Advertisement

As Japan's stock markets face recent downturns, with the Nikkei 225 Index down 5.8% and the broader TOPIX Index losing 4.2%, investors are keenly observing companies that show resilience and growth potential. In such a volatile environment, stocks with high insider ownership often signal confidence from those closest to the company's operations, making them attractive for their perceived stability and growth prospects. Understanding what makes a good stock in these conditions involves looking at companies that not only have strong earnings growth but also significant insider investment—indicating that those who know the business best are betting on its future success.

Top 10 Growth Companies With High Insider Ownership In Japan

| Name | Insider Ownership | Earnings Growth |

| Micronics Japan (TSE:6871) | 15.3% | 32.7% |

| Hottolink (TSE:3680) | 27% | 61.5% |

| Kasumigaseki CapitalLtd (TSE:3498) | 34.7% | 43.5% |

| Medley (TSE:4480) | 34% | 30.4% |

| Kanamic NetworkLTD (TSE:3939) | 25% | 28.3% |

| ExaWizards (TSE:4259) | 22% | 63% |

| Money Forward (TSE:3994) | 21.4% | 68.1% |

| Astroscale Holdings (TSE:186A) | 21.3% | 90% |

| Loadstar Capital K.K (TSE:3482) | 33.8% | 24.3% |

| AeroEdge (TSE:7409) | 10.7% | 25.3% |

Underneath we present a selection of stocks filtered out by our screen.

S Foods (TSE:2292)

Simply Wall St Growth Rating: ★★★★☆☆

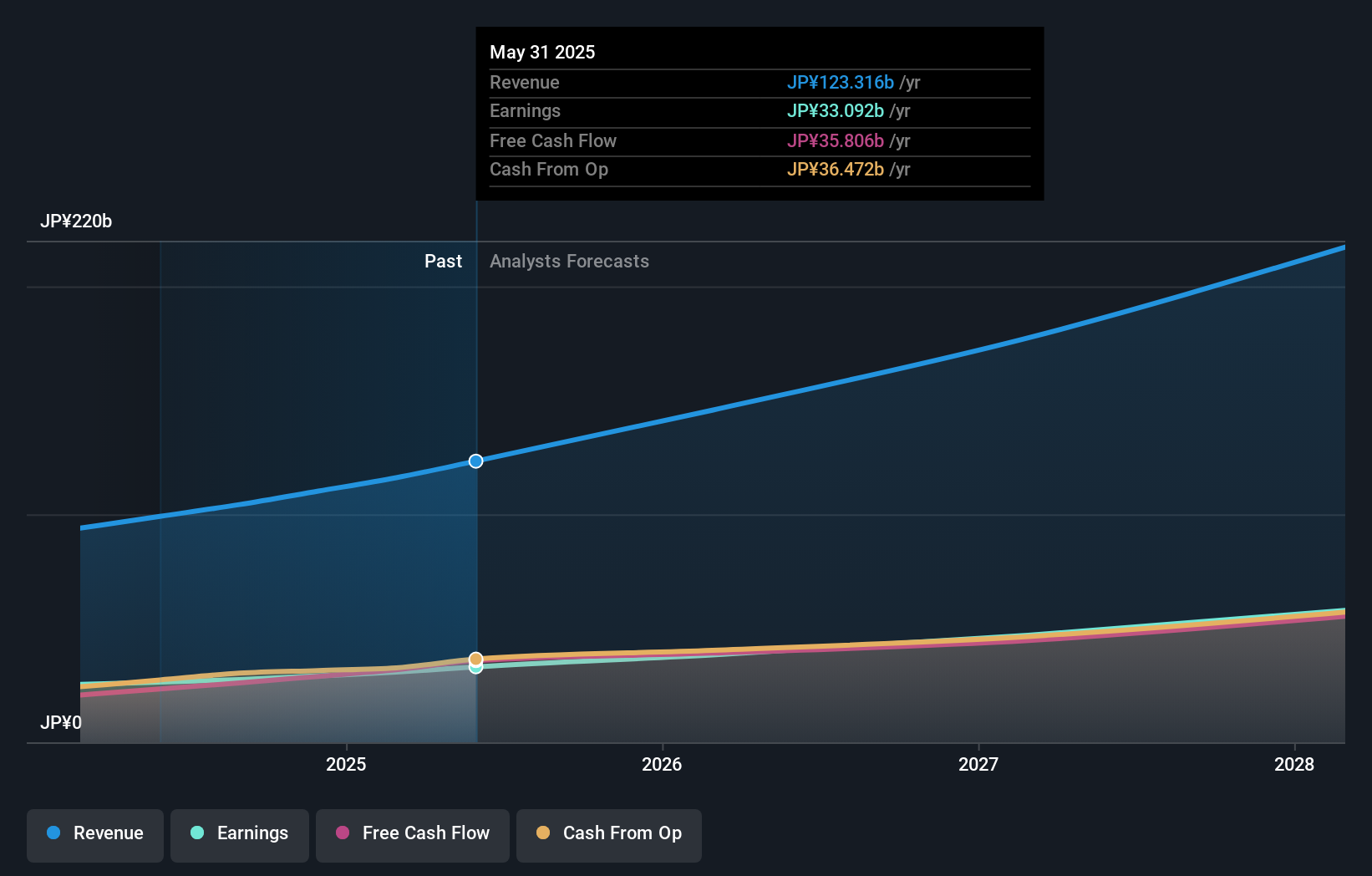

Overview: S Foods Inc. is a Japanese meat company involved in the manufacture, wholesaling, retailing, and food servicing of meat-related products with a market cap of ¥82.98 billion.

Operations: The company's revenue segments include manufacturing, wholesaling, retailing, and food servicing of meat-related products in Japan.

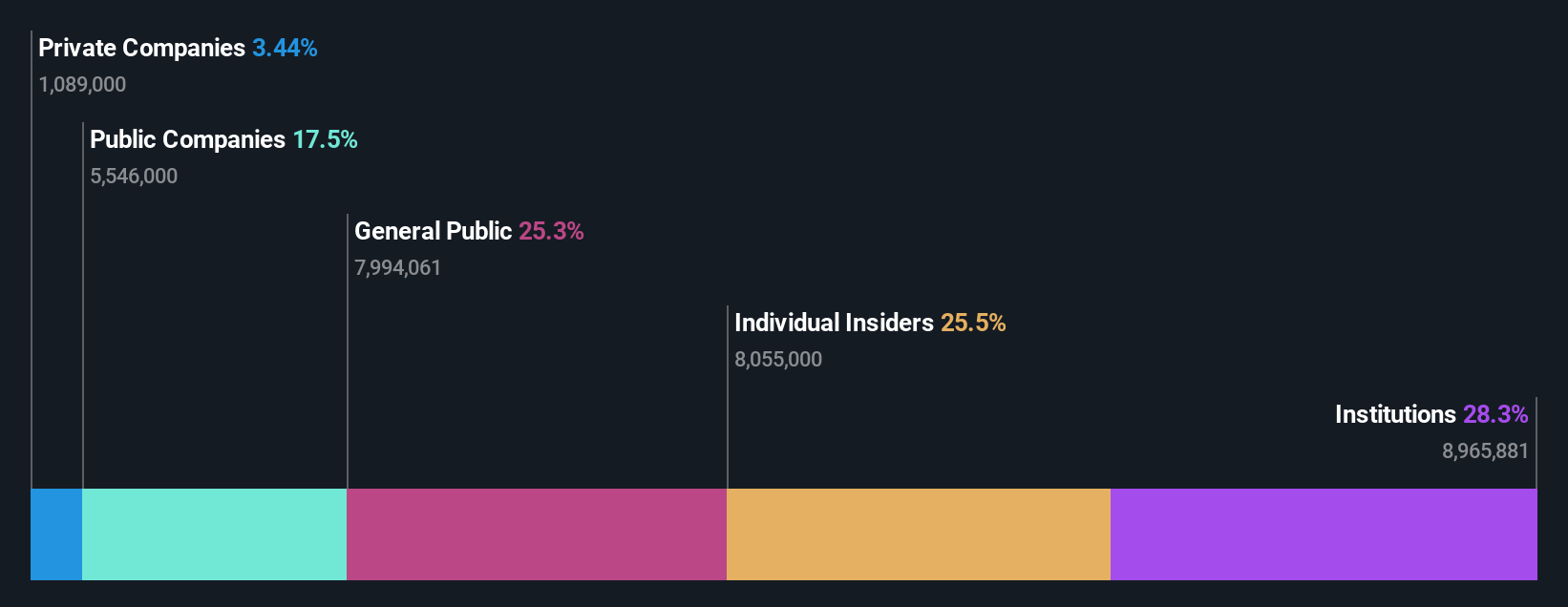

Insider Ownership: 25.5%

Earnings Growth Forecast: 22.4% p.a.

S Foods, a growth company with high insider ownership in Japan, is trading at 39% below its estimated fair value. Despite a decline in profit margins from 2.7% to 1.4%, the company's earnings are forecast to grow significantly at 22.4% annually, outpacing the JP market's average of 8.5%. However, revenue growth is expected to be moderate at 7.8% per year and return on equity is projected to remain low at 10.1%.

- Unlock comprehensive insights into our analysis of S Foods stock in this growth report.

- Upon reviewing our latest valuation report, S Foods' share price might be too pessimistic.

Round One (TSE:4680)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Round One Corporation operates indoor leisure complex facilities and has a market cap of ¥265.39 billion.

Operations: The company's revenue segments include various indoor entertainment activities such as bowling, amusement games, karaoke, and sports facilities.

Insider Ownership: 35.2%

Earnings Growth Forecast: 10.4% p.a.

Round One, with substantial insider ownership, is trading at 62.4% below its estimated fair value and offers good relative value compared to peers. The company reported robust earnings growth of 57.7% over the past year and forecasts indicate annual revenue growth of 6.8%, outpacing the JP market's 4.2%. Despite a highly volatile share price recently, earnings are expected to grow at 10.35% annually, surpassing the market average of 8.5%.

- Delve into the full analysis future growth report here for a deeper understanding of Round One.

- The analysis detailed in our Round One valuation report hints at an deflated share price compared to its estimated value.

BayCurrent Consulting (TSE:6532)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BayCurrent Consulting, Inc. offers consulting services in Japan and has a market cap of ¥732.82 billion.

Operations: BayCurrent Consulting, Inc. generates revenue through its consulting services in Japan.

Insider Ownership: 13.9%

Earnings Growth Forecast: 18.8% p.a.

BayCurrent Consulting, with significant insider ownership, is trading at 48.6% below its estimated fair value and demonstrates strong growth potential. The company's earnings are forecast to grow at 18.8% annually, outpacing the JP market's 8.5%. Revenue is also expected to increase by 18.6% per year, higher than the market average of 4.2%. Despite not reaching a significant growth threshold of over 20%, BayCurrent's projected Return on Equity in three years stands at a robust 35.5%.

- Dive into the specifics of BayCurrent Consulting here with our thorough growth forecast report.

- Insights from our recent valuation report point to the potential overvaluation of BayCurrent Consulting shares in the market.

Summing It All Up

- Access the full spectrum of 101 Fast Growing Japanese Companies With High Insider Ownership by clicking on this link.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:2292

S Foods

A meat company, engages in manufacture, wholesaling, retailing, and food servicing of meat-related food products in Japan.

Excellent balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|33.9% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|26.5% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.3% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor