As December 2024 unfolds, global markets are navigating a complex landscape marked by cautious Federal Reserve commentary and political uncertainty, which have led to broad-based declines across major indices. Smaller-cap stocks have been particularly affected in this environment, with the S&P 600 experiencing notable challenges amid tempered expectations for future rate cuts and looming government shutdown fears. In such uncertain times, identifying promising opportunities often involves seeking out stocks that demonstrate resilience through strong fundamentals and potential for growth despite broader market headwinds.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Resource Alam Indonesia | 2.66% | 30.36% | 43.87% | ★★★★★★ |

| Philippine Savings Bank | NA | 5.49% | 20.73% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Mandiri Herindo Adiperkasa | NA | 20.72% | 11.08% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Arab Insurance Group (B.S.C.) | NA | -59.20% | 20.33% | ★★★★★☆ |

| Eclatorq Technology | 37.47% | 8.43% | 18.41% | ★★★★★☆ |

| Chita Kogyo | 8.34% | 2.84% | 8.49% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Yuan Cheng CableLtd | 112.32% | 6.17% | 58.39% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

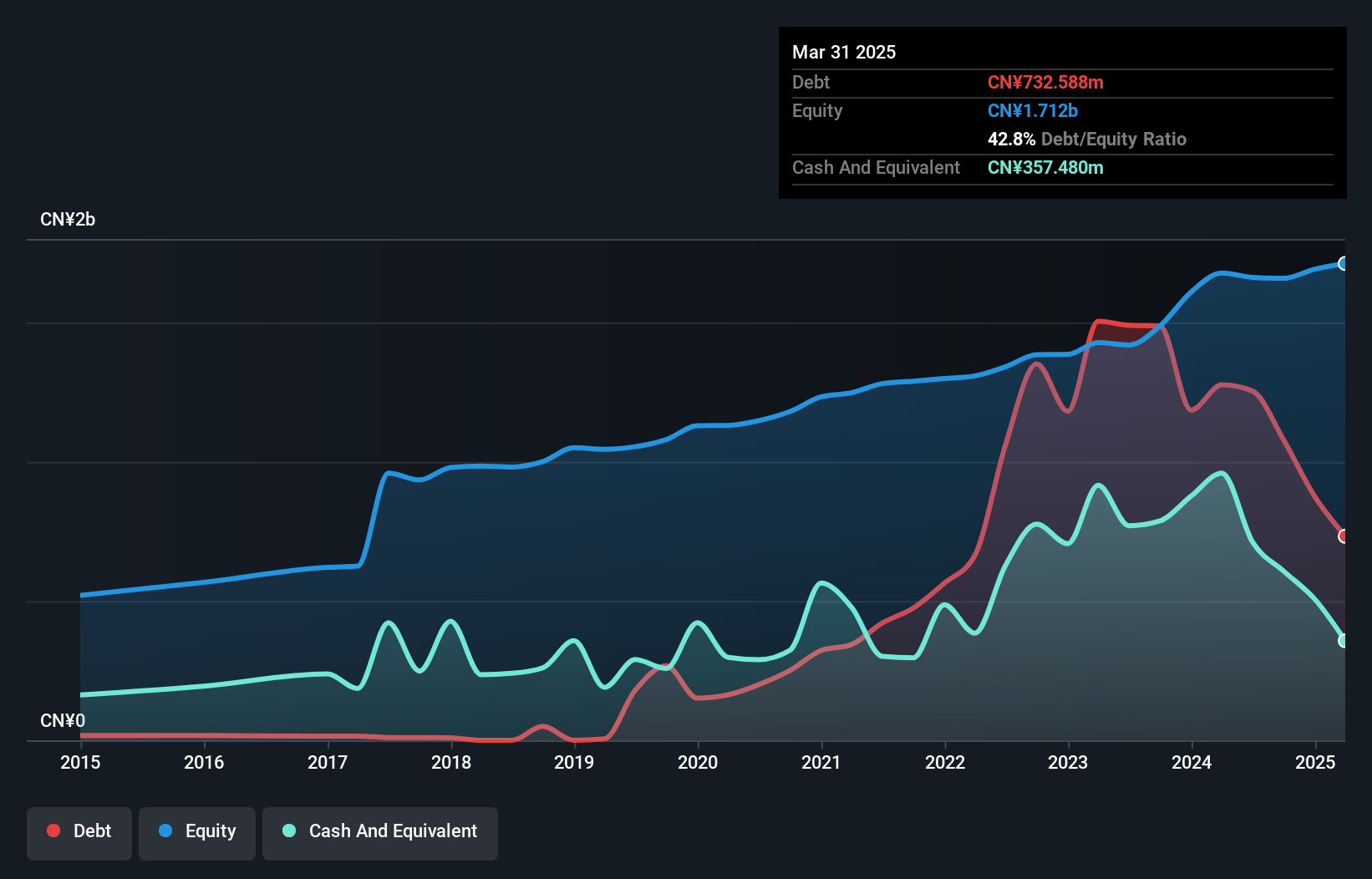

Shijiazhuang Kelin Electric (SHSE:603050)

Simply Wall St Value Rating: ★★★★★☆

Overview: Shijiazhuang Kelin Electric Co., Ltd. designs, manufactures, and sells electrical power distribution and metering products in China with a market cap of approximately CN¥5.79 billion.

Operations: Kelin Electric generates its revenue primarily from the electrical equipment manufacturing industry, amounting to approximately CN¥4.19 billion.

Kelin Electric, a smaller player in the electrical industry, appears undervalued at 84.7% below its estimated fair value. The company's debt to equity ratio has risen from 24.8% to 65% over five years, yet its net debt to equity remains satisfactory at 28.4%. Despite this leverage increase, Kelin's earnings growth of 48.7% last year outpaced the industry's 1.1%, showcasing strong performance relative to peers. However, recent figures reveal net income of CNY 148 million for nine months ending September compared to CNY 179 million prior year, indicating some challenges despite positive cash flow and robust EBIT coverage of interest payments at 8.8 times.

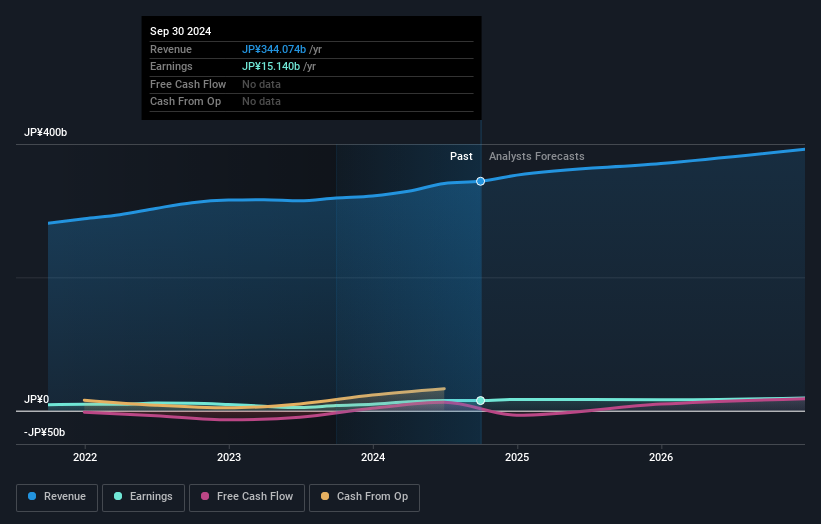

artience (TSE:4634)

Simply Wall St Value Rating: ★★★★★☆

Overview: Artience Co., Ltd. operates in the colorants and functional materials, polymers and coatings, printing and information, and packaging materials sectors across various regions worldwide, with a market capitalization of ¥156.29 billion.

Operations: The company generates significant revenue from its core segments, with the packaging materials business contributing ¥89.02 billion and polymers and coatings bringing in ¥85.51 billion. The printing and information segment adds ¥82.75 billion, while colorants and functional materials contribute ¥85.52 billion to its revenue streams.

Artience, a company with promising potential, has been making waves with its recent performance and strategic moves. Trading significantly below its estimated fair value by 79.5%, it offers an attractive entry point for investors. The firm reported impressive earnings growth of 94.9% over the past year, outpacing the broader Chemicals industry growth of 14%. With a net debt to equity ratio at a satisfactory level of 9.1%, Artience displays financial prudence while maintaining high-quality earnings and positive free cash flow. Recently, it completed a share buyback program worth ¥1,291 million, enhancing shareholder value amidst volatile market conditions.

- Delve into the full analysis health report here for a deeper understanding of artience.

Explore historical data to track artience's performance over time in our Past section.

Japan Investment Adviser (TSE:7172)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Japan Investment Adviser Co., Ltd. offers a range of financial solutions in Japan and has a market capitalization of approximately ¥65.20 billion.

Operations: The company generates revenue primarily through its Finance Solution segment, which contributes ¥28.10 billion. The net profit margin is a key financial indicator to consider when evaluating its profitability.

Japan Investment Adviser, a nimble player in the financial sector, has shown remarkable earnings growth of 289.8% over the past year, outpacing the broader Diversified Financial industry. Despite a hefty net debt to equity ratio of 159.2%, which is considered high, its interest payments are well covered with an EBIT coverage of 7.8 times. The company trades at a substantial discount of 40.2% below its estimated fair value, offering potential upside for investors seeking undervalued opportunities. Recent management changes and strategic shifts suggest a focus on strengthening sales operations and adapting to market dynamics amidst currency fluctuations impacting profits.

- Get an in-depth perspective on Japan Investment Adviser's performance by reading our health report here.

Gain insights into Japan Investment Adviser's past trends and performance with our Past report.

Seize The Opportunity

- Gain an insight into the universe of 4625 Undiscovered Gems With Strong Fundamentals by clicking here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4634

artience

Engages in the colorants and functional materials, polymers and coatings, printing and information, and packaging materials businesses in Japan, China, Europe, Africa, Asia, the Americas, and internationally.

Undervalued with solid track record and pays a dividend.