Advertisement

- China

- /

- Metals and Mining

- /

- SZSE:002290

Asian Insider-Owned Growth Stocks To Watch In March 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a period of uncertainty with growth stocks underperforming and geopolitical tensions affecting investor sentiment, Asia's economic landscape remains a focal point for opportunities. In this environment, companies with high insider ownership often attract attention due to the potential alignment of interests between management and shareholders, making them compelling candidates for those seeking growth in their portfolios.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.9% |

| PharmaResearch (KOSDAQ:A214450) | 38.6% | 26.4% |

| Samyang Foods (KOSE:A003230) | 11.6% | 29.7% |

| Laopu Gold (SEHK:6181) | 36.4% | 42.9% |

| Global Tax Free (KOSDAQ:A204620) | 20.4% | 77% |

| Suzhou Sunmun Technology (SZSE:300522) | 35.4% | 92.8% |

| Schooinc (TSE:264A) | 21.6% | 68.9% |

| Oscotec (KOSDAQ:A039200) | 21.2% | 148.5% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 125.9% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

Here we highlight a subset of our preferred stocks from the screener.

Qingdao Daneng Environmental Protection Equipment (SHSE:688501)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Qingdao Daneng Environmental Protection Equipment Co., Ltd. (ticker: SHSE:688501) specializes in the development and manufacturing of environmental protection equipment, with a market cap of CN¥2.05 billion.

Operations: Revenue segments for the company are not provided in the business operations text.

Insider Ownership: 27.2%

Earnings Growth Forecast: 32.1% p.a.

Qingdao Daneng Environmental Protection Equipment is positioned for strong growth, with earnings expected to grow significantly at 32.1% annually, outpacing the CN market. Despite a modest dividend yield of 1.32%, its price-to-earnings ratio of 21.7x suggests good value against peers and the broader market. Recent earnings reported sales of CNY 1.31 billion, up from CNY 1.03 billion the previous year, reflecting solid revenue expansion and steady profit increases amidst a competitive landscape.

- Get an in-depth perspective on Qingdao Daneng Environmental Protection Equipment's performance by reading our analyst estimates report here.

- Our valuation report here indicates Qingdao Daneng Environmental Protection Equipment may be undervalued.

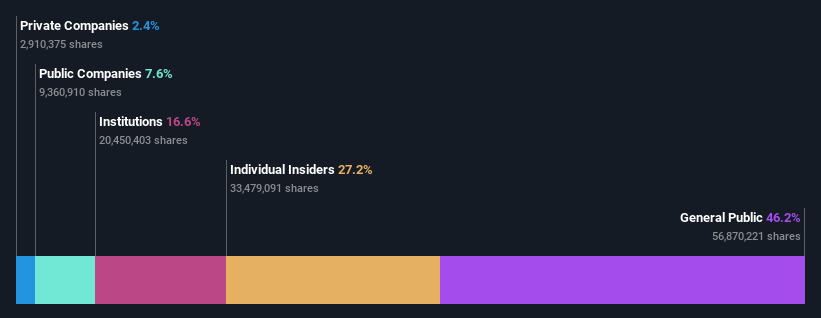

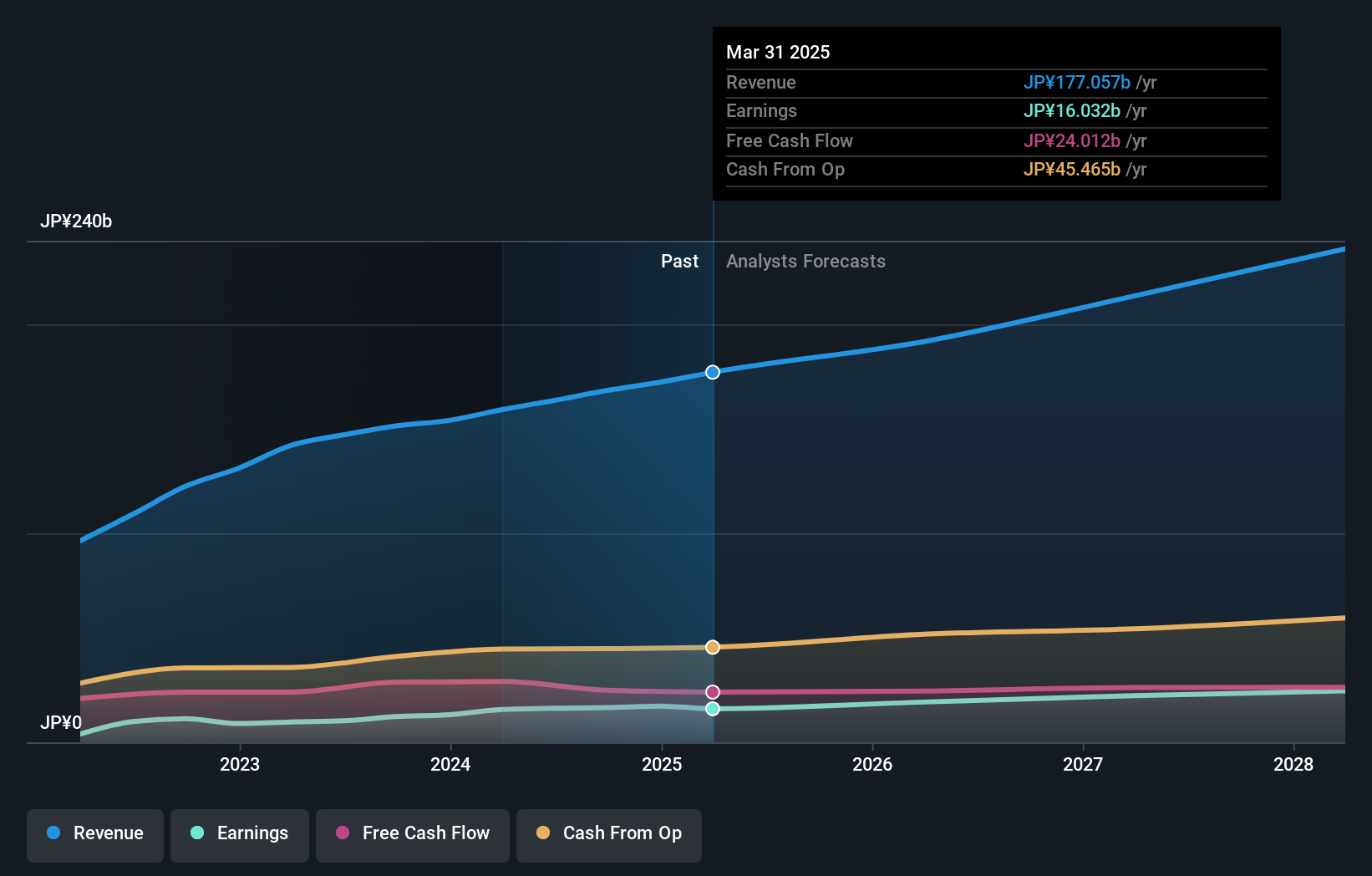

Suzhou Hesheng Special Material (SZSE:002290)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Suzhou Hesheng Special Material Co., Ltd. operates in the special materials industry and has a market cap of approximately CN¥6.31 billion.

Operations: Suzhou Hesheng Special Material Co., Ltd. generates revenue from its operations in the special materials industry, with a market capitalization of about CN¥6.31 billion.

Insider Ownership: 29.1%

Earnings Growth Forecast: 50.4% p.a.

Suzhou Hesheng Special Material is poised for substantial earnings growth, forecasted at 50.4% annually, significantly outpacing the CN market's 25.5%. While its revenue growth of 13.9% per year is slower than ideal, it still exceeds the market average of 13.3%. The company's Return on Equity is expected to reach a robust 20.7% in three years, despite recent share price volatility and modest past earnings growth of 4.4%.

- Take a closer look at Suzhou Hesheng Special Material's potential here in our earnings growth report.

- Our valuation report unveils the possibility Suzhou Hesheng Special Material's shares may be trading at a premium.

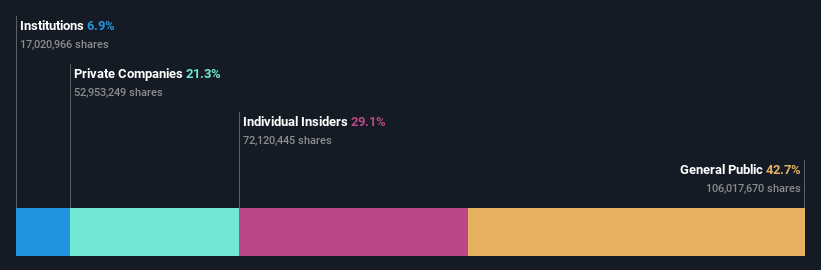

Round One (TSE:4680)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Round One Corporation operates indoor leisure complex facilities and has a market cap of ¥306.61 billion.

Operations: The company's revenue is primarily derived from its operations in Japan, contributing ¥101.35 billion, and the United States, adding ¥69.53 billion.

Insider Ownership: 35.7%

Earnings Growth Forecast: 11.8% p.a.

Round One Corporation is forecasted to achieve revenue growth of 7.4% annually, surpassing the JP market's 4.2%, with earnings growth projected at 11.8%, outpacing the market's 8%. The company's shares are trading at a significant discount to estimated fair value, and analysts predict a potential price increase of 32.1%. Recent sales reports show consistent revenue from Japan and the USA, while a recent share buyback reflects management confidence in its valuation.

- Click to explore a detailed breakdown of our findings in Round One's earnings growth report.

- Our comprehensive valuation report raises the possibility that Round One is priced lower than what may be justified by its financials.

Next Steps

- Click this link to deep-dive into the 645 companies within our Fast Growing Asian Companies With High Insider Ownership screener.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002290

Suzhou Hesheng Special Material

Suzhou Hesheng Special Material Co., Ltd.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor