- Japan

- /

- Specialty Stores

- /

- TSE:7599

IDOM Inc. (TSE:7599) Held Back By Insufficient Growth Even After Shares Climb 39%

Despite an already strong run, IDOM Inc. (TSE:7599) shares have been powering on, with a gain of 39% in the last thirty days. The last 30 days bring the annual gain to a very sharp 69%.

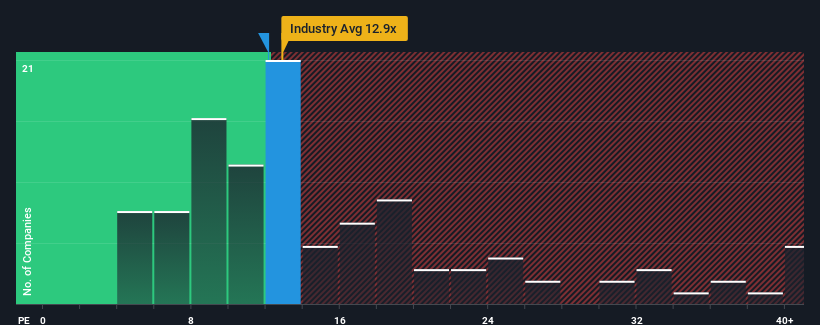

Even after such a large jump in price, IDOM may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 12.1x, since almost half of all companies in Japan have P/E ratios greater than 15x and even P/E's higher than 24x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

IDOM hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. The P/E is probably low because investors think this poor earnings performance isn't going to get any better. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for IDOM

Does Growth Match The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as IDOM's is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered a frustrating 19% decrease to the company's bottom line. Still, the latest three year period has seen an excellent 672% overall rise in EPS, in spite of its unsatisfying short-term performance. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

Shifting to the future, estimates from the four analysts covering the company suggest earnings should grow by 4.7% per annum over the next three years. With the market predicted to deliver 11% growth per year, the company is positioned for a weaker earnings result.

With this information, we can see why IDOM is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What We Can Learn From IDOM's P/E?

Despite IDOM's shares building up a head of steam, its P/E still lags most other companies. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that IDOM maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

You need to take note of risks, for example - IDOM has 3 warning signs (and 2 which make us uncomfortable) we think you should know about.

Of course, you might also be able to find a better stock than IDOM. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7599

IDOM

IDOM Inc. purchases and sells used cars in Japan and internationally.

Solid track record and good value.

Market Insights

Community Narratives