- Japan

- /

- Trade Distributors

- /

- TSE:8001

ITOCHU Corporation's (TSE:8001) Stock Is Going Strong: Is the Market Following Fundamentals?

Most readers would already be aware that ITOCHU's (TSE:8001) stock increased significantly by 16% over the past three months. Given the company's impressive performance, we decided to study its financial indicators more closely as a company's financial health over the long-term usually dictates market outcomes. In this article, we decided to focus on ITOCHU's ROE.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

View our latest analysis for ITOCHU

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for ITOCHU is:

14% = JP¥884b ÷ JP¥6.1t (Based on the trailing twelve months to September 2024).

The 'return' is the profit over the last twelve months. One way to conceptualize this is that for each ¥1 of shareholders' capital it has, the company made ¥0.14 in profit.

Why Is ROE Important For Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

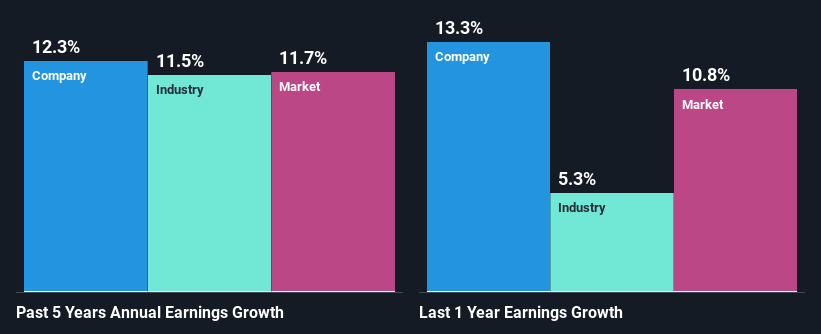

A Side By Side comparison of ITOCHU's Earnings Growth And 14% ROE

To begin with, ITOCHU seems to have a respectable ROE. Especially when compared to the industry average of 7.3% the company's ROE looks pretty impressive. Probably as a result of this, ITOCHU was able to see a decent growth of 12% over the last five years.

We then performed a comparison between ITOCHU's net income growth with the industry, which revealed that the company's growth is similar to the average industry growth of 12% in the same 5-year period.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. What is 8001 worth today? The intrinsic value infographic in our free research report helps visualize whether 8001 is currently mispriced by the market.

Is ITOCHU Using Its Retained Earnings Effectively?

ITOCHU has a healthy combination of a moderate three-year median payout ratio of 26% (or a retention ratio of 74%) and a respectable amount of growth in earnings as we saw above, meaning that the company has been making efficient use of its profits.

Besides, ITOCHU has been paying dividends for at least ten years or more. This shows that the company is committed to sharing profits with its shareholders.

Summary

In total, we are pretty happy with ITOCHU's performance. Particularly, we like that the company is reinvesting heavily into its business, and at a high rate of return. Unsurprisingly, this has led to an impressive earnings growth. Having said that, the company's earnings growth is expected to slow down, as forecasted in the current analyst estimates. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

If you're looking to trade ITOCHU, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8001

ITOCHU

Engages in trading and importing/exporting various products worldwide.

Solid track record with excellent balance sheet and pays a dividend.