Advertisement

- Japan

- /

- Personal Products

- /

- TSE:4527

Rohto Pharmaceutical Co.,Ltd.'s (TSE:4527) Earnings Haven't Escaped The Attention Of Investors

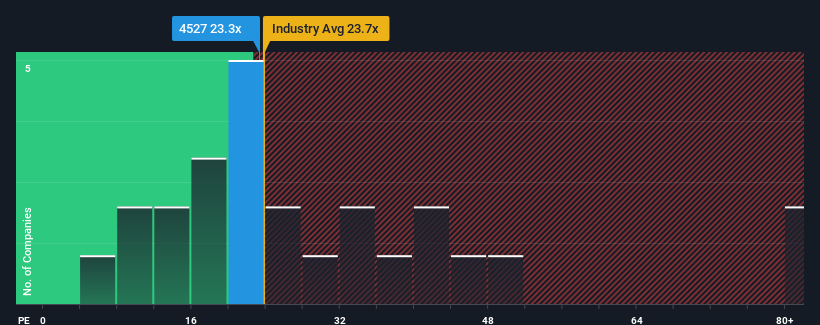

Rohto Pharmaceutical Co.,Ltd.'s (TSE:4527) price-to-earnings (or "P/E") ratio of 23.3x might make it look like a strong sell right now compared to the market in Japan, where around half of the companies have P/E ratios below 13x and even P/E's below 9x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Rohto PharmaceuticalLtd could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Rohto PharmaceuticalLtd

Is There Enough Growth For Rohto PharmaceuticalLtd?

The only time you'd be truly comfortable seeing a P/E as steep as Rohto PharmaceuticalLtd's is when the company's growth is on track to outshine the market decidedly.

Retrospectively, the last year delivered a frustrating 8.4% decrease to the company's bottom line. This has soured the latest three-year period, which nevertheless managed to deliver a decent 28% overall rise in EPS. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been mostly respectable for the company.

Looking ahead now, EPS is anticipated to climb by 16% per year during the coming three years according to the nine analysts following the company. That's shaping up to be materially higher than the 11% per annum growth forecast for the broader market.

With this information, we can see why Rohto PharmaceuticalLtd is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Rohto PharmaceuticalLtd's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

You always need to take note of risks, for example - Rohto PharmaceuticalLtd has 1 warning sign we think you should be aware of.

Of course, you might also be able to find a better stock than Rohto PharmaceuticalLtd. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:4527

Rohto PharmaceuticalLtd

Manufactures and markets pharmaceutical products, cosmetics, and functional foods worldwide.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|31.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|53.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.4% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|54.5% undervalued

AX

Community Contributor