Advertisement

Is Takeuchi Mfg (TSE:6432) Still Undervalued After Upgraded Sales and Profit Outlook?

Simply Wall St

Reviewed by Kshitija Bhandaru

Takeuchi Mfg (TSE:6432) has just updated its guidance for the fiscal year ending February 2026, now expecting higher net sales and stronger profits. This upward revision is largely credited to sales growth in North America and Europe, even as some markets faced headwinds.

See our latest analysis for Takeuchi Mfg.

Takeuchi Mfg’s latest upward earnings revision comes after a year of sustained momentum, with its share price now at ¥5,240 and a total shareholder return of 15.6% over the past year. While recent quarterly profits saw some pressure, the stock has more than doubled total returns over three and five years. This signals investor confidence in the company’s international growth prospects.

If you’re interested in finding other promising names, now’s a great time to broaden your search and discover fast growing stocks with high insider ownership

The company’s upbeat guidance and track record of double-digit returns raise a key question for investors: does Takeuchi Mfg remain undervalued after its strong run, or is future growth already reflected in the current share price?

Price-to-Earnings of 9.7x: Is it justified?

At a last close price of ¥5,240, Takeuchi Mfg trades on a price-to-earnings (P/E) multiple of 9.7x. This makes the stock look attractively valued compared to its competitors and sector peers.

The price-to-earnings ratio compares a company's share price to its earnings per share. It is a key tool for assessing whether a stock is expensive or cheap relative to its profits. For a company in the machinery sector like Takeuchi Mfg, the P/E ratio is especially relevant as it helps investors judge how much they are paying for current and future earnings power.

This P/E of 9.7x is substantially below both the JP Machinery industry average of 13.5x and the peer average of 28x. According to our valuation framework, the stock also trades at a steep discount to a fair P/E ratio estimate of 14.8x. This indicates plenty of upside potential if market sentiment shifts.

Explore the SWS fair ratio for Takeuchi Mfg

Result: Price-to-Earnings of 9.7x (UNDERVALUED)

However, investors should note that the stock trades 13% above analyst targets. Recent revenue growth, while positive, has slowed compared to prior years.

Find out about the key risks to this Takeuchi Mfg narrative.

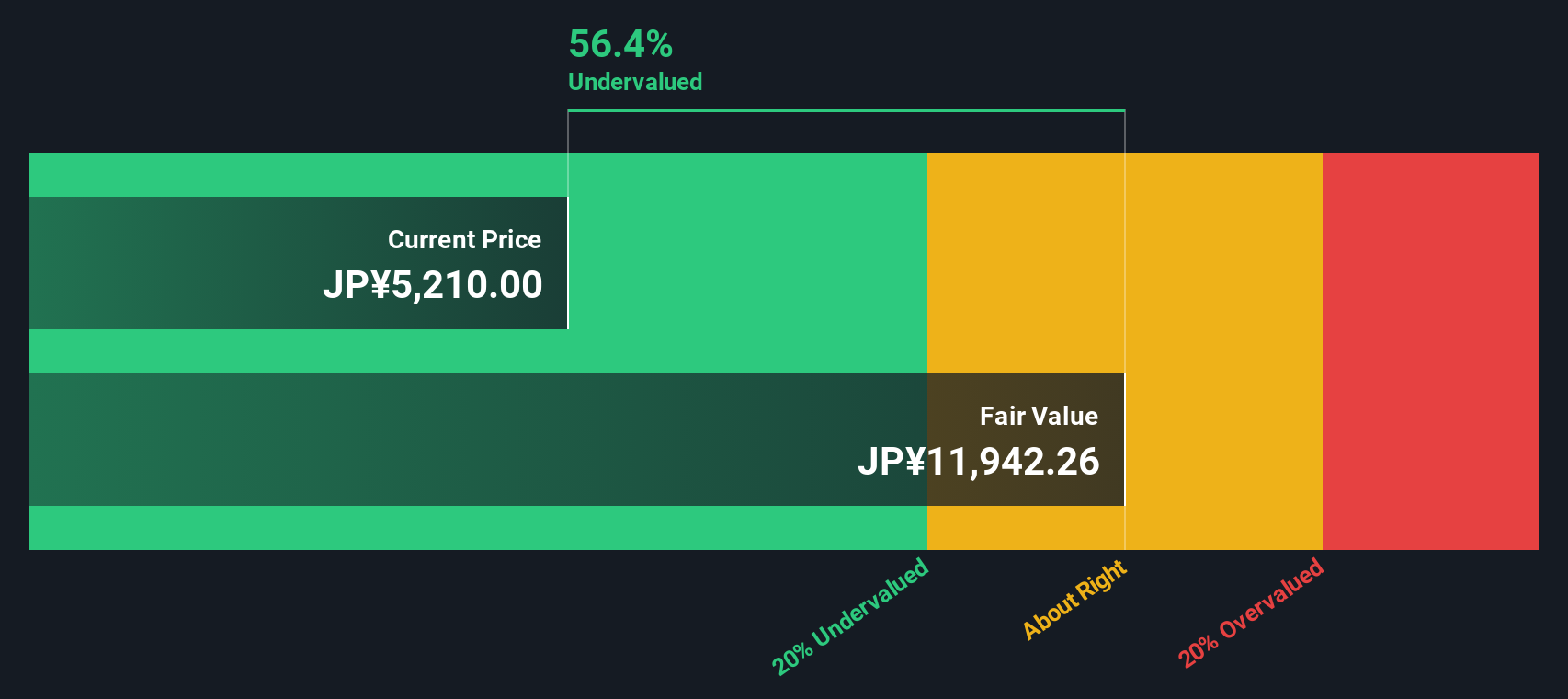

Another View: Discounted Cash Flow Model

While the price-to-earnings approach suggests Takeuchi Mfg is attractively valued, the SWS DCF model points to an even larger opportunity. Our DCF estimate places fair value at ¥11,676, about 55% above the current share price. Are market expectations too low, or is there something the model may be missing?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Takeuchi Mfg for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Takeuchi Mfg Narrative

If you have a different viewpoint or enjoy delving into your own research, you can quickly generate your personal narrative in just a few minutes. Do it your way

A great starting point for your Takeuchi Mfg research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Take your investing strategy further and don’t let exciting opportunities slip by. See what’s driving growth and value in high-potential companies right now.

- Unlock the upside in undervalued stocks by reviewing these 888 undervalued stocks based on cash flows based on powerful cash flow fundamentals.

- Boost your passive income potential with these 18 dividend stocks with yields > 3% offering strong yields above 3%.

- Get ahead of innovation by checking out these 25 AI penny stocks with advanced applications across industries.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Takeuchi Mfg might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6432

Takeuchi Mfg

Manufactures and sells construction machinery in Japan and internationally.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor