YONEX (TSE:7906): Revisiting Valuation After a Sharp Pullback in a Strong Multi‑Year Rally

Reviewed by Simply Wall St

YONEX (TSE:7906) has been on a mixed run lately, with the stock easing over the past month even after strong gains this year. That pullback is prompting investors to revisit the valuation.

See our latest analysis for YONEX.

Despite the recent 1 month share price return of negative 12.6% as investors cool on cyclical consumer names, YONEX still has a robust year to date share price return of over 50 percent and a five year total shareholder return above 450 percent. This suggests long term momentum is intact even as near term enthusiasm fades.

If YONEX has you thinking about where the next strong consumer winner might come from, it could be worth scanning for fast growing stocks with high insider ownership as potential ideas to research next.

With earnings still growing, the share price well below analyst targets and our model implying further upside, the key question now is whether YONEX remains undervalued or if the market is already pricing in its future growth.

Price to Earnings of 24x: Is it justified?

Based on a price to earnings ratio of 24 times at the last close of ¥3,230, YONEX screens as expensive against both its peers and its own fair multiple.

The price to earnings multiple compares what investors are willing to pay today for each unit of the company’s current earnings, a key yardstick for established consumer brands like YONEX. For a business with solid but not hyper growth, a higher than average multiple often signals the market is assuming strong and durable profit expansion.

In YONEX’s case, the market valuation appears stretched relative to fundamentals implied by our models and peer comparisons. The stock is trading at 24 times earnings, while our fair price to earnings ratio estimate sits materially lower at 17.8 times, a level the market could gravitate toward if growth expectations ease.

Compared with valuation anchors in the sector, the premium is even clearer, with YONEX’s 24 times earnings multiple standing well above the JP Leisure industry average of 13.5 times and the selected peer group average of 12.4 times, underscoring how aggressively the market is pricing its earnings stream.

Explore the SWS fair ratio for YONEX

Result: Price-to-Earnings of 24x (OVERVALUED)

However, risks remain, including a sentiment reversal on consumer cyclicals or earnings disappointments that prompt a derating toward sector-level valuations.

Find out about the key risks to this YONEX narrative.

Another View on Value

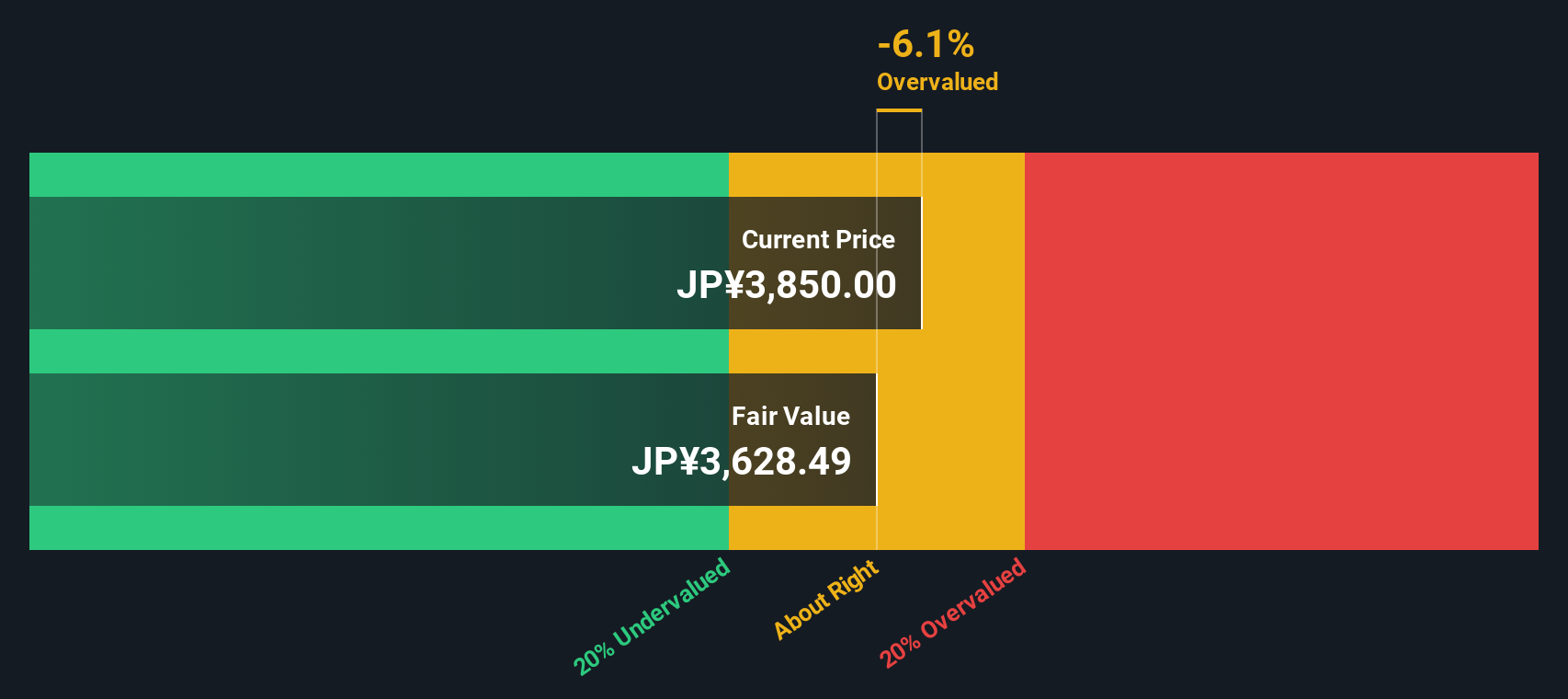

While the 24 times earnings multiple looks demanding, our DCF model paints a different picture, suggesting YONEX is trading about 25.6 percent below its fair value of roughly ¥4,344 per share. If cash flows point to upside while multiples flash risk, which signal should investors place more weight on?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out YONEX for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 906 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own YONEX Narrative

If you reach different conclusions or prefer to dig into the numbers yourself, you can quickly build a personalized view in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding YONEX.

Looking for more investment ideas?

Do not stop with a single stock story when you can quickly scan the market for other compelling setups that match your strategy on Simply Wall St.

- Capitalize on mispriced opportunities by targeting companies that our models flag as trading below intrinsic value through these 906 undervalued stocks based on cash flows.

- Ride structural growth in automation and data by focusing on innovators shaping the future of machine intelligence using these 26 AI penny stocks.

- Strengthen your income stream by filtering for reliable payouts and attractive yields via these 13 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7906

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)