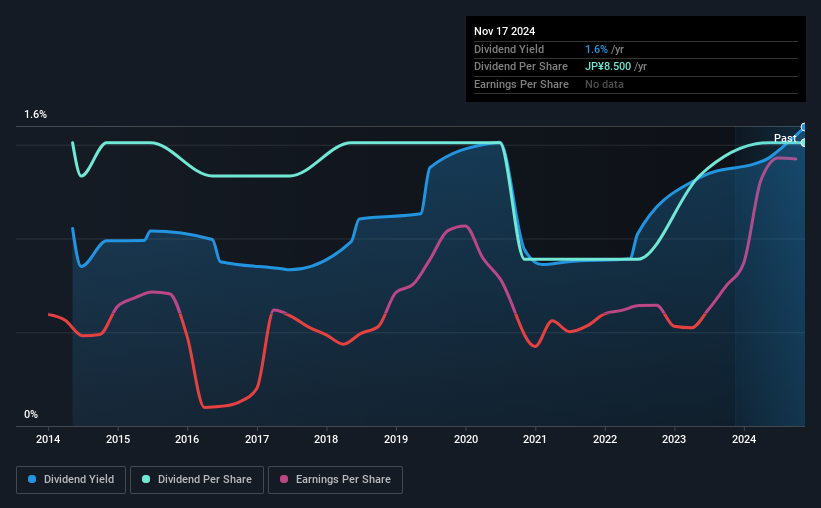

Lecip Holdings Corporation (TSE:7213) will increase its dividend from last year's comparable payment on the 6th of June to ¥10.00. This takes the annual payment to 1.6% of the current stock price, which is about average for the industry.

View our latest analysis for Lecip Holdings

Lecip Holdings' Future Dividend Projections Appear Well Covered By Earnings

We like a dividend to be consistent over the long term, so checking whether it is sustainable is important. However, Lecip Holdings' earnings easily cover the dividend. This means that most of its earnings are being retained to grow the business.

Over the next year, EPS could expand by 11.0% if recent trends continue. Assuming the dividend continues along recent trends, we think the payout ratio could be 4.7% by next year, which is in a pretty sustainable range.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. The payments haven't really changed that much since 10 years ago. We're glad to see the dividend has risen, but with a limited rate of growth and fluctuations in the payments the total shareholder return may be limited.

The Dividend Looks Likely To Grow

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. Lecip Holdings has impressed us by growing EPS at 11% per year over the past five years. With a decent amount of growth and a low payout ratio, we think this bodes well for Lecip Holdings' prospects of growing its dividend payments in the future.

An additional note is that the company has been raising capital by issuing stock equal to 13% of shares outstanding in the last 12 months. Regularly doing this can be detrimental - it's hard to grow dividends per share when new shares are regularly being created.

Lecip Holdings Looks Like A Great Dividend Stock

Overall, a dividend increase is always good, and we think that Lecip Holdings is a strong income stock thanks to its track record and growing earnings. Distributions are quite easily covered by earnings, which are also being converted to cash flows. Taking this all into consideration, this looks like it could be a good dividend opportunity.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Taking the debate a bit further, we've identified 2 warning signs for Lecip Holdings that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7213

Lecip Holdings

Plans, designs, manufactures, and sells lighting, electric power conversion, and information processing equipment for buses, trains, automobiles, and industrial equipment in Japan and internationally.

Flawless balance sheet, good value and pays a dividend.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion

Thanks for sharing these. They really help when I pick what dividend stocks to invest in