Advertisement

- Taiwan

- /

- Metals and Mining

- /

- TWSE:2020

3 Reliable Dividend Stocks Offering Yields Up To 6.7%

Simply Wall St

Reviewed by Simply Wall St

With global markets experiencing a boost from cooling inflation and strong bank earnings, major U.S. stock indexes have rebounded, highlighting the resilience of value stocks over growth shares. Amidst this backdrop of economic optimism, investors often look for reliable dividend stocks that can provide steady income streams, particularly in sectors showing robust performance like financials and energy.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Peoples Bancorp (NasdaqGS:PEBO) | 5.11% | ★★★★★★ |

| Tsubakimoto Chain (TSE:6371) | 4.32% | ★★★★★★ |

| Wuliangye YibinLtd (SZSE:000858) | 3.48% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.68% | ★★★★★★ |

| Southside Bancshares (NYSE:SBSI) | 4.49% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 4.13% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 3.47% | ★★★★★★ |

| Nihon Parkerizing (TSE:4095) | 4.03% | ★★★★★★ |

| Premier Financial (NasdaqGS:PFC) | 4.93% | ★★★★★★ |

| Citizens & Northern (NasdaqCM:CZNC) | 5.89% | ★★★★★★ |

Click here to see the full list of 1981 stocks from our Top Dividend Stocks screener.

Here's a peek at a few of the choices from the screener.

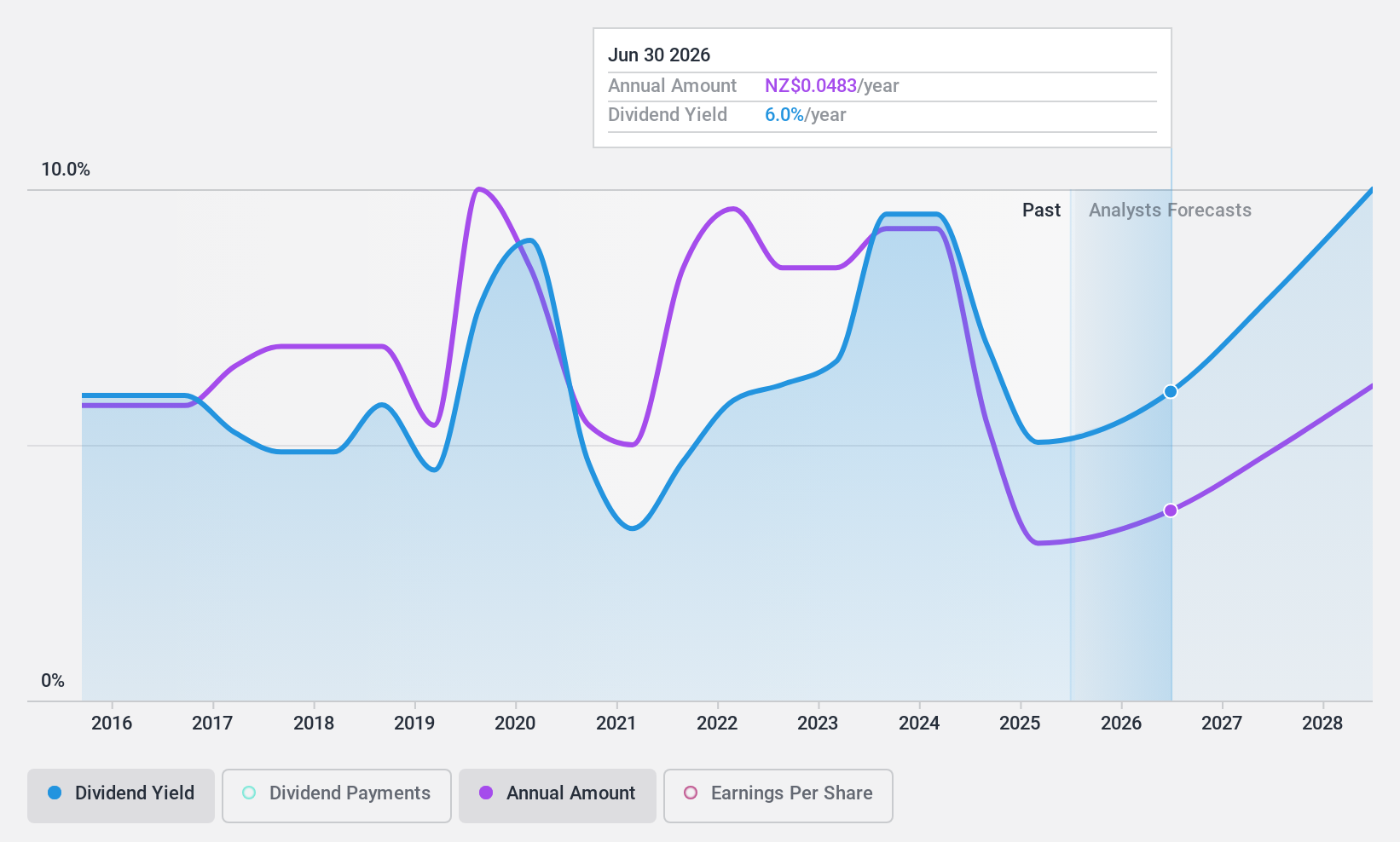

Heartland Group Holdings (NZSE:HGH)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Heartland Group Holdings Limited operates in New Zealand and Australia, offering a range of financial services, with a market cap of NZ$956.17 million.

Operations: Heartland Group Holdings Limited generates revenue from various segments, including Motor (NZ$39.68 million), Rural (NZ$32.16 million), Business (NZ$49.64 million), Personal Lending (NZ$4.42 million), Reverse Mortgages (NZ$49.24 million), and the Australian Banking Group (NZ$70.33 million).

Dividend Yield: 6.8%

Heartland Group Holdings offers a dividend yield of 6.8%, placing it in the top 25% of New Zealand dividend payers, with a current payout ratio of 71.1% and expected coverage improvement to 53% in three years. Despite this, its dividends have been volatile and unreliable over the past decade. Additionally, the company faces challenges with high bad loans at 2.2% and low allowance for these loans at 48%.

- Click here to discover the nuances of Heartland Group Holdings with our detailed analytical dividend report.

- Our valuation report here indicates Heartland Group Holdings may be overvalued.

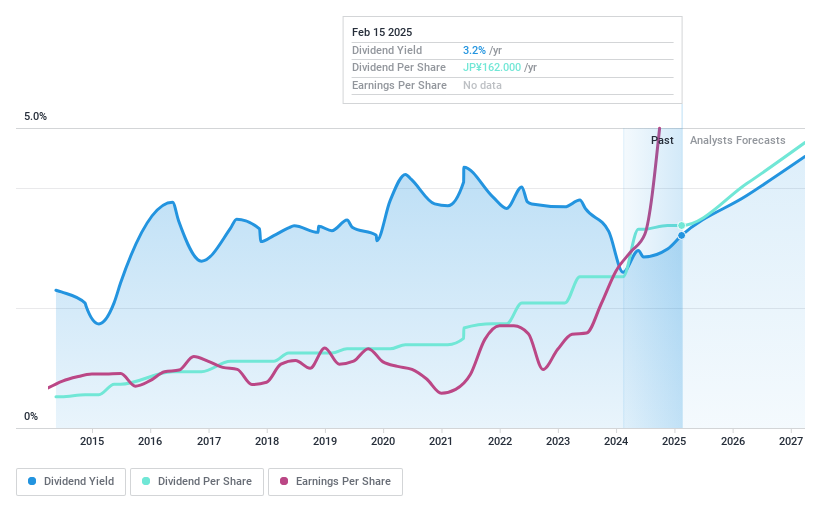

Tokio Marine Holdings (TSE:8766)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Tokio Marine Holdings, Inc. operates in the non-life and life insurance sectors, as well as financial and general businesses both in Japan and internationally, with a market cap of ¥10.34 trillion.

Operations: Tokio Marine Holdings generates revenue primarily from its Domestic Non-Life Insurance Business at ¥3.76 billion, International Insurance Business at ¥3.99 billion, and Domestic Life Insurance at ¥579.21 million, along with contributions from Finance Other Businesses totaling ¥106.68 million.

Dividend Yield: 3%

Tokio Marine Holdings provides a stable dividend yield of 3.05%, with payments reliably increasing over the past decade and well-covered by earnings and cash flows, given a low payout ratio of 23.9% and cash payout ratio of 32%. While trading below fair value, recent share buybacks, totaling ¥47.57 billion for 0.43% of shares, reflect a flexible capital strategy but do not significantly impact dividend attractiveness compared to top-tier payers in Japan.

- Click here and access our complete dividend analysis report to understand the dynamics of Tokio Marine Holdings.

- Upon reviewing our latest valuation report, Tokio Marine Holdings' share price might be too pessimistic.

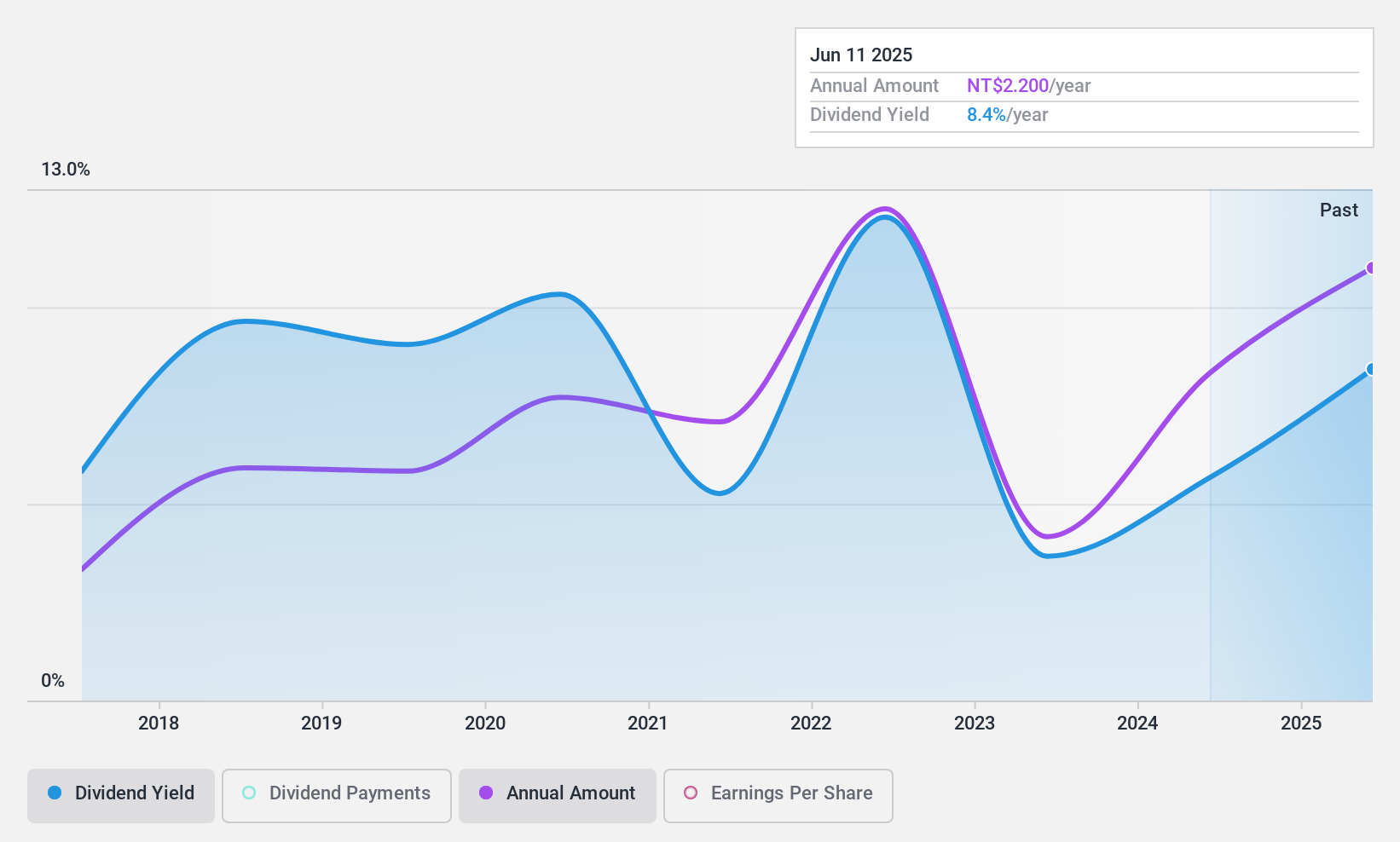

Mayer Steel Pipe (TWSE:2020)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Mayer Steel Pipe Corporation processes and sells steel pipes, plates, and other metal products in Taiwan with a market cap of NT$7.30 billion.

Operations: Mayer Steel Pipe Corporation generates revenue primarily from its Steel Department, which accounts for NT$5.33 billion, and also earns from its Hotel Services Department with NT$197.10 million in revenue.

Dividend Yield: 6.1%

Mayer Steel Pipe's dividend yield of 6.09% ranks in the top 25% of Taiwan's market, yet its dividends have been volatile and unreliable over the past decade. Despite a low payout ratio of 37.6%, dividends are not well-covered by cash flows, evidenced by a high cash payout ratio of 173.3%. The Price-To-Earnings ratio is favorable at 6.2x compared to the market average, but recent earnings show decreased sales and net income year-on-year.

- Get an in-depth perspective on Mayer Steel Pipe's performance by reading our dividend report here.

- In light of our recent valuation report, it seems possible that Mayer Steel Pipe is trading beyond its estimated value.

Key Takeaways

- Reveal the 1981 hidden gems among our Top Dividend Stocks screener with a single click here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:2020

Mayer Steel Pipe

Processes and sells steel pipes, plates, and other metal products in Taiwan.

Excellent balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor