- Japan

- /

- Professional Services

- /

- TSE:3967

Investors Shouldn't Be Too Comfortable With EltesLtd's (TSE:3967) Earnings

Last week's profit announcement from Eltes Co.,Ltd. (TSE:3967) was underwhelming for investors, despite headline numbers being robust. Our analysis uncovered some concerning factors that we believe the market might be paying attention to.

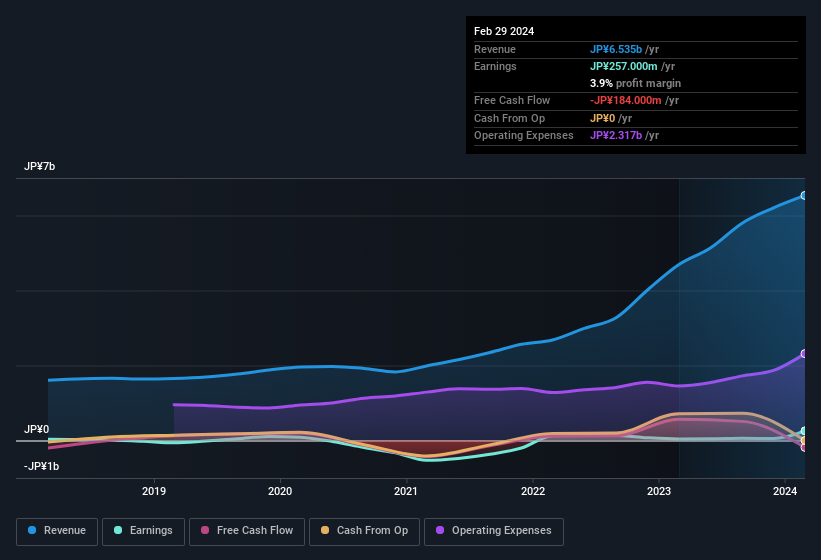

See our latest analysis for EltesLtd

The Impact Of Unusual Items On Profit

To properly understand EltesLtd's profit results, we need to consider the JP¥60m expense attributed to unusual items. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. Assuming those unusual expenses don't come up again, we'd therefore expect EltesLtd to produce a higher profit next year, all else being equal.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of EltesLtd.

An Unusual Tax Situation

Having already discussed the impact of the unusual items, we should also note that EltesLtd received a tax benefit of JP¥174m. This is of course a bit out of the ordinary, given it is more common for companies to be paying tax than receiving tax benefits! We're sure the company was pleased with its tax benefit. However, our data indicates that tax benefits can temporarily boost statutory profit in the year it is booked, but subsequently profit may fall back. In the likely event the tax benefit is not repeated, we'd expect to see its statutory profit levels drop, at least in the absence of strong growth. While we think it's good that the company has booked a tax benefit, it does mean that there's every chance the statutory profit will come in a lot higher than it would be if the income was adjusted for one-off factors.

Our Take On EltesLtd's Profit Performance

In its last report EltesLtd received a tax benefit which might make its profit look better than it really is on a underlying level. But on the other hand, it also saw an unusual item depress its profit. Based on these factors, we think it's very unlikely that EltesLtd's statutory profits make it seem much weaker than it is. If you want to do dive deeper into EltesLtd, you'd also look into what risks it is currently facing. To help with this, we've discovered 3 warning signs (1 shouldn't be ignored!) that you ought to be aware of before buying any shares in EltesLtd.

In this article we've looked at a number of factors that can impair the utility of profit numbers, as a guide to a business. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you're looking to trade EltesLtd, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if EltesLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3967

EltesLtd

Engages in the AI security, digital risk, and DX promotion businesses in Japan.

Adequate balance sheet and slightly overvalued.

Market Insights

Community Narratives