FUJIFILM Holdings (TSE:4901) shares have moved lower over the past week, with investors weighing recent price swings against the company’s steady annual revenue and net income growth. The stock’s long-term performance continues to draw attention from those focused on valuation.

FUJIFILM Holdings’ share price has seen a pullback this week, and while momentum has faded slightly in recent sessions, the company’s strong three- and five-year total shareholder returns of 66% and 114% remind investors that its long-term trend remains impressive despite short-term noise.

With shares trading below analyst price targets and steady profit growth, the debate now centers on whether FUJIFILM Holdings is currently undervalued or if the market has already factored in its future potential. Could this be a true buying opportunity?

Advertisement

Price-to-Earnings of 16.8x: Is it justified?

FUJIFILM Holdings’ shares currently trade at a price-to-earnings (P/E) ratio of 16.8x, narrowly above the average for similar companies and the JP Tech industry. With a last close at ¥3,541 and profit growth projected, investors are weighing if this multiple is warranted.

The P/E ratio compares a company’s share price to its per-share earnings, providing insight into how the market values each unit of profit. For a diversified technology company like FUJIFILM Holdings, this metric serves as a quick gauge of investor sentiment about future profitability relative to peers and the industry overall.

While the company’s earnings are forecast to grow at a moderate rate, this slightly higher than average multiple signals the market may be building in positive expectations for continued profit growth and operational stability. The P/E ratio also stands notably below our estimate of the fair P/E (20.6x), suggesting there could be room for a rerating if these expectations are met.

Compared to the broader JP Tech industry average P/E of 14.5x, FUJIFILM Holdings is trading at a premium. This is marginal when considered alongside its profit track record and earnings quality. The market could be anticipating outperformance ahead, and the fair value benchmark gives a sense of where the multiple might trend if sentiment shifts.

However, sluggish annual revenue growth and weaker short-term returns may challenge bullish expectations if momentum does not recover in the coming quarters.

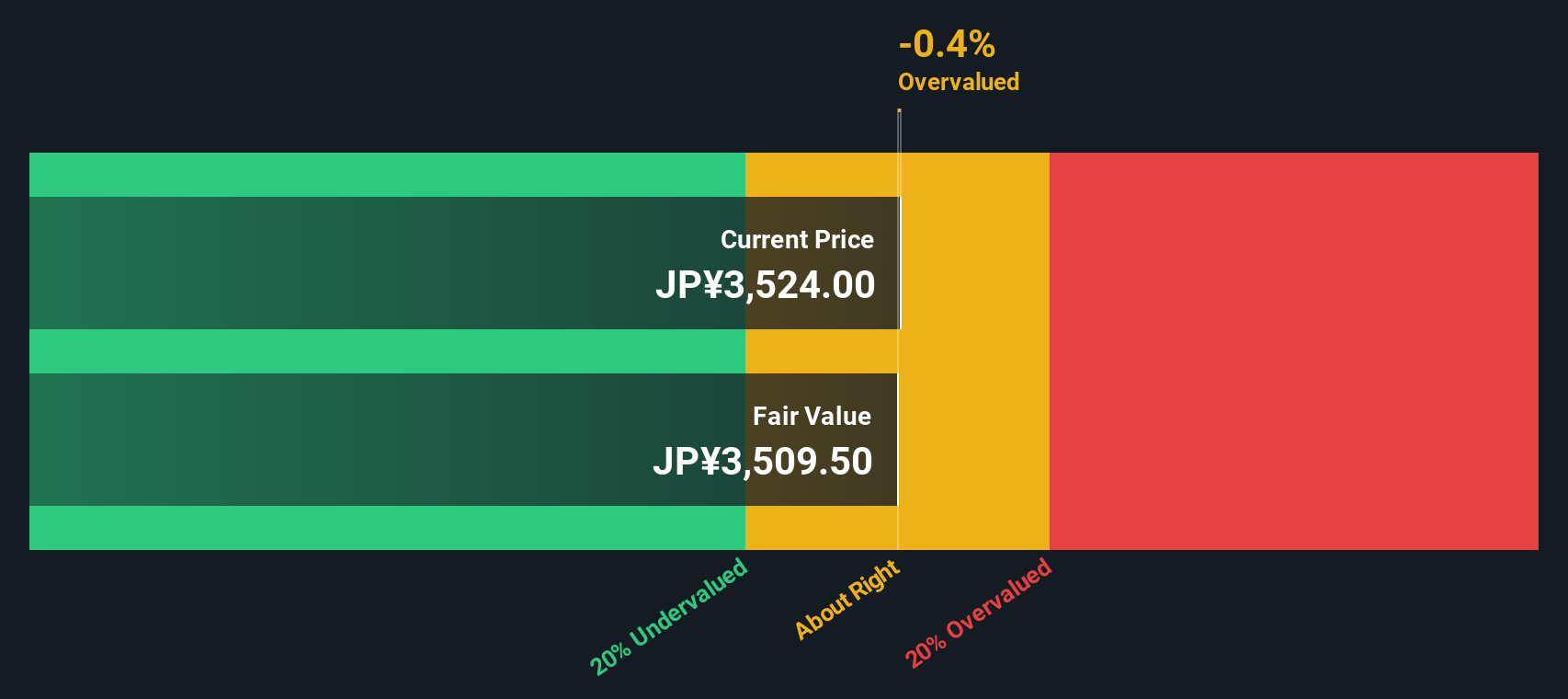

Looking at valuation from a different angle, our SWS DCF model suggests FUJIFILM Holdings may be trading slightly above its estimated fair value of ¥3,511. This perspective provides a more cautious read on the current price, indicating that upside might be limited unless future growth surprises. Does this lens change the risk profile for investors?

For those wanting to take a different approach or dig deeper into the numbers, you can customize your own take in just a few minutes. Do it your way

A great starting point for your FUJIFILM Holdings research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don't wait on the sidelines. Gain an edge by checking out investment opportunities that match your goals. Take action now to stay ahead of the market curve!

Capture double-digit yields and strengthen your income potential by checking out these 18 dividend stocks with yields > 3% for reliable dividend payers with impressive returns.

Ride the next wave in digital innovation by targeting companies behind major breakthroughs with these 25 AI penny stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

Provides products and services in the fields of healthcare, electronics, business innovation, and imaging in Japan, the United States, Asia, and internationally.