- Japan

- /

- Real Estate

- /

- TSE:3498

Top Japanese Growth Stocks With Insider Ownership In October 2024

Reviewed by Simply Wall St

In October 2024, Japan's stock markets have experienced volatility amid political changes and global economic uncertainties, with the Nikkei 225 Index and TOPIX Index both seeing declines. Despite these challenges, growth companies with high insider ownership can offer unique opportunities as they often demonstrate strong alignment between management and shareholder interests.

Top 10 Growth Companies With High Insider Ownership In Japan

| Name | Insider Ownership | Earnings Growth |

| Micronics Japan (TSE:6871) | 15.3% | 31.5% |

| Hottolink (TSE:3680) | 26.1% | 61.5% |

| Kasumigaseki CapitalLtd (TSE:3498) | 34.7% | 38.5% |

| Medley (TSE:4480) | 34% | 30.4% |

| Inforich (TSE:9338) | 19.1% | 29.5% |

| Kanamic NetworkLTD (TSE:3939) | 25% | 28.3% |

| ExaWizards (TSE:4259) | 22% | 75.2% |

| Money Forward (TSE:3994) | 21.4% | 68.1% |

| Soracom (TSE:147A) | 16.5% | 54.1% |

| freee K.K (TSE:4478) | 23.9% | 74.1% |

Let's take a closer look at a couple of our picks from the screened companies.

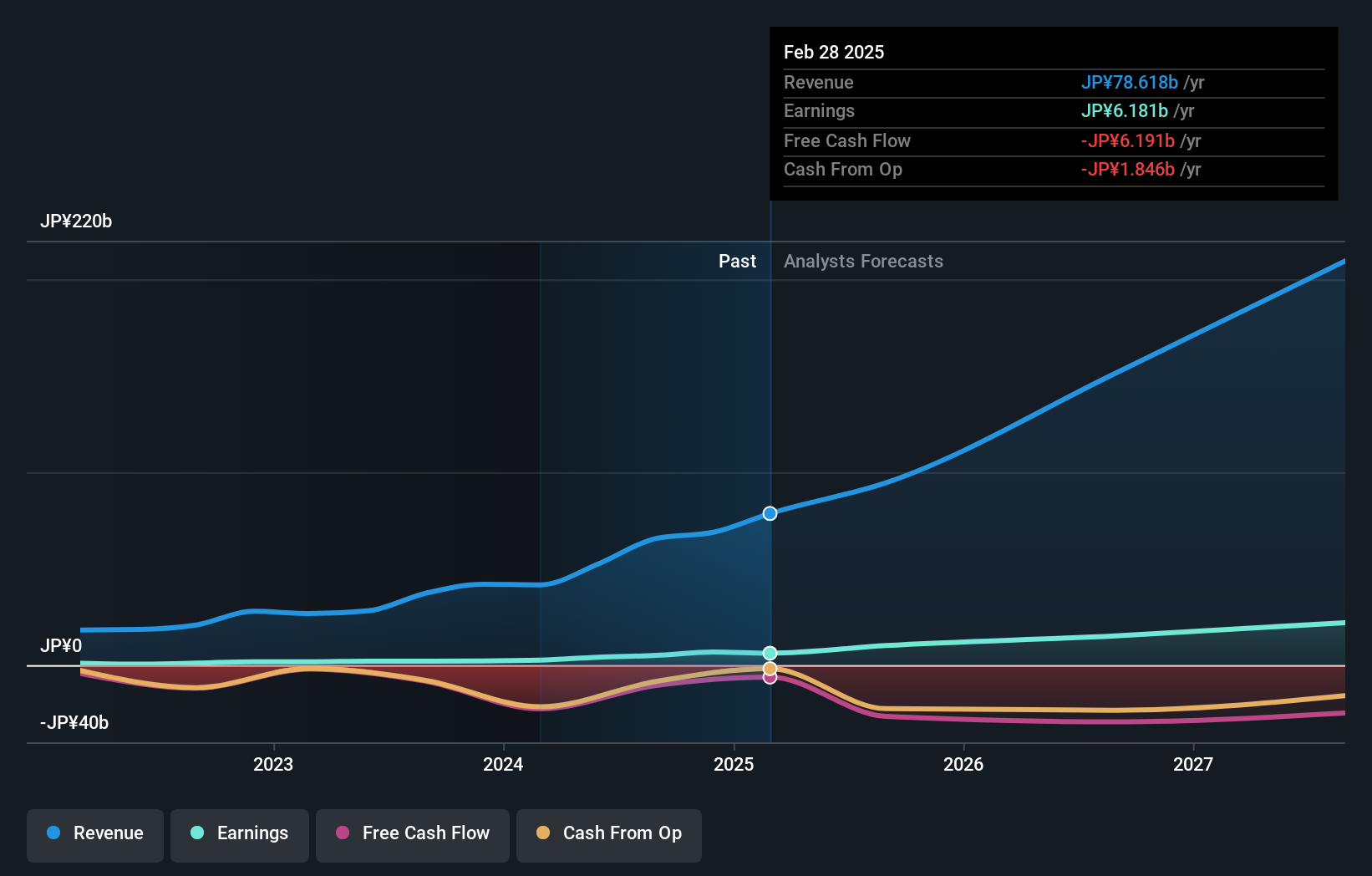

Kasumigaseki CapitalLtd (TSE:3498)

Simply Wall St Growth Rating: ★★★★★★

Overview: Kasumigaseki Capital Co., Ltd. operates in the real estate consulting sector in Japan, with a market capitalization of ¥168.14 billion.

Operations: The company generates revenue from its operations in the real estate consulting sector within Japan.

Insider Ownership: 34.7%

Return On Equity Forecast: 35% (2027 estimate)

Kasumigaseki Capital Ltd. demonstrates significant potential as a growth company with high insider ownership in Japan. The company is forecast to achieve revenue growth of 26.3% annually, outpacing the JP market's 4.2%, while earnings are expected to rise by 38.5% per year, surpassing market averages. Despite past shareholder dilution and debt coverage concerns, its new luxury hotel venture underlines strategic expansion efforts aimed at enhancing value and redefining guest experiences in the hospitality sector.

- Get an in-depth perspective on Kasumigaseki CapitalLtd's performance by reading our analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Kasumigaseki CapitalLtd shares in the market.

freee K.K (TSE:4478)

Simply Wall St Growth Rating: ★★★★★☆

Overview: freee K.K. provides cloud-based accounting and HR software solutions in Japan, with a market cap of ¥169.44 billion.

Operations: Revenue Segments (in millions of ¥): freee K.K. generates its revenue primarily through its cloud-based accounting and HR software solutions in Japan.

Insider Ownership: 23.9%

Return On Equity Forecast: 22% (2027 estimate)

freee K.K. is poised for robust growth, with revenue expected to increase by 18.2% annually, outpacing the Japanese market average of 4.2%. Earnings are anticipated to grow at a substantial rate of 74.08% per year, with profitability projected within three years. Despite recent volatility in share price and changes in executive leadership, including the appointment of Yasuhiro Kimura as CPO, the company remains undervalued by over half its estimated fair value, signaling potential for long-term investors.

- Click here and access our complete growth analysis report to understand the dynamics of freee K.K.

- According our valuation report, there's an indication that freee K.K's share price might be on the cheaper side.

LITALICO (TSE:7366)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: LITALICO Inc. operates schools for learning and preschool in Japan with a market cap of ¥44.28 billion.

Operations: The company's revenue segments include the Employment Support Business at ¥11.08 billion, the Child Welfare Business at ¥9.39 billion, and the Platform Business at ¥4.05 billion.

Insider Ownership: 37.2%

Return On Equity Forecast: 23% (2027 estimate)

LITALICO's revenue is forecast to grow at 13.8% annually, surpassing the Japanese market average of 4.2%, while earnings are projected to increase by 17.4% per year, exceeding the market's 8.7%. Despite a decline in profit margins from 10.6% to 7.4%, and a high debt level, its return on equity is expected to reach a robust 23.3% in three years. The stock trades significantly below its estimated fair value, though recent share price volatility persists.

- Unlock comprehensive insights into our analysis of LITALICO stock in this growth report.

- The valuation report we've compiled suggests that LITALICO's current price could be quite moderate.

Summing It All Up

- Investigate our full lineup of 101 Fast Growing Japanese Companies With High Insider Ownership right here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Kasumigaseki CapitalLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3498

Kasumigaseki CapitalLtd

Engages in real estate consulting businesses in Japan.

Exceptional growth potential moderate.