- Japan

- /

- Professional Services

- /

- TSE:277A

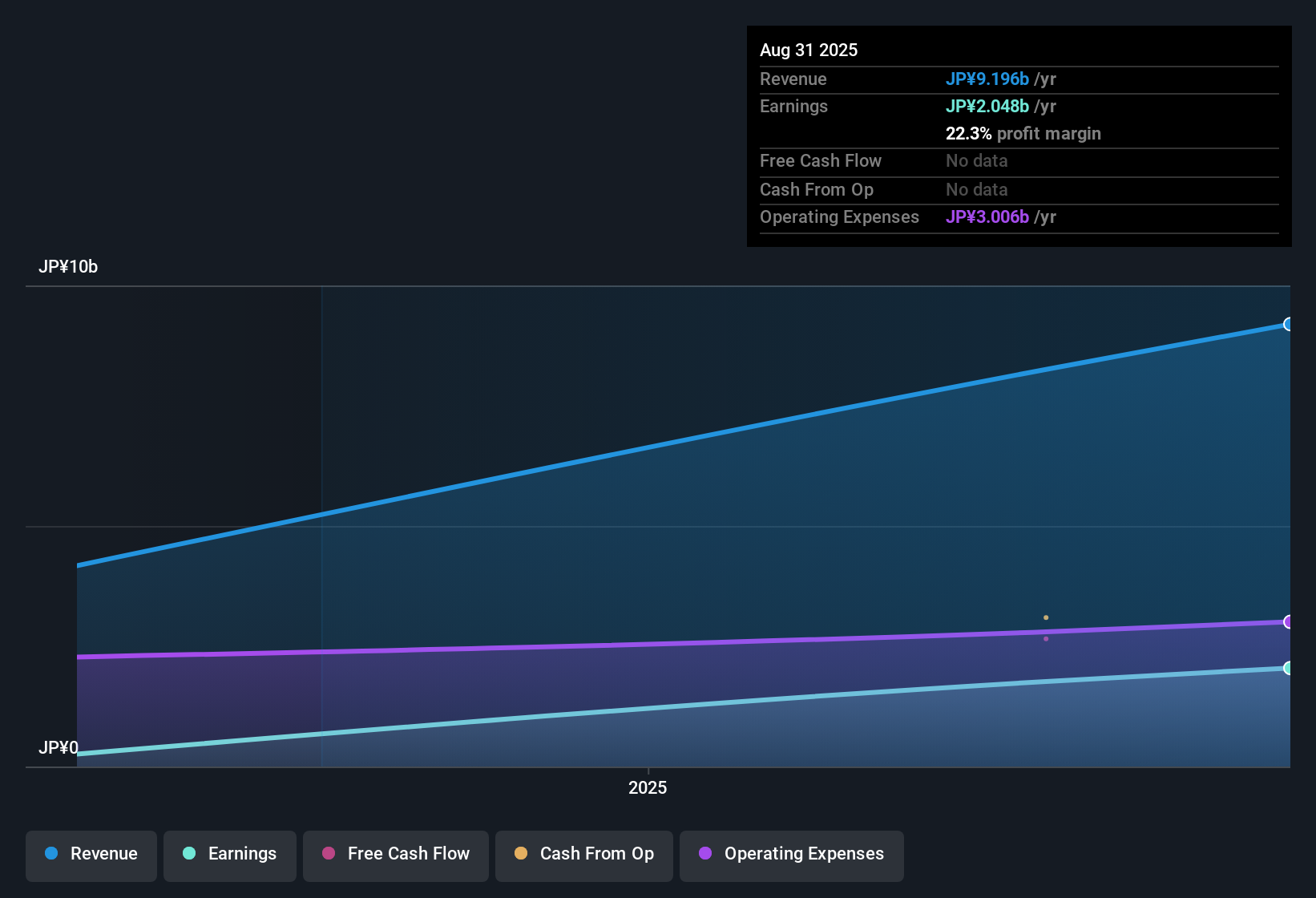

Globe-ing (TSE:277A) Net Margin Jumps to 22.3%, Reinforcing High-Quality Earnings Narrative

Reviewed by Simply Wall St

Globe-ing (TSE:277A) recorded a net profit margin of 22.3%, up from 12.3% last year, reflecting a notable jump in profitability. Both revenue and earnings are forecast to grow rapidly, with projections of 21% and 20.3% per year respectively, outpacing the broader Japanese market. Investors are weighing these strong growth drivers against recent share price volatility as the company enters earnings season.

See our full analysis for Globe-ing.Next, we will see how the numbers compare to the prevailing narratives. Some long-held views may be reaffirmed while others could be challenged by the data.

Curious how numbers become stories that shape markets? Explore Community Narratives

DCF Fair Value Points to Undervalued Share Price

- At ¥2,653, Globe-ing's stock trades meaningfully below its DCF fair value estimate of ¥3,547.42, creating a fundamental valuation gap even as price-to-earnings multiples look stretched versus peers.

- What stands out is how this discounted cash flow valuation heavily supports the bullish view that Globe-ing offers long-term upside despite short-term volatility.

- Strong revenue and earnings momentum, both forecast to grow over 20% per year, provide tangible evidence to back up the idea of undervaluation on a cash flow basis.

- Bulls argue that high profit margins (now 22.3%) and above-market growth rates justify Globe-ing’s premium price-to-earnings ratio, positioning it ahead of slower-growing competitors.

Margins Outpace Peers, but Share Price Swings Hard

- Net profit margin of 22.3% puts Globe-ing well ahead of most industry peers, yet the company’s share price has shown notable volatility over the last 3 months, signaling uncertainty around how consistently these margins can be maintained.

- Digging into the prevailing market view reveals sharp tension between steady operational strength and the unpredictable stock price.

- Investors see profitability as a positive core driver, but recent price swings create hesitation, especially without clear forward guidance.

- Profit expansion supports optimism, yet questions linger about whether Globe-ing can sustain these margins under changing market conditions.

Growth Pace Surges Past National Average

- With annual revenue growth projected at 21% and profit growth at 20.3%, Globe-ing is advancing more than four times faster than the Japanese market’s 4.4% average revenue growth rate.

- This breakneck expansion supports a narrative of operational momentum and sector leadership.

- Outpacing broader market trends suggests Globe-ing has competitive advantages, fueling investor demand despite valuation concerns.

- Skeptics may highlight that premium multiples add risk, but the current trajectory aligns with the company’s “high quality earnings” label in filings.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Globe-ing's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Despite rapid growth, Globe-ing's shares remain subject to sharp price swings. This raises concerns about stability and the predictability of future performance.

If you prefer steady gains and less volatility, use our stable growth stocks screener (2097 results) to discover companies with consistent track records and smoother earnings trajectories.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:277A

Globe-ing

Provides DX and strategic consulting, and digital analytics/data services in Japan.

Exceptional growth potential with flawless balance sheet.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)