Did Buyback, Dividend Hike, and Upbeat Forecast Just Shift Japan Post Insurance's (TSE:7181) Investment Narrative?

Reviewed by Sasha Jovanovic

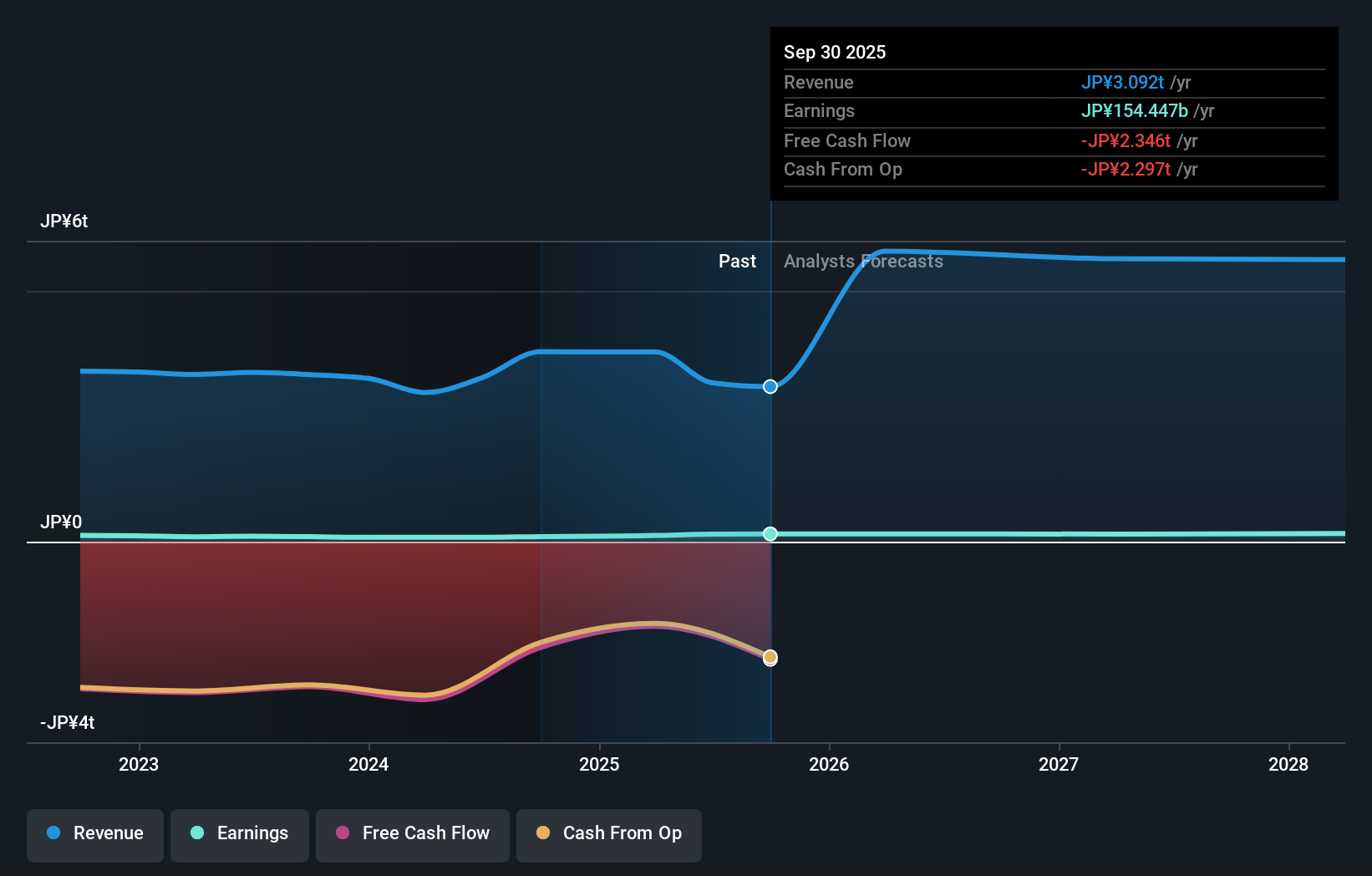

- On November 14, 2025, Japan Post Insurance announced a buyback of up to 20 million shares (5.38% of issued capital) for ¥4 billion, accompanied by a raised full-year earnings forecast and a second-quarter dividend increase to ¥62 per share.

- This combination of stronger guidance, an enhanced dividend, and a substantial share repurchase reflects management’s increased confidence in capital efficiency and shareholder returns.

- Let’s explore how the new buyback program and improved earnings outlook may influence Japan Post Insurance’s investment narrative going forward.

These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Japan Post Insurance Investment Narrative Recap

To be a shareholder in Japan Post Insurance, you need to see value in its ability to capture demand for life insurance in an aging Japan while bolstering earnings through operational efficiency and improved capital management. The recent share buyback, stronger earnings guidance, and dividend hike reinforce management’s focus on shareholder value, yet the most important short-term catalyst, continued growth in new policy sales, remains more dependent on demographic momentum than this announcement, with market skepticism around earnings sustainability still presenting a meaningful risk.

Among the recent updates, the company’s upward revision to full-year earnings guidance is especially relevant, as it points to improved investment income and cost controls supporting higher profits per share. This not only complements the buyback and higher dividend, but also addresses the catalyst of translating digital transformation and salesforce enhancements into tangible margin expansion, as the insurance sector in Japan pivots to meet evolving policyholder needs.

However, it’s important for investors to recognize that, despite these financial improvements, persistent doubts over long-term earnings quality and the company’s relatively low price-to-book and price-to-earnings multiples reflect...

Read the full narrative on Japan Post Insurance (it's free!)

Japan Post Insurance's narrative projects ¥6,605.3 billion in revenue and ¥152.1 billion in earnings by 2028. This implies a 25.2% annual revenue growth rate and a ¥14.9 billion earnings increase from ¥137.2 billion today.

Uncover how Japan Post Insurance's forecasts yield a ¥4282 fair value, in line with its current price.

Exploring Other Perspectives

The Simply Wall St Community estimates only one fair value for Japan Post Insurance at ¥8,685,120, highlighting a stark difference from current valuations. While upbeat earnings guidance suggests stronger near-term results, concerns about profit sustainability persist and are shaping how some investors view the company's longer-term performance.

Explore another fair value estimate on Japan Post Insurance - why the stock might be worth over 2x more than the current price!

Build Your Own Japan Post Insurance Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Japan Post Insurance research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Japan Post Insurance research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Japan Post Insurance's overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7181

Japan Post Insurance

Provides life insurance products and services in Japan.

Undervalued with acceptable track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)