Advertisement

The five-year decline in earnings might be taking its toll on Kureha (TSE:4023) shareholders as stock falls 6.0% over the past week

These days it's easy to simply buy an index fund, and your returns should (roughly) match the market. But in our experience, buying the right stocks can give your wealth a significant boost. For example, the Kureha Corporation (TSE:4023) share price is 85% higher than it was five years ago, which is more than the market average. In comparison, the share price is down 1.0% in a year.

In light of the stock dropping 6.0% in the past week, we want to investigate the longer term story, and see if fundamentals have been the driver of the company's positive five-year return.

To quote Buffett, 'Ships will sail around the world but the Flat Earth Society will flourish. There will continue to be wide discrepancies between price and value in the marketplace...' One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

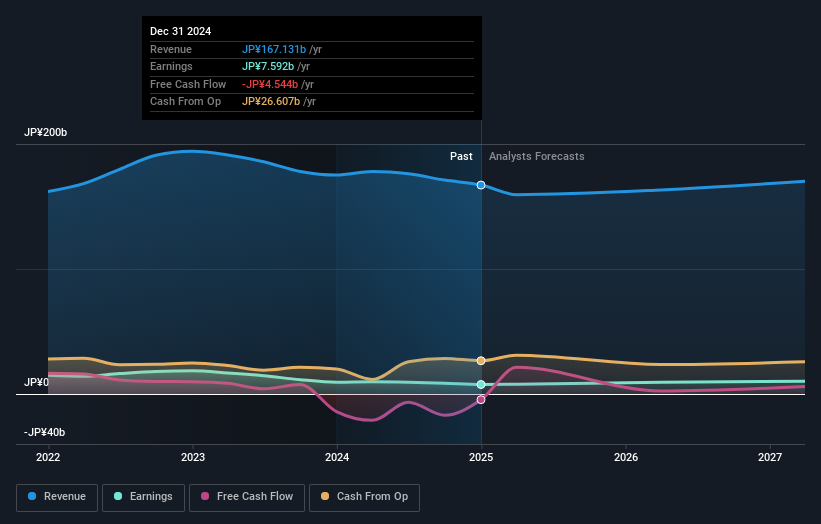

Kureha's earnings per share are down 17% per year, despite strong share price performance over five years.

This means it's unlikely the market is judging the company based on earnings growth. Since the change in EPS doesn't seem to correlate with the change in share price, it's worth taking a look at other metrics.

On the other hand, Kureha's revenue is growing nicely, at a compound rate of 5.4% over the last five years. In that case, the company may be sacrificing current earnings per share to drive growth.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

If you are thinking of buying or selling Kureha stock, you should check out this FREE detailed report on its balance sheet .

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. It's fair to say that the TSR gives a more complete picture for stocks that pay a dividend. As it happens, Kureha's TSR for the last 5 years was 114%, which exceeds the share price return mentioned earlier. The dividends paid by the company have thusly boosted the total shareholder return.

A Different Perspective

It's good to see that Kureha has rewarded shareholders with a total shareholder return of 2.1% in the last twelve months. Of course, that includes the dividend. However, that falls short of the 16% TSR per annum it has made for shareholders, each year, over five years. The pessimistic view would be that be that the stock has its best days behind it, but on the other hand the price might simply be moderating while the business itself continues to execute. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Case in point: We've spotted 2 warning signs for Kureha you should be aware of.

We will like Kureha better if we see some big insider buys. While we wait, check out this free list of undervalued stocks (mostly small caps) with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Japanese exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Kureha might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:4023

Kureha

Manufactures and sells functional materials, specialty chemicals, and plastics in Japan and internationally.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality Assets, Cautious Expansion and Commodity Super-cycle To Deliver Steady Revenue Growth

Fair Value US$20.44|13.6% undervalued

ST

Equity Analyst and Writer

Tullow Oil's Share Price Could Soar Up to 135% if Oil Holds at $70

Fair Value UK£0.45|69.8% undervalued

OI

Community Contributor